Bond investors are still trying to recover from 2022, arguably [the worst year in history] for fixed income. After that 13% annual loss in the aggregate U.S. bond market, fixed-income funds still have billions of dollars of unrealized losses on their books.

That, in turn, has created a highly unusual opportunity. Because of those losses, a substantial chunk of many bond funds’ current and future returns won’t be subject to the tax treatment that historically was typical.

For most of the past four decades, bond prices rose and yields fell, so capital losses were rare at investment-grade bond funds, especially at index funds that seldom trade their holdings. The bulk of the returns on bond funds tended to come from their interest income—taxable at ordinary-income rates that could exceed 40%.

After 2022, however, deep losses are embedded in many mutual funds and exchange-traded funds that invest in high-quality, intermediate-term and long-term bonds. That enables current and future returns on a portion of those funds’ holdings to be taxed at the capital-gains rates that apply to investments held for more than one year. The maximum rate there is 20%, roughly half the top ordinary-income rate.

I play with bonds very little, and bond funds even less mostly because I got killed on the tax angle when I did. But this article makes me think there might be something there if you’re worried about the tax bite from passive income.

I have reverted back to my theory that yields won’t fall much. The reason is inflation as a background noise is here to stay. The income taxes are not that high in the US. Employment is going to be strong most of the coming ten years.

I do not see bad inflation. I actually see very little inftlation going forward. But I do see the need for higher yields and modest taxation.

Corporate taxes are to be cut soon in a deal. I expect that as sound economic reworking against a mild recession in some industrial sectors. That along with a larger Unearned Income Credit. Whatever it is called. That leaves consumption stronger as well.

We are in a time of mild swings but high real GDP growth.

Hard not to live it up in equities. We face a possibility of seasonality in the 1H24. Early to say.

If you look at the BLE chart, the bottom was – surprise, surprise – Oct 28. You are a bit late to the party but there is much more potential if rates continue to fall. Of course some think interest rates will plateau for a while. That can limit capital gains but better dividends are attractive.

We talked about BLE before. It is a leveraged closed end tax exempt bond fund. Some one objected to the high expense ratio. They said 5%, actually its 3.4%. But it turns out the interest paid to borrow for leverage is counted in the expense ratio. Mgt fee is 0.9%. So all leveraged funds have high expense ratios.

It’s important to have a large fixed income allocation early in retirement to guard against a large market drop. Then if you happen to retire into a favorable market, you can reduce your fixed income allocation as your portfolio grows. For example, if your portfolio doubles in value, and your withdrawal rate is now 2% rather than 4%, you can half your fixed income allocation to 20% from 40% and still have the same number of years of spending in fixed income.

I’ve actually considered what I would do for my bond allocation once I hit retirement, and BRK.B was on my radar. And possibly some dividend aristocrat stocks as well. But agreed to avoid bond funds and I learned that the hard way in our 529 plan, which did horrible in 2022 (because the enrollment target date fund is 60% bonds). Ugh.

It’s important to have enough money when you retire so when you have a large market drop you do not have to worry about it. Just realize you might have drops of 30 to 50 percent. Don’t leverage and you will be fine.

With due respect, that is the worst take. You settle for whatever yield, but that doesn’t mean “you are picking pennies in front of a bulldozer” , if you want to describe selling puts for income as such, I can understand.

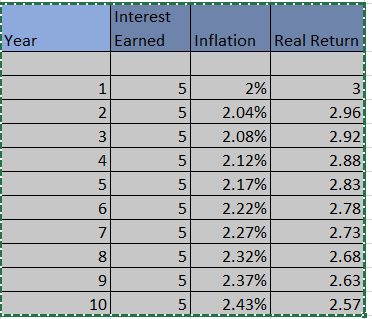

If we are not having “inflation” then we are having deflation. So in general interest rates are “inflation”+ real rates, currently the real rates are high. Expect interest rates to come down. Where long-term investing in bonds fail is due to compounding nature of inflation. For ex:

If the coupon or yield on a $100 face value bond is 5% and we have inflation 2%, You started with real return of 3% and the steady inflation has eroded your real return to 2.57. Where the trouble is in US the real return is squeezed and especially savers were punished by FED ever since GFC. Also, FED and politicians, in the last 2 decades got addicted to money printing or easy money policies. So expect rates to go down. Still one can expect 2% ~ 2.5% real return.

Poor take. While FED may bring headline inflation to around 2%, the inflation affects various folks in different ways. Generally service costs goes up, house price goes up much higher than inflation, medical costs averaged CAGR 5.5%. College tuition is another area that sees price increase much higher than inflation.

<> A reckless federal education policy that subsidizing many private colleges offering useless degrees, and now compounded by tuition waiver is only going to make a worst situation even worse. All statistics shows US college students live longer, have multi-million retirement nest, own house, travel the world etc… This is the best cohort in the world. Let it sink, US college grads are the best cohort in the world. Any policy waiving their college tuition is the worst policy, fiscally irresponsible << End Rant>>

Only if they are STEM graduates, doctors or lawyers. Many people have gotten scammed by the “college at any cost” that was promoted by both parties over the past 40 years and ended up with useless degrees, if they graduated at all. Many of those folks are still poor, and backpacking and staying in hostels, if they’re even traveling.

What if they raise interest rates more? If you hold them till maturity I guess that would work but if interest rates are at 8 percent and you are holding a bond for 20 years at 4 percent I would see that as a loss.

Fair enough. Then why not “define poor” and set eligibility. Most folks don’t pay these loans because of tax benefits. How about using some common sense definitions? If you own a house, you bought a new car in the last 2 or 3 years, have assets that are 10x of your loan etc.

Your narrative of poor has no data to support. It is a narrative sold by politician which you are buying.

You cannot predict future, every investment has risk. Now, that doesn’t mean they are “picking pennies in front of a steamroller”. That phrase is for “assuming huge risk for a a small return”. Even in your 8% scenario, what are the possibilities of it?, your loss is the different between the coupon vs at any given time interest rate. Not permanent loss of capital or other significant loss.

Whether to invest in a bond or not is your personal choice, and circumstances. But your description just doesn’t fit.

You are arguing against strawmen. We are not talking about any asset class comparison. Also, not everyone has a “long run” window. If your individual circumstances allows you to be fully invested in equities great. Saying that meets everyone’s need is an indefensible argument.