Hi all - Some of us (still) hold ELF, which has taken quite a haircut lately (presumably) due to Ulta’s forecast that a predicted cosmetic slowdown has come earlier than expected [link here]

When something like this happens, I do my best to evaluate the “quality of the data”. Sometimes there’s news or a report and it’s more flash than substance, which can sometimes affect valuation but often valuation bounces back in a few days, but this news/revelation from Ulta deserves at least some consideration, since they’re closer to the paying customer.

Next, I look at 2 things: 1. the strength of the company/business and 2. its valuation:

-

Company strength: ELF is strong, taking share from the other (older) brands and growing revenue, and in a very profitable way. Here’s the link to their presentation at CAGNY:https://staticcontents.investis.com/media/e/elfcosmetics/elf-cagny-2024.pdf. No concerns here.

-

Valuation: Here’s where it gets interesting (and where I’ve been burned before). As we all know, valuation is such a tricky thing to establish. I use market cap divided by (future) annual revenue if I can get the data. But there are other ways to do it, including discounted cash flow analysis. In this case, since Loreal is a French company, I had a hard time finding their outlook revenue, so I went with TTM. And Loreal is such a large conglomerate, they sell so many different products, including cosmetics, so not sure if it’s even relevant anyway, but it’s included in the data below. Clearly ELF is priced like a market leader:

There’s an interesting free article on Seeking Alpha asserting that ELF is poised to continue taking significant market share](e.l.f. Beauty: Poised To Gain Market Share Leading To Further Upside. (NYSE:ELF) | Seeking Alpha). The upshot of the article is that ELF is oversold, and an argument is made that a reasonable valuation is $200/share perhaps in 2025.

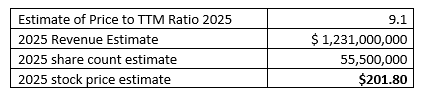

Using my simple valuation approach, let’s estimate ’25 revenue and see what we find. In FY24, ELF is forecasted to see 70% revenue growth YoY, but projections suggest a slowdown in growth for FY25, expected to be in the high twenties range. So just going with 25% growth, we get the following:

Just using back of the envelope math, and with the following assumptions, yields the following:

So using my simple valuation model also gets us in the $200 range, in 2025. Does that mean it will happen? No, unfortunately, but I still hold ELF and have not sold any, in fact.

Below is a quick look at Elf’s recent performance and their history of sandbagging![]() , going back one year.

, going back one year.

Reminder ELF is expected to announce their results on 5/22/24 for their quarter ending in 3/31/24.

I’m curious how others are evaluating ELF currently.