At about 2 minutes in, DasGupta talks about their primary advantage - safety - coming from a ceramic layer in the modules. Sounds a lot like Aspen Aerogels material, which also has ceramic in it. I wonder how unique Electrovaya’s approach really is, and whether it’s truly unique and patent-protectable, or whether it’s just they’re the only ones currently using it in their market (forklift batteries).

At about 3 minutes in, DasGupta mistates cycle life. He claims that “about 800 cycles” is equivalent to 2 years of cell phone use. In the battery industry, a “cycle” is defined as a 0% to 100% SOC charge/discharge cycle. If you charge your phone at night from 50% to 100% and then use it the next day down to 50%, that’s only a half cycle. In this example, 800 cycles is equivalent to 1600 days, or over 4 years. Another aspect of cycle life is that it “ends” when the battery capacity is 80% of new, so batteries are still usable after that.

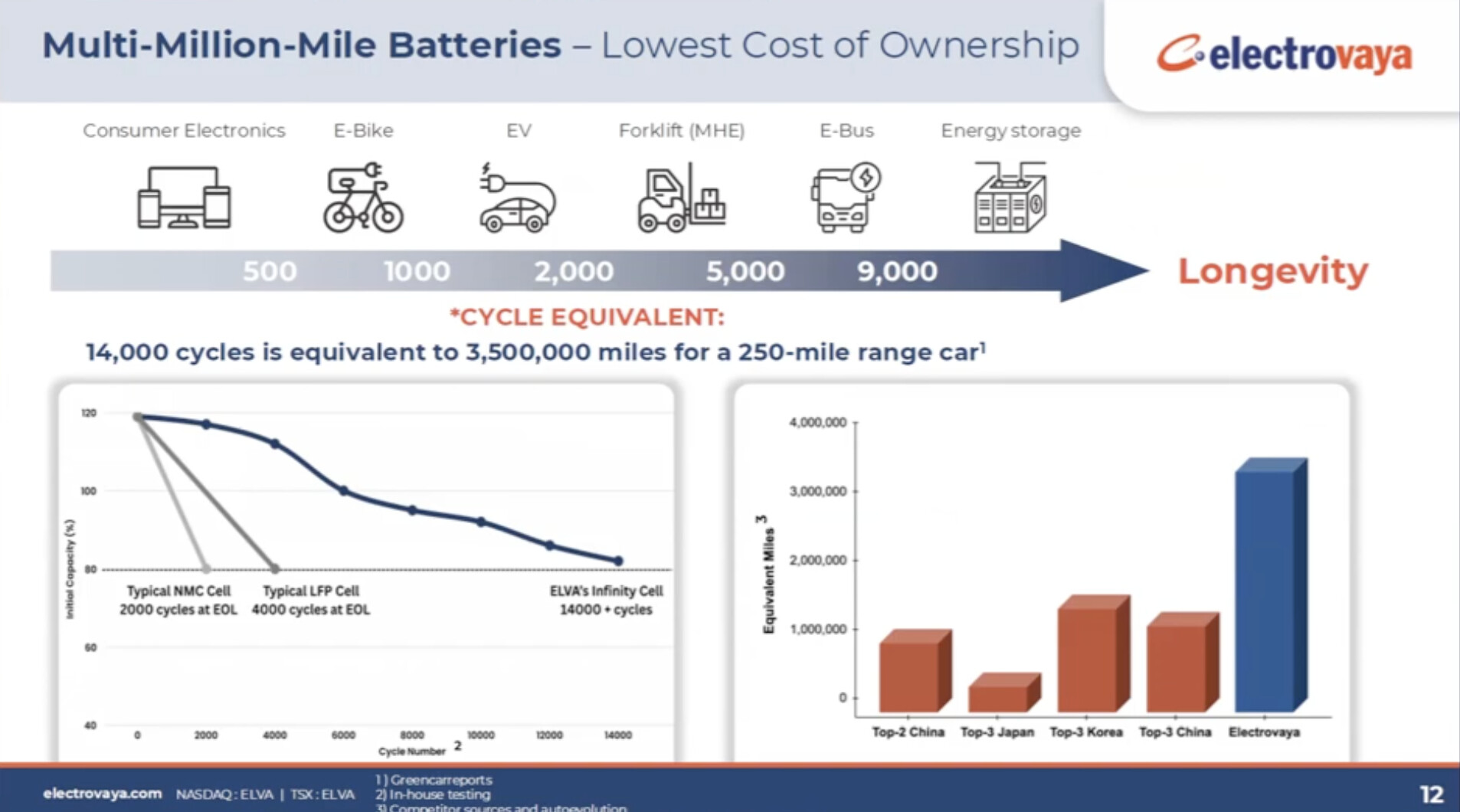

BTW, Electrovaya has previously described its product as “a million mile battery,” but do not compare with car/truck batteries , which have different operating requirements. For instance, Electrovaya’s best battery has a WH/Kg (Watt-Hour to Kilogram) ratio of 171 while Tesla’s batteries are between 260 and 295 today. It’s fine for a forklift to be heavy - it’s actually considered a good thing to help counterbalance the weight of what it’s carrying on the forks! Not so much for passenger cars, where it adversely impacts range.

Another thing I found odd was that at one point DasGupta says they’re not going after the EV market, but then shows this slide:

Even though its for comparison of cycle life, one can’t isolate cycle life from other battery attributes. Personal electronic devices can’t have sophisticated cooling mechanisms, E-bikes and EVs can’t be too heavy and have to operate in wide temperature ranges, etc. And the numbers for cycle life can be (and have by some automotive companies) juiced by the BMS preventing the cells from being fully charged or discharged. Like having a pack that looks like a 60kWh pack, but in reality is a 100kWh pack where the BMS stops charging at 80kWh and shuts down at 20kWh. You’ll get great cycle life out of that, at the price of additional cost and weight. Although that does vary with chemistry as the LFP lithium cells can go to 100% with no additional degradation.

Thinking about this, Electrovaya might be doing this. Their Wh/Kg ratio isn’t great, so maybe they’re reserving additional cell capacity to help apparent cycle life. But, I’m speculating here.

OTOH, they claim “Set to be one of the only profitable battery companies in North America.” That would be great if it comes to pass, but it also shows how tough an industry batteries are.

Market cap of just over $200M is pretty small, making this a true “micro-cap” company.

One AI says:

Electrovaya (TSX:ELVA)

Overview: Electrovaya Inc. designs, develops, manufactures, and sells lithium-ion batteries and related products for energy storage and clean electric transportation in North America, with a market cap of CA$415.51 million.

Operations: The company generates revenue of $54.88 million from the development, manufacturing, and marketing of power technology products.

Estimated Discount To Fair Value: 47.3%

Electrovaya, trading at CA$10.27, is significantly undervalued based on discounted cash flow analysis with an estimated fair value of CA$19.51. The company recently reported record revenue growth, exceeding $64 million for fiscal 2025 and showing strong year-over-year performance. Despite past shareholder dilution and interest coverage concerns, Electrovaya’s earnings are forecast to grow over 41% annually, driven by robust demand for its innovative energy storage systems and strategic positioning in the North American market.

So, I can’t say anything about the financials. If the above is correct, then it’s had some dilution and interest rate concerns, but those may be in the past, making this stock still undervalued. The only thing I can say is that the battery business is tough. That ELVA is so small, however, does give it a possibility of growing into it’s limited market, which if it does, would boost the stock. I’m just so wary of battery companies, it’ll take more than what I’ve seen to make me invest.