This is from the EOSE Investors X Subthread

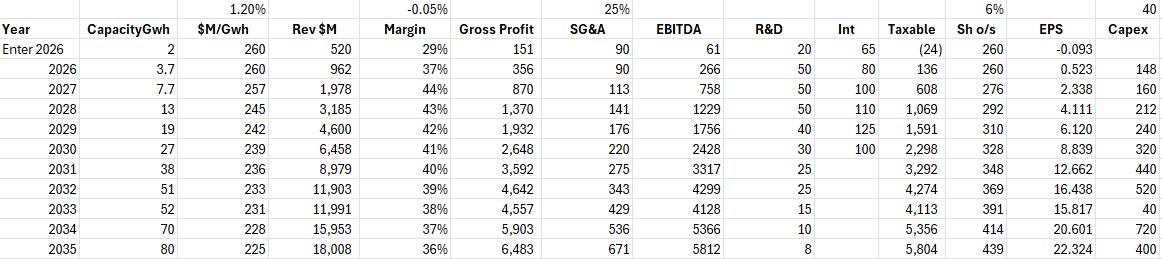

EOS Energy Enterprises: Pioneering Zinc-Based Long-Duration Energy Storage Investment Pitch - TL;DR version EOS Energy Enterprises ($EOSE) is entering its first year of scaled commercial operations with momentum across manufacturing, capital, and customer growth. Its Z3 battery—designed for safe, scalable, U.S.-made long-duration energy storage—is now being deployed at scale, with efficiency and installation milestones that significantly lower project costs. Backed by a DOE loan, strategic investment from Cerberus, and recent capital raises totaling $336 million, EOS is expanding production capacity toward 8 GWh and delivering on a $680.9M backlog and $15.6B pipeline. From data centers to grid peakers, standalone storage is driving new demand, and EOS is positioned to lead with a fully domestic, non-lithium solution. Long-form Pitch EOS Energy Enterprises specializes in zinc-based long-duration energy storage (LDES) systems, including standalone storage - critical for firming capacity and integrating renewable energy sources like solar and wind into the grid. With U.S. demand for LDES projected to reach 460 GW by 2050, EOS’s advanced zinc-bromine battery technology positions the company at the forefront of this rapidly expanding market. Technological Advancements and Manufacturing Milestones Building upon zinc-bromine battery technology initially developed by Exxon in the 1970s, EOS has secured multiple new patents over the past decade, enhancing various aspects of its battery systems. In June 2024, EOS commenced commercial operations of its first state-of-the-art manufacturing line, producing the Z3 battery - its first truly manufacturable, high-throughput design. The EOS Znyth™ aqueous zinc battery was designed to overcome the limitations of conventional lithium-ion technology. It is non-flammable, can be safely installed indoors and out, is scalable, efficient, quiet, and manufactured in the U.S. These attributes position EOS’s technology as a robust, safe, and proven solution for utility, industrial, and commercial customers with energy storage needs in the 3 to 12-hour range. The system is also well-suited for standalone storage deployments requiring long-duration performance and minimal degradation over time. Recent system-level milestones confirm Z3’s manufacturability and performance: EOS cold commissioned 75 cubes in just 7 days at a recent site - reducing installation costs by 96% versus prior designs. Z3 systems now achieve round-trip efficiencies above 80%, with some longer-duration configurations surpassing 90%. EOS Energy Enterprises joins the ranks of just four other U.S. companies recognized by Bloomberg New Energy Finance (BNEF) as a Tier 1 energy storage supplier. This elite group includes Tesla, Fluence, and FlexGen Power Systems. Powin Energy, formerly on the list, no longer meets BNEF’s criteria following its recent bankruptcy filing. Strategic Grid Applications Beyond Renewables In addition to its critical role in firming renewables, the Z3 battery is itself a fully dispatchable energy asset - capable of delivering multi-hour power on demand. EOS is also targeting standalone storage configurations that complement gas peaker plants - enhancing grid responsiveness, strengthening capacity, and improving the overall efficiency and flexibility of thermal generation assets. CEO Joe Mastrangelo has identified this application as a strategic focus area, further expanding the relevance of EOS’s technology across a broader range of utility use cases. Strategic Partnerships and Financial Growth Since going public in 2020, EOS has navigated capital markets and operational risk to secure critical funding from both private and public sources - positioning the company for scalable growth. In August 2023, EOS partnered with ACRO Automation Systems, a Wisconsin-based leader in high-speed, custom-designed manufacturing systems, to develop and deliver the company’s first high-throughput Z3 production line. ACRO played a key role in the successful launch of EOS’s first commercial manufacturing line in June 2024, and continues to be a critical partner in scaling the company’s production capacity. Under Project AMAZE, ACRO is now actively engaged in delivering Line 2, which has been ordered and is expected to be operational in the first half of 2026, with additional lines anticipated in future phases of the company’s scale-up roadmap. In June 2024, EOS announced a strategic investment agreement with Cerberus Capital Management, a global investment firm with $65 billion in AUM. The deal included a Delayed Draw Term Loan (DDTL) and warrant package, structured to provide up to $315 million in total capital, contingent on meeting operational milestones. Cerberus’s involvement brought not just funding, but operational and technical support to accelerate EOS’s execution strategy. As of June 2025, EOS had successfully met 15 of the 16 performance milestones associated with the DDTL agreement, with the final milestone on track to be achieved in July. Further bolstering its financial foundation, EOS finalized a $303.5 million loan guaranteed by the U.S. Department of Energy (DOE) in December 2024. The funding - awarded after a rigorous two-year vetting process that validated the technical strengths and commercial viability of EOS’s battery technology - will support Project AMAZE, the company’s initiative to expand manufacturing capacity to 8 GWh by 2027 with state-of-the-art, high-volume production lines. In early July 2025, EOS received the second disbursement under Tranche One of the loan guarantee and has now drawn the full $91 million allowed under that tranche. Most recently, in June 2025, EOS raised $336 million in gross proceeds through oversubscribed public equity and convertible note offerings, with underwriter options fully exercised in both. Proceeds from the raise were used to repurchase $131 million of existing convertible debt from Spring Creek Capital, make a $50 million prepayment on the Cerberus loan, cover $16 million in fees associated with the transactions, and add approximately $139 million in cash to the balance sheet. The $50 million Cerberus prepayment triggered significant improvements: the loan’s interest rate was reduced from 15% to 7%, financial covenants were deferred to 2027, and nearly $29 million in prepayment penalties were waived. Together, these three capital events provide EOS with a fully funded execution runway, a reduced cost of capital, and the institutional backing needed to deliver on its rapidly growing project pipeline. Supply Chain Strengthening and Market Expansion In January 2024, TETRA Technologies, a key supplier of high-purity zinc-bromide electrolyte essential to EOS’s batteries, announced a significant multi-year capital investment to ensure a reliable supply of this critical material. Through its U.S.-based manufacturing process, TETRA will provide at least 75% of EOS’s electrolyte needs, securing a domestic supply chain and underscoring confidence in EOS’s technological advancements and market potential. To further enhance its supply chain and manufacturing capabilities, EOS signed a Memorandum of Understanding in November 2024 with Wabash National Corporation, a leading manufacturer of advanced engineered solutions for the transportation, logistics, and distribution industries. This partnership is expected to improve EOS’s supply chain efficiency, enabling the effective and reliable delivery of large-scale battery energy storage systems (BESS) across the U.S. High-Profile Contracts and Strategic Collaborations EOS continues to expand its market presence through significant partnerships and contracts. In December 2024, the company secured a 400 MWh order with International Electric Power to enhance resilience for a project at Marine Corps Base Camp Pendleton in California. This follows a 216 MWh order with City Utilities, underscoring EOS’s growing influence in critical energy markets. EOS also announced a 400 MWh project in Puerto Rico and signed a 5 GWh Memorandum of Understanding with Frontier Power to support long-duration storage deployment in the United Kingdom - early signals of growing global demand. Additionally, in December 2024, EOS and FlexGen Power Systems announced a Joint Development Agreement (JDA) to create America’s first fully integrated, domestically produced BESS. This collaboration combines EOS’s Z3™ zinc-bromine batteries with FlexGen’s HybridOS™ Energy Management System (EMS) to deliver comprehensive energy storage solutions tailored for long-duration applications. The partnership targets a combined pipeline exceeding 50 GWh and positions EOS to deliver fully integrated, domestic LDES systems at utility scale. Infrastructure Expansion and Leadership Enhancement To meet the increasing demand for American-made energy storage solutions, EOS received preliminary approval to construct a 181,000-square-foot facility on a 28-acre site at the former U.S. Steel Duquesne Works, located within the Regional Industrial Development Corporation (RIDC) industrial park along the Monongahela River. This facility, part of the Mon Valley expansion under Project AMAZE, will house new manufacturing lines dedicated to producing EOS’s advanced zinc-based energy storage systems. Separately, EOS has announced plans to further expand its manufacturing capacity beyond the Mon Valley project, positioning the company to scale production significantly and solidify its leadership in the growing LDES market. The recently ordered second Z3 manufacturing line will be housed within this facility and marks a key milestone in the company’s multi-line scale-up strategy. In alignment with its growth and innovation objectives, EOS is expanding its leadership team. In December 2024, Francis Richey was appointed Chief Technology Officer, bringing decades of experience in battery technology to advance EOS’s zinc-bromine systems. The company also welcomed David Urban to its Board of Directors, whose expertise in government relations and public policy will assist EOS in navigating complex regulatory environments and capitalizing on opportunities created by the Inflation Reduction Act. Market Position and Future Outlook With endorsements from influential organizations and robust federal and state support, EOS is well-positioned to capture a significant share of the fast-growing LDES market. Experts estimate that LDES could deploy 1.5 to 2.5 terawatts of power capacity globally by 2040, representing an investment of $1.5 to $3 trillion. As the only player in the LDES space capable of scaling large utility orders with fully domestic infrastructure, EOS is poised to lead the market’s next phase of growth. EOS reported Q1 2025 revenue of $10.5 million - a 58% year-over-year increase - and reaffirmed full-year guidance of $150 to $190 million, a projected tenfold increase over 2024. As of its first-quarter 2025 financial statements, the company reported a commercial pipeline valued at $15.6 billion (±60 GWh) and an order backlog of $680.9 million (±2.6 GWh) - a notable increase from the prior quarter and a clear sign of accelerating commercial traction. EOS also booked $9.2 million in new orders during the quarter, including two additional customers, and noted that year-to-date shipments have already exceeded total deployments for all of 2024. In total, EOS now tracks over $29.1 billion in commercial activity across 115 GWh, spanning pipeline, backlog, MOUs, and executable near-term opportunities. This scale, combined with the company’s Tier 1 bankability rating, DOE loan guarantee, and U.S.-based manufacturing platform, gives EOS a strategic position unmatched among non-lithium storage providers. Beyond renewables and utility-scale storage, EOS is seeing growing interest from data center operators seeking multi-hour, zero-augmentation storage for mission-critical uptime. The Z3’s low degradation, high cycle rate, and stable long-duration performance make it well-suited to this sector, where power availability is becoming as critical as raw computing power. Standalone storage applications - including peak demand reduction, grid flexibility, and resilient backup power for industrial operations - represent a growing share of EOS’s opportunity pipeline. With Line 2 on track for 2026 and project deliveries accelerating, EOS is now executing against one of the largest utility-facing order books in North America - and entering its first year of scaled commercial operations.