I first posted this on April 9th on a couple of online forums. I don’t think I posted it here on MF…not sure why. Anyways, I am sharing this now, because:

- It is still very relevant

- I am writing a follow up, specifically focused on FCF (free cash flow).**

So here goes. Let’s discuss…

Over the past 15 months or so, it has been increasingly clear to me that investors are looking for answers on how to juice their portfolio returns….and….they are getting some pretty bad advice.

2020 and 2021 were relatively easy pickings in the tech and growth markets. Buy the leading stocks and ride them higher. If you had any FOMO, then just BTFD and YOLO your way to the bank. I am sure you have, by now, seen a Tik Tok video of this young couple that advises “just buy a stock…wait for it to rise…and then sell it when it is higher…that’s it…simple way to make money”. It just works, bro.

But then on Dec 15th 2021, when the US Feds announced their intention to start raising interest rates to tackle rising inflation, all bets were off.

Growth investors start falling behind

I have been tracking how growth investors like me continued make a series of missteps since the beginning of 2022, hoping that it would not be “too bad”. Hoping for a quick turnaround in inflation and US Fed thinking. Hoping that market tantrums would encourage them to pivot earlier. Hoping that our favorite companies were more resilient. Lots of hope and hoping…but as we know, hope is not a good investing strategy. Growth investors started falling behind…

Ignore the macro

Many growth investors have not been through an interest rate hike regime. I was in middle school when Paul Volcker was doing his thing (1979 - 1982), but I was actively investing during subsequent FOMC rate hike and cut cycles. They were quite instructive for both the bulls and the bears. One had to be aware of the broader impacts that interest changes would have on the economy and the specific impacts to our stocks and their industries.

In early 2022, growth investors kept telling each other three things:

- Just ignore macro because we cannot control it

- Continue investing in “mission critical” growth stocks because this too will pass

- Don’t worry about valuations because our growth stocks are measured differently

Macro is like a snow storm. It might start with small flurries, making everything look all white and pretty. But it builds up and builds up and soon you have 12 inches of snow outside your home, the world becomes as cold as an ice-box and the roads get dangerously slippery.

“Mission critical” gets thrown out the window when a customer’s CFO has to make hard budget decisions. If the business is slowing down, if it is harder or more expensive to get funding in the public market, then cash preservation is the first step that a prudent C-level team will take.

And valuations…oh valuations. Valuations are in the eye of the beholder. If you think a stock is cheap or expensive, you can always find a valuation metric that supports your POV. The problem is when that valuation is based on historical data or ignores the future macro impacts to a company’s top line (revenues) and bottom line (earnings). This resulted in growth investors paying more for stocks that were worth less, based on where the economy was heading.

I never really bought into the mission critical argument, however my biggest mistakes here were TWLO and ROKU. Ignoring how the macro was shifting under their business models and not paying attention to their valuations resulted in a -48% and -60% loss respectively.

Expanding margins and cash flows

By the middle of 2022, we all realized that the Powell FOMC was serious about tackling inflation. They had to be. They had no other choice. Inflation kept rising and peaked at 9.1% in June 2022. The US Feds kept raising interest rates mercilessly.

Suddenly, growth investors heard that companies with expanding margins and increasing cash flows might be better investment opportunities. These companies may not need to raise additional funding in 2022 and so the hunt was on for these unicorns.

So the mantra now was:

- Continue ignoring macro because we still cannot control it

- Let’s buy companies with expanding margins and cash flows

The problem is that objects in the rear view mirror may appear as they really are. Using only historical data to identify “good” companies with increasing margins and rising cash flows proved to be somewhat faulty.

If you still ignore the macro, then you are not paying attention to which companies will be able to sustain their margins and cash flows over the next 12 months. So you buy a stock based on their fabulous past performance only to be disappointed when they publish their next earnings report. In this regard, I faltered on UPST, SNAP and MGNI with losses ranging between -65% and -80%.

TINA, so let’s go to cash

By Oct 2022, growth portfolios were decimated. If we had not sold by then, our holdings were sporting 60, 70, even 80% losses on the books. The despair permeated throughout online investing forums that went quieter and darker. Confusion reigned because nothing seemed to be working.

Growth investors kept hearing that TINA (there is no alternative) to growth stocks. But growth stocks were not doing well. So we just need to go to cash and wait it out. Markets bottomed on Oct 13th 2022. Many investors got scared and sold at these lows. Cash preservation was all the talk.

Very few investors were buying.

Now I was hearing that:

- Markets are not done going lower and there is another shoe to drop

- Staying heavy in cash is better because we cannot find good companies to invest in

Again, they were ignoring the macro signals…they were still focusing on the rear view mirror. Because, this time the data was telling us that inflation was trending lower, the economy was showing early signs of slowing down….that 9-12 months from THEN, rate hikes could be paused.

Don’t believe this 2023 rally

After a bleak 2022, we did not get the highly anticipated Santa rally in Dec. Over the holiday break, we were left wondering if 2023 was going to be a repeat of the past 12 months. But then on Jan 6th, the Nasdaq said “Hold my beer”. The tech laden index started climbing and kept going higher and higher.

No one anticipated how strongly markets would perform in the first quarter of 2023. What a crazy, good time it was to be a tech investor! Who would have “thunk” that we would wake up on April 1st with the Nasdaq up 16.77% and the SP500 up 7.03%. And who would have expected tech stocks to lead the way higher.

So what did growth investors do?

The general tone amongst investor circles was that:

- This rally can’t last. It will not last

- There is still another shoe to drop. Just look at what happened in 2008, in 2001, in 1990

Many were ill-positioned to take advantage of this rally. Early data indicates that most of this Q1 rise was likely due to funds, retail investors and trading algorithms being underweight tech and even being actively short tech.

Many others were too scared to believe that this rally could last, having been scarred from their 2022 experience.

The present: Treasuries, dividend stocks, Gold and GAAP

And so my friends, we come to the present day. I am now seeing a few new trends developing.

- There has been a rush to treasuries and money market funds…for their guaranteed 4-5% returns

- More investors are looking at dividend stocks to secure ongoing cash returns from these companies

- Gold is all shiny again and advertising for gold coins is on the rise

- Good ole’ GAAP accounting is becoming more fashionable

Now, I am all for putting a portion of one’s portfolio in steady return holdings like treasuries and dividend stocks. In fact, I am doing something similar. And I have always used GAAP accounting because it can be consistently applied across companies and it is less fungible by management teams that often will use adjusted metrics to color the earnings report in the manner of their choosing.

However, leaning heavily into conservative investments will leave growth investors further behind as we continue through 2023 and into 2024.

We know that the US, and likely the world, is heading towards a recessionary slowdown. We don’t know how long or short or deep or shallow it will be. We might already be in a recession and not know it (yes, that has happened before) because most macro economic reports are based on lagging data that is about a month old (sometimes more).

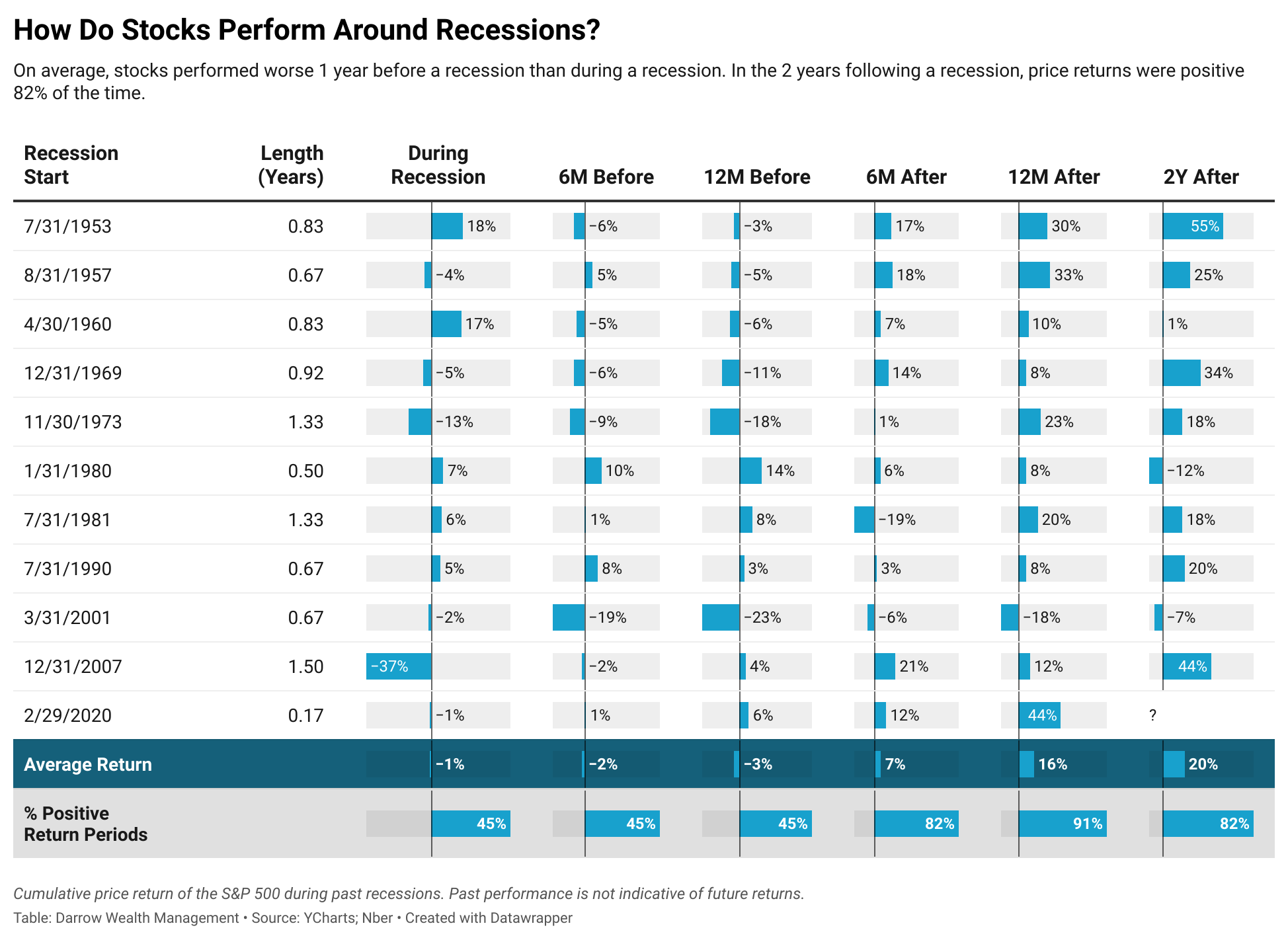

Yes, markets usually do not perform well in a recession. However….and this is a big however…

…as the economy works its way through the slowdown and onto higher future GDP growth, some industry sectors will do better than others, some stocks will do better than others…

…as Jim Cramer says, “There is always a bull market somewhere.” And that is true even when the economy is slowing down.

New investor habits

Now in 2023, we need to develop some new investor habits:

- Be an investor, not a trader

- Don’t get intimidated to learn about macro trends and data…consider them in a daily life, common sense framework

- Understand the layers of markets, sectors and stocks, including how each of them can move in different directions

- Focus on how specific sectors and, more so, specific stocks could perform 9-12 months after rate hikes are paused

- Look past the management speak, flashy press releases and investor presentation slides and go straight to the numbers and the tables

- Use consistent business fundamental metrics across all the companies you are researching and learn to distinguish between leading and lagging indicators

- Fine-tune and broaden your intake of fin media and fin twit…get out of your echo chamber and read diverse opinions

Final thoughts

I believe that 2023 is going to be a fantastic opportunity for savvy investors who make the right moves. Take a look at the table below from Forbes and Darrow Wealth management.

If we want to secure those juicy returns after the economic slowdown is over, now might be the right time to find the sectors and stocks that will get us there.

Cheers!