Data released by Bank of America Global Research and published in the Financial Times shows U.S. 10-year government bond annual returns by percentage to be in rare negative territory and the lowest since 1788.

“But U.S. Treasurys are down two years in a row. The last time that happened was in 1959, shortly after Elvis was drafted,” reports the FT. “An absence of dead-cat after a greater than 5% annual loss last happened in 1861, the outbreak of the US Civil War, while three consecutive down years has never happened.”

1 Like

Headline investing.

Hummm

I don’t know. I really don’t. But, not knowing rarely keeps me or anyone else from pontificating on the internet.

Let’s think of this from a Macro perspective. Using my super simple three inputs macro model, (An economy needs three things in balance to function well, energy, labor and capital. In today’s world these are represented by, wages, oil prices and interest rates) We look at the economy and see that oil is almost in balance. The end of Covid and the beginning of the Ukraine war had it out of balance, but it seems to be returning to balance. Labor is tight, and demographics in the northern hemisphere indicates that it will remain tight for a while. (In the short term India will provide a lot of labor, in the longer term, as far as I can peer into the future, Sub Saharan Africa will provide labor.) This tightness in labor tends to throttle the maximum growth in the economy. Moreover, the tightness in labor is due to an aging workforce.

Now, this aging workforce has another attribute, in addition to high productivity, it tends to have capital. (Children are expensive) This large pool of capital is what concerns me about bonds.

In other words, a large pool of capital looking for work to do in a labor constrained economy should tend to cap interest rates and support the face value of bonds.

Moreover, as we may be seeing a large growth in capital light industries, the demand for capital may be low. This also drives interest rates down and bond prices up.

There is one large capital expense the economy is facing in the near term. It is disruptive and the other end of the disruption is not foreseen. The build out of battery manufacturing. Using some numbers from the latest Honda battery plant build that is started in Ohio, it appears (If anyone wants to check my math, ping me and we can go over it, recommended) that to build all cars using batteries, we need to spend a little under 1 trillion dollars to build battery factories. This actually doesn’t seem like that much and I am not sure it will create a large enough demand for capital to soak up

all the capital available.

So, today may indeed be a decent time to invest in bonds, or bond like investments.

Cheers

Qazulight

6 Likes

Headlines from a shop Cramer started, at that.

Steve

Well reasoned. I gave you a rec. ![]()

The large pool of USD capital in China from their tremendous positive trade balance was the reason for suppressed long-term bond yields in the 2000s, which Fed Chair Alan Greenspan called “a conundrum” since he expected them to rise. Both China and Japan became huge investors in long-term U.S. Treasuries.

On the other hand, our future bond market will be flooded with a gigantic quantity of U.S. Treasury debt due to increased federal deficits. The U.S. faces a challenging fiscal outlook according to CBO’s extended baseline projections, which show budget deficits and federal debt held by the public growing steadily in relation to gross domestic product over the next three decades. In CBO’s projections, federal deficits over the 2022–2052 period average 7.3 percent of GDP (more than double the average over the past half-century) and generally grow each year, reaching 11.1 percent of GDP in 2052. In CBO’s projections, debt as a percentage of GDP begins to rise in 2024, surpasses its historical high in 2031 (when it reaches 107 percent), and continues to climb thereafter, rising to 185 percent of GDP in 2052.

Since 2009, the Federal Reserve has bought a large percentage of federal debt, along with Japan and China. That suppressed Treasury yields. Now that the Fed, China and Japan are all reducing their books of Treasuries (selling more than they are buying)…who will buy the future Treasury debt?

Free bond market buyers can’t create fiat money out of thin air like the Fed. Supply will begin to exceed demand. Bond yields will be forced upwards.

I’m also dubious that inflation can be controlled in the long term due to excess fiscal stimulus from government spending.

Because of this, I will only buy TIPS in the future, not plain Treasuries. I have watched the TIPS yield for many years and bought heavily in October 2008 when the 10 year TIPS yield was 3% + inflation. That has not happened since. When they matured in 2018 it was impossible to replace the yield at equivalent safety. I wished then that I had bought 30 year instead of 10 year bonds, but who knew that the Fed would suppress long-term yields for so many years?

Today, secondary market TIPS up to 2025 are yielding 2% or more. The 10 year is yielding 1.6%. This is based on the bond market’s 10 year inflation expectation of 2.22%. The bond market clearly has confidence that the Fed (and demographics) will keep inflation down.

TIPS principal fluctuates with prevailing interest rates if sold before maturity, like any other bond. The longer the duration, the greater the fluctuation.

I may ladder some TIPS up to 2025. If the 10 year yield rises to 2% I would buy 10 year TIPS.

Note that I-Bond principal does NOT fluctuate with prevailing interest rate the way that TIPS principal does. An I-Bond can be redeemed for full principal from 1 year to 30 years.

I do want to buy some stock during the recession in 2023 or 2024 so I don’t want to lock up all my money in bonds.

Wendy

3 Likes

It is too early still to know if the JPY and EUR will peak much higher with a spirally trade to sell US paper. If that really gets under way before the end of March then there will be a small window of very rich bond yields before the FED and US Treasury buy the long end of the yield curve.

Meanwhile you have little to lose by wait? Wendy has the pulse of this better than I do. I am just looking for the crisis.

1 Like

I generally respect the CBO, so I am not dismissing them, also, I believe the FED will attempt to hold inflation to 2 percent. If the CBO is correct and the FED succeeds, then we will see higher interests rates than we have seen.

But. (I had a friend tell me that “but” after a statement means that I meant none of the statement.)

There is the possibility that the CBO is wrong and the FED will miss its targets and interest rates will not rise.

How?

Well. . . demographics. It comes back to the labor constraints world wide in the economy. Specifically in the lower income sectors. Most skilled craft labor cannot be offshored, the skilled craft labor we have been importing from Mexico is drying up. Worse, the imported labor from central america, small as it is, is being consumed at the factories in Mexico, and the labor that does get through generally has less craft skills than the Mexican labor.

This means all craft labor in the U.S. is going up in cost. In general a lot of manufacturing labor is also rising in cost. This rising cost for labor at the low end has a profound effect on the velocity of money. The federal tax system mostly taxes the movement of wealth, not wealth itself. This is different for state and local governments as the have property taxes which is a tax on static wealth.

I believe that this increase in velocity of money will have two profound effects that we have not seen in a very very long time. It will dramatically increase income and Social security tax revenue and it will make taming inflation very difficult.

There are some large counter cycle things happening, so I cannot say down at this level of detail what will happen.

Those counter cycle things are AI, cloud computing (yes it still matters) and EV’s.

While AI may have the largest impact, I am

too much of a simpleton to attempt to evaluate it. EV’s on the other hand are starting be analizable.

The other day I ran a projection that was pretty amazing (If I did not miss a decible point) That was the entire capital cost of all of the battery factories need to build all of the light cars an trucks in the world as EV’s could be paid for with $10,000 per vehicle premium for 1 years worth of production.

My projection was that the capital required for all the battery plants needed was under 1 trillion dollars! Spread out over 5 years, this would be a premium of only $2000 dollars per car for 5 years. When you think what the economic value of the EV really is, (another long subject) $2000 per EV for 5 years is negative cost.

In other words. . .

EV’s are a large deflationary force. Even with a trillion dollar capital cost for battery plants!

Here is a question for you.

In a deflationary environment 5 years from now, would I be happy holding TIPS bought today? Or would I be happier holding 30 year treasury bonds?

Cheers

Qazulight

5 Likes

Hi Wendy,

If the interest rates rises for one more time, and the Fed pauses, but no rate cuts…

-

Would it make sense to buy just a 1 year treasury directly from the Treasury direct? or even 3 month Treasury bill? I guess the Principal is safe, and we get a reasonable yield while waiting for things to settle.

-

Am I right in assuming that TIPS would also have a similar pathway? I guess the principal value fluctuates but if one holds it, for say a few years, and assuming the FED cuts rates even in 2024, wouldn’t the principal go inversely higher and the yields fall? Does the yield of the TIPS we buy fall in that scenario or does that stay at the same yield we bought it for, while only the principal value increases.

-

Is there any laddered treasury bills that you buy in a regular fashion? If so, could you please explain how yo do that and how that works.

Thanks again,

Charlie

1 Like

@Inspired2learn:

If the interest rates rises for one more time, and the Fed pauses, but no rate cuts…

- Would it make sense to buy just a 1 year treasury directly from the Treasury direct? or even 3 month Treasury bill? I guess the Principal is safe, and we get a reasonable yield while waiting for things to settle.

Wendy: Because the Fed has announced that they plan to raise the fed funds rate to 5% in early 2023 it would probably be best to put the cash into a money market fund that is yielding near 4% but will rise as rates rise. Even the Fed doesn’t know how high they will have to raise rates to control inflation. They have raised their estimates at every meeting since early 2022.

Inspired2learn:

2. Am I right in assuming that TIPS would also have a similar pathway?

Wendy: Yes, TIPS always yield less than the equivalent Treasury and move in parallel. The difference is the expected inflation rate. If inflation is higher than expected then TIPS will yield more.

Inspired2learn:

I guess the principal value fluctuates but if one holds it, for say a few years, and assuming the FED cuts rates even in 2024, wouldn’t the principal go inversely higher and the yields fall?

Wendy: The yield of a TIPS is set when you buy it. It won’t change over time. But the principal value will change (like any bond) depending on prevailing yields. If the Fed cuts rates in 2024 the principal value of the TIPS will rise.

Inspired2learn: Does the yield of the TIPS we buy fall in that scenario or does that stay at the same yield we bought it for, while only the principal value increases.

Wendy: The coupon yield stays the same but the interest you earn rises as the principal rises with the CPI.

Inspired2learn:

3. Is there any laddered treasury bills that you buy in a regular fashion? If so, could you please explain how yo do that and how that works.

Wendy: I do construct a bond ladder with bonds that mature in sequence over time. I have done this for many years. I keep a spreadsheet listing the bonds to keep track of when they will mature.

Wendy

3 Likes

Thanks so much. That was super helpful.

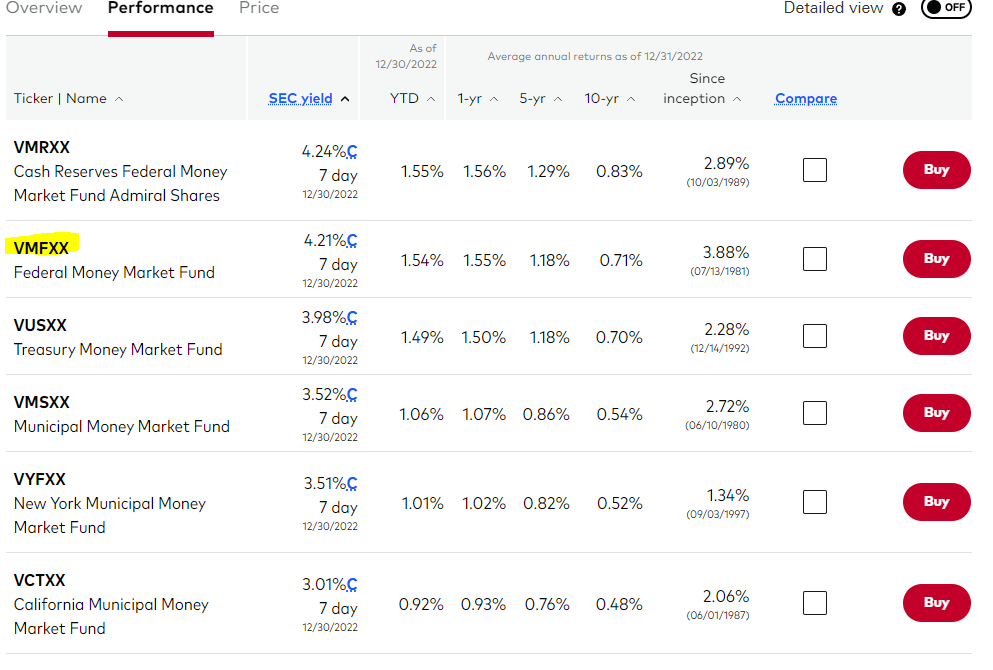

So, for Vanguard money market funds, if one invests in VMFXX, would that mean we get a yield of 4.21% per annum, which fluctuates in parallel (directly proportional) with the Fed funds rate…

The principal value of TIPS also rises with inflation, and the inflation part of the increase is taxable in the current year of increase despite not receiving that amount in cash (this is typically called “phantom income”).

2 Likes

This is interesting in public finance a higher level course in 1989 the professor put forth the idea that the national debt doubles every four years. And had been doubling like that for a couple of decades. It is normal was the jist of his lesson.

The interesting part perhaps is the over taxing in the 1950 to 1960 period when the debt load dropped. The problem being lower yields on the long bond made up the pension fund assets on hand, and longer term at that. Ruinous by the 1980s. The country’s corporations were insolvent in reality funding the pension liabilities against a rising inflation. In other words the 1950 to 1980 demand side econ period no matter how great was fiscally planned inside out.

If the issuer does not go broke and the buyer holds to maturity he/she/it/14-more-pronouns gets what he/she/it/14-more-pronouns bargained for. In other words, timing bonds is only for traders.

The Captain

no longer buys bonds

Back in 1924, almost a century ago, Edgar Lawrence Smith set out to prove the conventional wisdom of the day, that bonds were better investments than stocks. After examining the data he came to the opposite conclusion.

A big thanks to former Fool BuildMWell for pointing out this book

The book stired a lot of controversy, Benjamin Graham, co-author of the Investing Bible, Security Analysis, accused Smith of causing the 1929 stock market bubble and crash.

From Stock Market History from Graham, Buffett and Others pages 62-63

A resentful undercurrent was washing trough the room. Sermonizing on the stock market‘s excesses at Sun Valley in 1999 was like preaching chastity in a house of ill repute. The speech might rivet the audience to its chairs, but that didn‘t mean that they would go forth and abstain. Buffett waved a book in the air. "This book was the intellectual underpinning of the 1929 stock-market mania. Edgar Lawrence Smith‘s Common Stocks as Long-Term Investments proved that stocks always yielded more than bonds. Smith identified five reasons, but the most novel of these was the fact that companies retained some of their earnings, which they could reinvest at the same rate of return. That was the plowback—a novel idea in 1924! But as my mentor, Ben Graham, always used to say, 'You can get in way more trouble with a good idea than a bad idea,‘ because you forget that the good idea has limits. Lord Keynes, in his preface to this book, said, 'There is a danger of expecting the results of the future to be predicted from the past.‘" [emphasis added]

Read books!

3 Likes

Sure - but then keep an eye on the expense ratio - which seems pretty high for a MM Fund. 0.11% is how they take their piece of the action.

'38Packard

It only costs you a quarter or half point to take a very short bond instead of a longer duration. If you think you want the money sooner than later, buy a bunch of 3 month or 6 month paper and just keep rolling it over until the “other” (stock) market is where you want it to be.

It’s better than cash, on which you earn nothing, it’s better than locking up a significant pile for 5 or 10 years when you don’t know what is going to happen in between. It could be inflation, it could be a runaway market, it could be a recession - and all of those seem equally probable at this moment.

You won’t stay even with inflation, but you’ll do better than cash. The other option is to find some stable dividend payers and buy a slug, take the payout, and sell the stock when you find a more attractive opportunity.

(At the moment I’m doing both - lots of short-term bonds, a few heavy dividend payers that I think stable (tobacco, oil, etc.) and I’ll figure out what to do when the dust settles.)

5 Likes

Yield SHOULD BE quoted net of expenses so a MMF yielding 4.21% should actually pay 4.21%.

In other words, that 0.11% expense ratio is largely irrelevant (i.e. what ends up in one’s wallet is all that really matters).

Just clarifying for anyone that may otherwise be confused.

1 Like

Wendy has been mumbling about the Zombie bond explosion - presumed to hit around 2015. I doubt if inflation can drop to 2% within a year - unless the expected recession is much deeper than currently touted.

Regardless, little grasshopper, now is a time for patience as we wait to see what unfolds over the next few months.

Jeff

2 Likes

I want to publicly announce that bonds will stage a record breaking rally this year.

My wife and I took our RMDs from our bond funds yesterday. You’re welcome.

6 Likes

LOL, I often feel the same way after making a trade. Like when I sold my XOM when oil hit $100 last year.

But I suspect that no bond rally will ever even come close to the multi-decade bond rally that began in the early 80s with treasury rates at 14+%. Can you imagine a risk-free return of 14% every single year for 30 years straight???

1 Like

The first year IRAs were made available to most of us I bought a 20-year zero Treasury bond at 14.25%. Sweet.

DB2

3 Likes

Hi Wendy and other METAR members,

I was looking to understand the process of buying AAA graded corporate bonds for the yields while waiting it out in this stock market environment…

I had a query and hope Wendy and others can help clarify.

On the screener, this is what I got for the Corporate AAA rated bonds…

While I am assuming others are equally good, I thought Goldman Sach would be a solid company…and so, if I buy the 11/29/2023 bond, would that mean I get paid a total of 10.19% overall interest for this bond ( 6.33% coupon rate plus 4.86% yield).

Or Am I completely wrong here.

Thanks so much,

Charlie