Hey, fellow investors ![]()

Let’s dive right in.

My Portfolio

The purpose of my monthly portfolio review is to help you understand my investment philosophy, view my current investments, and facilitate mutual learning. I hope this review is helpful to you!

Portfolio performance compared to market

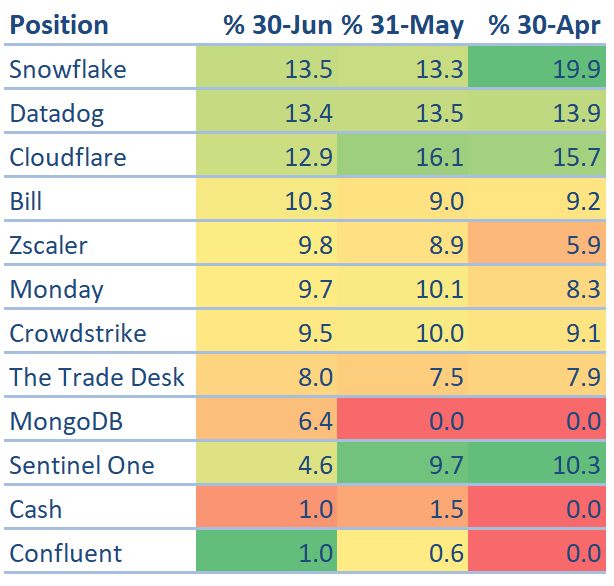

Timestamp: 6/30/2023

Portfolio allocations

Recent changes to the portfolio

This month was more active than usual for me, mainly because I opened a new position in MongoDB and needed funds for that. Additionally, you may notice a small cash position (1%), which I plan to reduce to 0% soon since I typically don’t hold any cash.

Trimmed

- Cloudflare - NET

Once the stock reached $70, I decided to reduce my already large position so that I could invest more in MDB. - Sentinel One - S

After the stock went up to $16, I reduced my position in S by about 30% to allocate more funds to MDB.

Snowflake - SNOW

Like NET, SNOW’s stock price continued to rise ($170), and they wanted to add more to MDB. - Datadog - DDOG

Like NET, DDOG’s stock price continued to rise ($100), and they wanted to add more to MDB.

Added

- Confluent - CFLT

My plan is to increase CFLT to around 5% in the near term, which is why I am adding to it on a monthly basis.

New position

- MongoDB - MDB

I finally reopened a position after monitoring MDB for the past few years due to better-than-expected earnings and a positive outlook.

Company updates

Note: To keep it concise, only companies with noteworthy updates might be included. Absolute numbers relate to last quarter’s earnings release. Metrics are adjusted values (Non-GAAP).

Crowdstrike - CRWD

What they do: Leading cybersecurity firm with a "mission to protect customers from breaches”

Type of revenue: Seat-based (Endpoints)

Cash: $2.9B

TTM revenue: $2,446M

Market cap: $35B vs last month’s $38B

Key Highlights

Revenue

Crowdstrike’s Q2 2023 revenue was $692.6M, 42% year-over-year, and 8.7% quarter-over-quarter beating expectations, but decelerating sequentially.

Net new ARR was $174.24M, negatively surprising the market, but management is confident about acceleration for the back half of the year due to momentum with large customers, record Q2 pipeline, and partnerships.

The remaining performance obligations were $3,315M, negative sequentially for the first time. International revenue is slowly gaining share and growing faster than total revenue at 53% year-over-year.

Outlook

The Q2 revenue guide is $727.4M, suggesting 7.3% quarter-over-quarter and 38.8% year-over-year growth if they keep beating their guide.

The FY2024 revenue guide was raised by 2% to $3,036.7M, with a potential 40% year-over-year growth if they keep raising their guide and deliver a beat in Q4.

The Q2 operating income guide is $123.8M, and the FY2024 operating income guide was raised by 1% to $526.2M. Also, the FY2024 EPS guide has been raised to $2.43 from $2.39.

Cash Flow & Profitability

Subscription gross margin increased to 80% due to investments in data center and workload optimization.

Operating income was $110M (16% of revenue), up from last year’s $83M. Net income was $136M (19.7% of revenue), up from $75M. Earnings per share increased to $0.57 from $0.31.

Operating cash flow increased to $301M (43.4% of revenue) and nearly half of the revenue generated cash flow. Free cash flow increased to $227M (32.8% of revenue).

Next quarter, we should expect lower cash flow due to the usual seasonality in Q2 and this year management expects to see more pronounced seasonality but maintains the target of achieving 30% free cash flow margin for the fiscal year.

Crowdstrike reached GAAP profitability for the first time in its history with $0.5M net income, compared to a loss of $31.5M the previous year. The biggest factor for this achievement was the modest growth in stock-based compensation.

Customers

Unfortunately, we cannot see the quarterly development of customer growth since Crowdstrike is moving to annual reporting for new logo metrics.

The dollar-based net retention rate was 120%, down from 125%.

Customers using 5+ modules was 62% (stable), 6+ modules were 40% (up from 39%), and 7+ modules was 23% (up from 22%), indicating vendor consolidation and customer’s wanting more of Crowdstrike.

The gross retention rate remained high and best-in-class.

Notable Developments

Multiple future growth drivers have been mentioned:

First , a compelling partnership with AWS to develop powerful new Generative AI applications that help customers accelerate their cloud, security and AI journeys.

Second , the Impact Level 5 Provisional Authorization from the Department of Defense to sell more products into the public sector.

Third , the sustainable advantage as three mega-trends continue to unfold, AI, consolidation, and cloud:

AI

CrowdStrike believes that large language models (LLMs) are only as good as the data on which they are trained, and their unique dataset spanning petabytes and capturing trillions of new events daily from their global fleet of sensors, combined with over 10 years of attack data and threat graph, creates a sustainable data advantage yielding better models, automation, and outcomes in the rapidly growing adoption of generative AI within cyber security.

Moreover, Crowdstrike anticipates that the utilization of LLMs will decrease the difficulty for malicious actors to generate advanced cyber-attacks. This, in turn, will be a catalyst for demand for contemporary cybersecurity technologies such as Falcon.

Lastly, Crowdstrike has introduced Charlotte AI , a generative AI security analyst that uses high-fidelity security data and is continuously improved through human feedback. Charlotte AI aims to provide faster results, better security outcomes, and lower costs, and will benefit from a continuous human feedback loop with CrowdStrike’s OverWatch, Falcon Complete, and Intel teams.

Consolidation

The current macro environment has increased the need for customers to reduce vendor sprawl, agents, and costs, while protecting their businesses with a best-in-SaaS platform. Falcon offers over 200% ROI for enterprise customers, making CrowdStrike a popular choice for businesses looking to protect and drive efficiencies.

Cloud

The exploitation of cloud services has increased by 95% YoY, and the number of threat actors operating in cloud environments has increased by 288%. Securing cloud assets is crucial and will continue to grow in importance. Crowdstrike is well-positioned to meet this need.

Competition

CrowdStrike’s competitive environment has remained unchanged since April, with enterprise customers choosing CrowdStrike over Microsoft 8 out of 10 times during testing and strong win rates across all competitors in the quarter.

Dilution & Valuation

Dilution increased by 4% year-over-year to 241M diluted shares outstanding. Management expects 242M in Q2, which continues the upward trend. However, for a healthier development for shareholders, it would be ideal to see this increase go back to around 2% year-over-year. Management has mentioned that they aim to keep it under 3% this year.

Crowdstrike is richly valued at an EV/S of 11, but still below the average (13) of the top 10 SaaS company multiples in Jamin Balls’ valuation list for high-growth stocks.

Investment Decision

It’s good to see that my hypothesis from last quarter seems to be holding up so far, with sequential revenue growing at 8.7%.

From my March 2023 summary:

Here is my thesis: Crowdstrike has a seat-based subscription model. I interpret the stabilization of sequential metrics as a slowdown in layoffs, which is good for seat-based subscription model businesses like Crowdstrike, indicating the endpoint market is not saturated and the market has stabilized.

However, this does not mean we should expect further quarter over quarter acceleration, as businesses are not currently hiring more. So, I assume we’ll see minimal beats for another 1 to 2 quarters and possibly acceleration again in Q3.

I believe assuming Q1 revenue of $690M, 8.3% quarter over quarter growth with a 1.7% beat is realistic and “prudent.” I try to make conservative assumptions (and if these sound too conservative, it’s time to trim) - the last thing I want is a negative surprise every quarter.

I also assume Crowdstrike will achieve around 40% revenue year over year at the end of FY2024 (with some luck), more would be very optimistic.

While the actual top-line results were mixed due to weakness in RPO and net new ARR , the outlook appears positive. Management’s confident tone and multiple raises from revenue to profitability guides support this view. If the macro environment starts to improve, we might even see 40% year-over-year revenue growth.

The profitability across the board is great, especially considering the impressive operating cash flow margin of 43%! Achieving GAAP profitability for the first time is a significant accomplishment.

The decline in DBNRR was expected due to macroeconomic factors negatively impacting sales. Despite this, it’s great to see customers still buying more modules .

The partnership with AWS , the Impact Level 5 Provisional Authorization , and positioning for megatrends (AI, Consolidation, and Cloud) with no change in competition indicates sustainable growth ahead.

Dilution (4% YoY) is higher than I prefer, but management is keeping an eye on it. The valuation at an EV/S of 11 makes sense. Given its strong performance, tailwinds, and runway ahead, I believe the stock is reasonably valued.

As mentioned in my previous summary, I took advantage of the 10% drop in after-hours trading to increase my allocation from 9% to 10%. I have no plans to make any further changes for now.

Sentinel One - S

What they do: Cybersecurity firm catching up with CrowdStrike

Type of revenue: Seat- and consumption-based

Cash: $1.1B

TTM revenue: $477M

Market cap: $4.4B vs last month’s $4.4B

Key Highlights

Revenue missed Sentinel One’s own Q1 guidance by 2.6%, coming in at $133.4M, up 70.5% year over year, and 5.8% quarter over quarter.

During the earnings call, management explained the miss due to customers generating less consumption-based revenue . Unfortunately, that’s just one of multiple issues.

Revenue guidance for FY ‘24 was reduced to $600M from the previously guided $679M. This was shocking, as a slight raise was expected instead. Last quarter, I expected them to achieve 60% at the end of the year, but now I’m thinking they might achieve 50% at best.

Revenue guidance for Q2 of $141M was lower than expected, but still implies a slight sequential acceleration from 5.8% in Q1 to 6.8% in Q1 considering a 1% beat. Note: Q2 revenue will likely slow down to 39% year over year due to tough comps versus previous years’ Q2, when they acquired Attivo.

But how can I expect a beat next quarter, while they’ve just missed the revenue guide for Q1?

Let me explain:

Net new ARR was lower than expected at $41.6M, up 40.1% year over year, but down 29.5% quarter over quarter. The sequential decline in net new ARR is likely due to seasonality. However, the real issue lies in their historical methodology for tracking ARR.

ARR guidance for FY ‘24 has been reduced to $522M, representing a 35% YoY growth, down from the previously guided 41%. This reduction in revenue is a real bummer.

In the last quarter, I noted:

“CFO Dave Bernhardt couldn’t help highlighting multiple times how conservative that forecast is. I try not to read too much into it, though he seemed really eager to convey how low that guidance is. I’d like that, but his last mistake guiding to 50% ARR growth 90 days ago makes me wary.”

Unfortunately, the guidance is even lower now.

Four Reasons:

-

In recent years, management has observed a steady increase in usage and consumption patterns by their large customers, which accounted for real-time and quarterly ARR. However, during the first quarter, they experienced a noticeable decline in usage, which continued in May:

As a result, management saw a shortfall in revenue during Q1 and conducted a deep dive into their customer base. During the investigation, they discovered that excess consumption-based revenue was included in the ARR calculation. “Excess” refers to the additional amount that customers have to pay if they consume more than what was contractually agreed upon.

This consumption-based revenue makes up to 5% of total revenue and is generated from data ingestion, the security data lake, and the data set consumption products.

The issue: They should have never included the excess consumption-based revenue into ARR, since ARR means “annual recurring revenue,” which consumption is not. Due to the volatility in consumption (similar to Snowflake’s or Datadog’s), the revenue guides were honest but fell short.

To reduce ARR volatility from changes in usage-based consumption and better align ARR with revenue, management decided to change the methodology for calculating ARR for consumption and usage-based agreements to reflect committed contract values.

The bright side: Once customers consume more than what was agreed upon in the contract, there may be an additional upside in revenue beats surprising investors. -

While conducting the deep dive, management also discovered and corrected some historical recording inaccuracies relating to ARR classifications of certain contracts that they identified during the ARR review. An error in their CRM added renewals on top of upsells, which should now be fixed and not happen again.

-

Macroeconomic conditions have impacted deal sizes and sales cycles. Budgetary scrutiny has resulted in deal size adjustments for new customers and renewal contracts, as is happening in other businesses facing similar challenges.

-

Management was disappointed by some execution challenges in the late stages of contract negotiations for large deals, which caused a few deals to slip to the next quarter. They highlighted a multimillion-dollar deal with a customer who had already fully deployed Sentinel One’s solution but could not close the deal in Q1 due to contract delays.

Overall, the change in methodology and correction resulted in an ARR reduction of $27 million or approximately 5% of total ARR as of Q4 FY23, as well as a comparable estimated adjustment to the remaining quarters in the fiscal year 2023.

Unfortunately, the reduced revenue guide has pushed the target to break even from Q4 FY2024 to FY2025. However, progress toward profitability remains on track:

The Q2 operating margin guide has improved to -36%, up from -57% in Q1 2023, and remains on track. The FY ‘24 gross margin guide has been slightly raised from 74.5% to 75%, and the FY ‘24 operating margin guide of -25% remains unchanged.

To achieve these targets, Management announced a plan to optimize their workforce that is expected to impact around 5% of current employees and affect future headcount growth plans.

Margins and cash flows have improved across the board:

- Gross margin has increased to 75% from 68% last year.

- Operating loss was -$50.76M (-38.1% of revenue), which matched my expectation and is a strong improvement from -$57.44M (-66.1% of revenue) a year ago. The smaller loss resulted from revenue growth exceeding the increase in expenses. It’s also worth noting that Q1 is usually their weakest quarter for profitability due to front-loaded expenses.

- Net loss was -$42.25M (-31.7% of revenue), up from -$56.98M (-72.8% of revenues).

- Operating cash flow was -$28.06M (-21% of revenue), up from -$49.35M (-63.1% of revenues).

- Free cash flow was -$31.43M (-23.6% of revenue), up from $54.73M (-69.9% of revenues).

Sentinel One continues to invest aggressively in Sales & Marketing , accounting for 63% of its revenues, to capture market share. This indicates that they are not scaling back their go-to-market efforts as they pursue profitability.

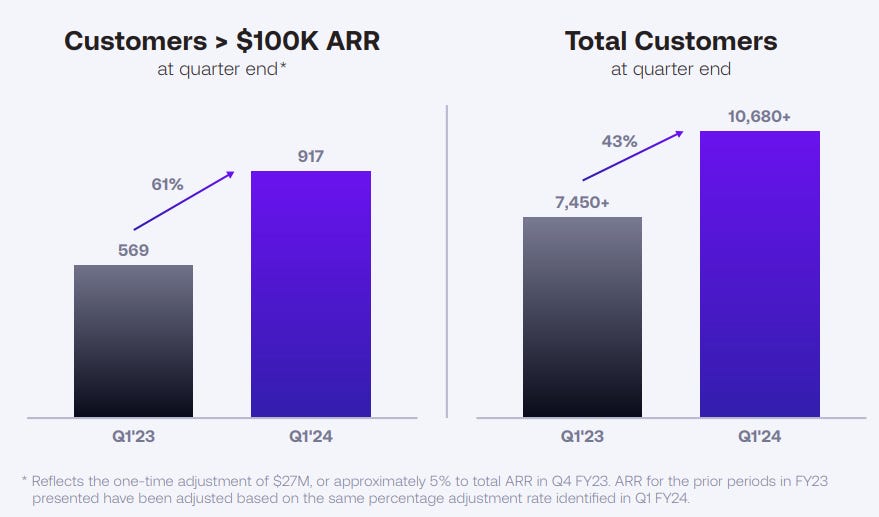

Looking at customers, Sentinel One added 680 customers, bringing their total to 10,680 , which is a 43.4% increase year over year and 6.8% increase from last quarter. However, this quarter’s growth rate slightly decelerated compared to the previous quarter.

More important is the progress in customers spending more than $100k:

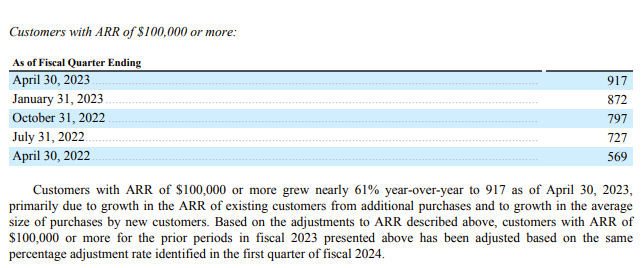

In Q1, Sentinel One added 45 net new customers of the $100k cohort, bringing the total to 917. This represents a 61.2% increase year over year and a 5.2% increase sequentially.

Unfortunately, I can’t compare Sentinel One to Crowdstrike , as Crowdstrike no longer reports customers and never reported a $100k cohort.

Comparing the performance to other software businesses with a $100k+ customer cohort:

- ZScaler added 95 net new adds (4.3% QoQ ) vs 140 net new adds (8% QoQ) a year ago. That makes the development look solid for Sentinel One since Zscaler shows a similar weakness and the lowest amount of $100k customers in almost 3 years.

- Datadog added 130 net new adds (4.7% QoQ ), vs 240 net new adds (11.9% QoQ) a year ago. The lowest amount of customers spending more than $100k in the past 3 years.

Furthermore, it’s worth noting, Sentinel One added 1 net new Fortune 10 customer , now protecting half of them:

Walmart, Amazon, Apple, CVS Health, UnitedHealth Group, Exxon Mobil, Berkshire Hathaway, Alphabet, McKesson, Chevron.

My takeaway : When considering other companies’ performance in the current environment, customers for Sentinel One aren’t falling off the cliff, but going forward I’d like to see a stabilization or acceleration in growth, soon.

The Dollar-based Net Retention Rate was a solid 128%, but down from 130%+ last quarter. Customers continue to consume less and we can see a decline in that metric for all companies in that environment - like Snowflake or Datadog.

I’m seeing no issues here since a) Management highlighted to be confident in staying above 120%+ and b) the gross retention rate “has essentially been flat for the past eight quarters or so. I don’t think it’s deviated more than 1 point. So one of the things that Tomer had talked about is when customers use us, they don’t tend to leave us” .

Lastly, ARR per customer increased by more than 20 percentage points year-over-year demonstrating success with large enterprises as well as increasing adoption of broader platform offerings.

Notable Developments

Sentinel One has launched Purple AI , which enables users to control all aspects of enterprise security, from visibility to response, with speed and efficiency. Customers and prospects had hands-on access to a live demo of Purple AI at RSA, the world’s largest cybersecurity event, and the feedback was very positive.

Dilution increased by 6.9% year over year, which is much too high. Ideally, I would like to see a maximum annual increase of 2-3%. However, in Q4, they announced that they expect dilution to slow to 5% YoY in FY2024, which is a significant improvement from the previous year.

My Investment Decision

I trimmed slightly on the way up to $17, but I don’t plan to sell further for now.

Here’s why:

Obviously, the CFO made significant rookie mistakes and should be held accountable. Executives left Sentinel One a few quarters’ ago to join Crowdstrike and lowering revenue guidance is also never a good sign. Furthermore, management highlighted deals slipping due to execution challenges. Dilution needs to slow down. That’s a lot of flags!

On the other hand, management has been sincere and upfront about their mistakes. Most importantly, the adjustment to Annual Recurring Revenue (ARR) did not impact historical revenue, total bookings, cash flows, or income statement. Moreover, the ARR for the quarter was in line with management’s expectations, except for the consumption downsizing.

By taking out the excess consumption revenue from ARR, they were forced to take the guide down, which is the right move to reduce volatility. Management highlighted that key factors like competition environment, win rates, and the healthy pipeline didn’t change .

Customer growth isn’t falling off the cliff. In fact, they have even added one of the top 10 largest companies in the US by revenue , and now protect half of them.

Furthermore, the progress to profitability remains on track, although it has been slightly delayed until FY2025. With $1.1 billion in cash and no debt, Sentinel One has plenty of financial runway.

Finally, I found an interesting insight provided by Ivana Spear after talking to Sentinel One’s management: 10% of Sentinel One’s revenue comes from the cloud, which is growing at over 100% growth rates.

I’m taking a calculated bet when considering all the puzzle pieces, including listening to what management said, the low valuation, and the market cap.

I believe the risk/reward looks decent: With a market capitalization of only $4B, and a forward EV/S of just 6, the company is still growing at a healthy pace and has visible progress toward profitability.

I’m controlling the risk part of that equation with the size of my allocation, which sits at ~5%.

- If I’m right about my bull thesis, there is significant upside potential.

- If I’m wrong, I expect to lose another 50%, which means a 2.5% loss for the total portfolio, plus lots of learning. I can live with that.

Some people say that Sentinel One is losing to Crowdstrike, but I wonder if that’s the right question to ask. The cybersecurity market is large enough for everyone, with a total addressable market (TAM) of $100 billion.

Even Microsoft, a leading security provider, has only captured 1/5 of the market, leaving the remaining 80% for other providers. In my opinion, it’s not a matter of Sentinel One versus Crowdstrike. Rather, it’s about how well Sentinel One performs on its own in the future.

Please note: This is not a bullish take on a story that might or might not unfold in the next few years. I have no idea about the future, as I don’t have a crystal ball.

I don’t think I will hold Sentinel One forever since I lack the long-term conviction I have in businesses like Snowflake. I may even trim opportunistically ahead of earnings.

These results would make me to finally sell out:

- Another downgrade of the FY revenue guide

- Not meeting their net new ARR guide

- A sequential slowdown of $100k customer growth, while peers don’t show the same

- No progress on their path to profitability

However, I believe there could be more near-term upside than expected. As usual, please don’t follow me blindly and make your own judgment.

Zscaler - ZS

What they do: Cybersecurity firm that provides services secure user-to-app, app-to-app, and machine-to-machine communications over any network and any location

Type of revenue: Subscription-based

Cash: $1.97B

TTM revenue: $1,480M

Market cap: $21B vs last month’s $20B

Key Highlights

Revenue

Zscaler’s revenue was $418.8M, a 46% YoY increase and an 8% QoQ increase. This met the positive preliminary guidance announced a month ahead of earnings.

Calculated billings were $482.3M, a 39.5% YoY increase and a -2.3% QoQ decrease. This was better than expected and an acceleration from last quarter.

Remaining performance obligations were $3,023M, up 7.6% sequentially, indicating that customers are committing to more future spend.

Management’s ability to execute was aided by their well-performing sales organization and good product. Customers recognized the ROI by simplifying their network.

10 out of 13 analysts congratulated management on the impressive results.

My take: Zscaler continues to deliver. Their strategy of partnering with CXOs early on to create CFO-ready business cases appears to be effective.

Outlook

Zscaler’s Q4 guide suggests 7% QoQ and 41% YoY growth if they exceed historical guidance.

For the full year , the revenue guide was raised by 2% to $1,593M, up 46% YoY, calculated billings guide was raised by 1.7% to $1,978M, and the operating income guide was slightly raised to $225M.

My take: Zscaler raised its full-year guidance for all metrics, indicating promising times ahead.

Cash Flow & Profitability

Zscaler achieved a gross margin exceeding 80% for the 11th consecutive quarter, with operating income at $63.9M (15.3% of revenue), net income at $74.6M (17.8% of revenue). Operating cash flow was $108.5M (25.9% of revenue), and free cash flow was $73.9M (17.6% of revenue).

Compared to patterns in previous years, S&M expenses have been cut down the most: $185M, which is 44.1% of revenue. However, there are no concerns here.

My take : The overall profitability remains excellent, with healthy cash flow margins ranging around 20%.

Customers

Zscaler added 95 customers spending more than $100k ARR, 22 customers spending more than $1M ARR , and 5 customers spending more than $5M ARR . Customer growth for the $100k ARR and $1M ARR cohort is decelerating sequentially due to larger deals take longer to close as customers introduce more checks and reviews.

The company serves eight of the world’s largest financial services and diversified insurance companies, outside of China. They also have 40% of the Fortune 500 and 30% of the Global 2000 as customers.

Approximately 60% of new business comes from existing customers, who are spending more: The Dollar-based Net Retention Rate has remained at 125%+, but the company’s success in selling bigger bundles, multiple pillars, and faster upsells within a year may reduce the rate in the future.

The Net Promoter Score of over 70 is a testament to Zscaler’s strong relationship with customers and in Gartner’s peer insight rating, which is a customer survey done by Gartner, Zscaler is the only MQ leader who is in number one in all eight Gartner’s category.

As stated in their earnings call, the focus is on ARR over having a large number of customers. Management still sees a vast upside in their customer base. After understanding this, I’m a bit less worried about the lower customer growth, which I expect to pick up again at some point.

Why it makes sense to focus on existing customers:

Zscaler has a 6x upsell opportunity with its existing customer base for protecting their users.

Management states, when it comes to cyber companies they’re probably the only company that delivers significant ROI, because they eliminate a bunch of point products.

They see customers buy ZIA, ZPS and ZDX - solutions they offer - for every employee happening more-and-more, because customers are seeing the value by being able to remove a bunch of point products and show ROI and that actually gives them more incentive to buy more.

Here’s a recent example:

A fast-growing global bank in the APJ region upgraded to Zscaler for Users bundle, which supports 150,000 users, after deploying ZIA last year. This upgrade significantly reduces the time it takes to open new branches by 50% and eliminates the need for firewalls and MPLS network services.

Zscaler is now a strategic partner for this customer, as they continue to expand their footprint and transform into a cloud-centric organization. The customer stated that it was the first time they had seen a security vendor that understood their business needs and aligned its solution to address them.

With this latest purchase, the customer’s ARR has surpassed $10 million. This is also an example of the geographic diversity of Zscaler’s business outside the U.S.

My take: Zscaler primarily focuses on large enterprises, but currently, it takes more time to close deals, which slows down customer growth. While this is acceptable, an acceleration in sequential growth is expected next year.

On the other hand, Zscaler’s focus on its existing customers makes sense due to the 6x upsell opportunity.

Notable Developments

Using AI, Zscaler has the opportunity to predict most of today’s ransomware and other sophisticated attacks on their customers before they happen. And management plans to launch a number of innovations around AI.

That being said, Zscaler has already started integrating ChatGPT with policy-based access controls to ensure safe use of AI applications for their customers. If employees submit sensitive data to ChatGPT or similar applications, our DLP technology will detect and block it.

Zscaler’s CEO, Jay Chaudhry, commented on his expectation that AI/ML will expand Zscaler’s TAM (total addressable market).

My take: Exciting insights into how Zscaler incorporates AI and how it might become a significant advantage in the future can mean only additional fuel for sustainable growth ahead.

My Investment Decision

Zscaler continues to perform well, thanks to its strategy of partnering with CXOs early on to create CFO-ready business cases. This approach appears to be effective, as indicated by Zscaler’s raised full-year guidance for all metrics.

The company’s overall profitability remains excellent, with healthy cash flow margins averaging around 20%. Although Zscaler primarily focuses on large enterprises, it takes more time to close deals, which slows down customer growth. However, an acceleration in sequential growth is expected next year.

On the other hand, Zscaler’s focus on its existing customers makes sense due to the 6x upsell opportunity. AI may become a significant advantage in the future, which bodes well for the company’s continued success.

Zscaler’s forward EV/S (enterprise value to sales) ratio is 13, which is slightly below the average of the top 10 SaaS company multiples in Jamin Balls’ valuation list for high-growth stocks. Although Zscaler’s valuation is stretched, it appears cheaper than NET, which has an EV/S ratio of 16.

It’s important to note that while I do consider valuation as one factor for investment decisions, it’s not my main consideration.

As I outlined in my previous portfolio summary, I added funds in small increments both before and after the positive preliminary guide with a target allocation of 10%.

Last month, I based my reasoning on the ongoing decline in the stock price. At that time, the valuation had reached a forward EV/S of 8.2, which I considered to be undervalued.

I did not change my already large position in June and plan to hold it for now.

MongoDB - MDB

What they do: Provides a scalable and flexible NoSQL database for storing structured and unstructured data.

Type of revenue:

Consumption-based

Cash: $1.9B

TTM revenue: $1367M

Market cap: $29B

Coming soon: I’m planning to publish my review on MongoDB earnings in my next portfolio review.

Confluent - CFLT

What they do: Provides a platform for managing and processing streaming data.

Type of revenue: Consumption-based

Cash: $1.85B

TTM revenue: $634M

Market cap: $10.5B vs last month’s $9B

Coming soon: I’m planning to publish my review on Confluent in my next portfolio review. Until then, check out my TL;DR version here (Twitter thread).

Already covered

Check out the most recent reviews for my other positions here:

My Watchlist

DUOL, OKTA, IOT, GTLB, NVDA

Closing Thoughts

Keeping it short this month. Just one thing:

Starting to write a monthly portfolio review was a game-changer for me.

Why:

- It allows me to track performance regularly.

- I can dive deep into each company.

- It boosts my confidence, even in tough times.

I encourage you to start your own review.

And don’t be afraid to share it publicly. More puzzle pieces mean better decisions for all of us!

My Previous Portfolio Reviews

Thank you for reading and Happy Investing, everyone!

Twitter: @MoritzMDrews