Hi there!

The portfolio summary for march 2023 has 4 parts:

- How my investments did compared to the overall market

- How my money is invested and how strongly I believe in each investment

- The changes I made last month to invest in new opportunities or reduce risk

- Updates on the companies I invested in and closing thoughts

Disclaimer: This portfolio summary is for informational purposes only and does not constitute investment advice. Everything expressed here is just my personal opinion. I am not a professional, so please don’t follow me blindly as my perspectives could lead to incorrect conclusions.

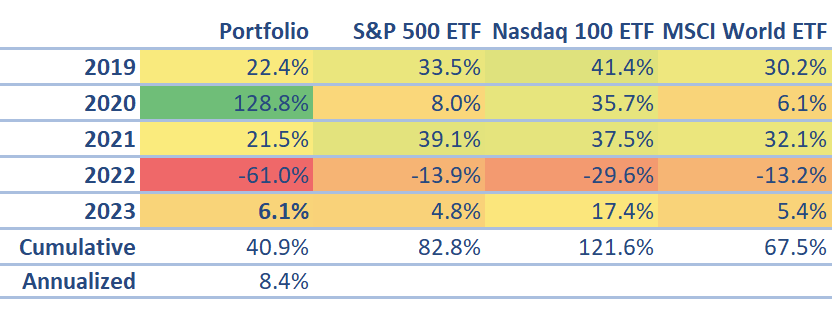

1. How my investments did compared to the overall market

Timestamp: 3/31/2023

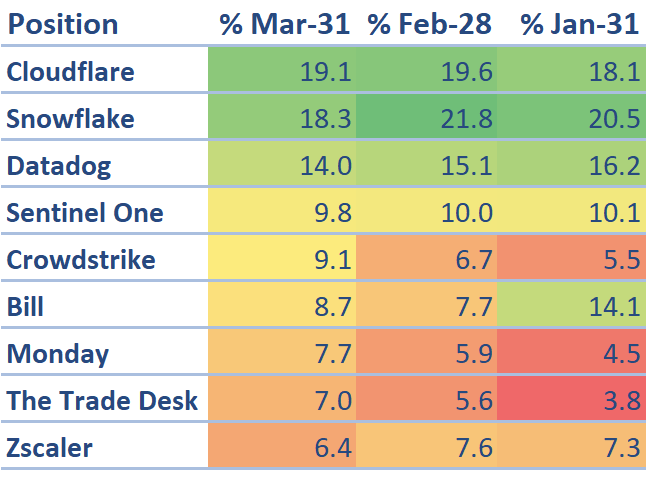

2. My Portfolio

3. The changes I made last month

Added: The Trade Desk

The Trade Desk reported solid earnings in February and I continued increasing The Trade Desk over the month as I planned to raise it to ~7%. The rationale remains the same as mentioned in my previous portfolio summary:

- Gaining market share and outperforming peers (32% platform growth vs 8% sector growth)

- High margins (50% EBITDA margin, 25% free cash flow)

- Large total addressable market ($1 trillion vs $175 billion for linear TV)

- Connected TV tailwinds , Netflix opening, shopper market supporting re-acceleration

Added: Monday

Monday reported solid earnings in February and I kept adding more during the month to increase my position.

Recap:

- Monday was one of the few reporting companies that surprised me positively . Many analysts congratulated them on the quarter.

- Sequential revenue growth stabilizes and the full-year guide looks decent to me when considering the adverse macro effects.

- Though, they expect a further decline for DBNRR by the end of 2023 due to the macroeconomy headwind.

Added: CrowdStrike

I liked CrowdStrike’s confident tone in the earnings call and strong Q4 results, including:

- 47.9% revenue growth to $637.4M, exceeding expectations.

- 20.4% growth in remaining performance obligations to $3.4B.

- 42.9% operating cash flow margin and healthy customer metrics.

- The sequential increase in Net New ARR by 11.9% instead of the projected 10% decline.

I expect revenue growth to accelerate in Q3, as CxOs anticipate tech budgets will increase in 2023, especially for cybersecurity . Though I don’t foresee major revenue beats for 1-2 quarters, growth should pick up by Q3. My confidence increased after that strong earnings report. I increased my position.

Added: DataDog

After markets plunged on March 10 due to fears of another potential banking crisis (SVB), I added DataDog below $65 . I believe Datadog will show accelerating revenue growth in the coming quarters, so at these levels, Datadog seems undervalued.

Recap: Overall, while DataDog’s guidance indicates slower growth ahead, I remain bullish. They continue adding customers at a steady rate and existing customers are spending more. Key metrics still look good. Conservative guidance likely reflects uncertainty, not declining trends. DataDog should see strong growth beyond 2023 due to new products and market opportunity. Though 50% growth may not last, 25% seems too pessimistic. I’ll reassess after Q1 but am optimistic for now.

Added: BILL

I added several times after the SVB incident when the price dropped below $70. I believe that Bill is vastly undervalued at that point, given its forward EV/s of just 7 and small market cap of $8b. When looking at BILL’s projected >50% YoY revenue growth, it provides a decent risk/reward.

4. Company Reviews

Note: To keep it concise, only companies with noteworthy updates might be included.

Absolute numbers relate to last quarter’s earnings release. Metrics are adjusted values (Non-GAAP).

Snowflake

What they do: Provides data storage, management, and sharing for the cloud

Confidence tier: Champion

Type of revenue: Consumption-based

Cash: $5.1B

TTM revenue: $1,938.8M (product)

Market cap: $45B

Thoughts on Snowflake’s customer acquisition and GTM strategy

Snowflake’s primary focus is to acquire the largest enterprise businesses in the world: the Global 2000 .

Why?

Each new Global 2000 customer is worth far more than any other customer. This is due not only to higher revenue potential but to data gravity .

Almost every major business likely works with a Global 2000 customer.

Think of Global 2000 customers as stars in a solar system. The smaller customers, $100K and $1M customers, are like planets orbiting those stars due to the star’s strong gravity. These smaller “planets” need access to the shared sunlight —the shared data— to survive, so they get pulled into that ecosystem: Snowflake’s powerful network effect.

Here’s Snowflake’s development of acquiring Global 2000 customers:

Due to the small total number of very large G2k customers, significant volatility is involved in the quarterly numbers. Snowflake cannot acquire G2k customers at an increasing rate as with smaller customers, of which there are countless businesses worldwide.

Snowflake mentioned G2k customer sales cycles are one to two years, extremely long sales cycles: “They will be lumpy in terms of when we land them”.

Add elongated sales cycles from the current environment on top of that (which G2k customers are also part of, I assume) and they still acquired 19 G2k customers last quarter.

Of course, I would like to see Snowflake gain G2k customers at an increasing rate, but I’m fine with the progress. They consistently continue acquiring those customers, and consistency will pay off long-term.

Noteworthy insights in March

- Forbes released an interesting article outlining how Snowflake benefits from large customers in the long term.

- Battery, a VC firm, published an insightful report on Cloud Spend. Based on that, Data Warehouse Providers like Snowflake should be a top priority in the next 12 months and onwards.

Recap and Conviction

Snowflake reported strong revenue and profitability growth in Q4. Product revenue was $555.3M, up 54.4% year over year. They guided to 6.3% quarter-over-quarter growth next quarter. Full-year 2024 product revenue is expected to grow 40% to $2,705M .

The operating income margin is projected to reach 6% in 2024, representing $173M. The free cash flow margin is forecast to be 25% or $722M.

Customer growth slowed but large customers expanded spending. The net revenue retention rate declined to 158% due to customer optimizations, still best-in-class. Newer customers adopted Snowflake more slowly, slowing overall growth.

Snowflake repurchased $2B of stock and expanded its AWS partnership to better serve customers.

I believe spending on Snowflake’s services can rebound quickly and maintain a cautiously optimistic outlook on Snowflake’s business and growth opportunities despite lowering its revenue forecast for the fiscal year 2024. Quarterly revenue increases can fluctuate due to Snowflake’s consumption-based business model and seasonality.

I see no issues with Snowflake itself and believe its growth thesis remains intact for 2024 and beyond, citing its large scale, strong free cash flow, and continued high growth despite macroeconomic headwinds and tailwinds from digital transformation likely to rebound.

Sentinel One

What they do: Cybersecurity firm catching up with CrowdStrike

Confidence tier: Contender

Type of revenue: Seat-based (Endpoints)

Cash: $1.2B

TTM revenue: $422.16M

Market cap: $4.4B

My Take on the Latest Earnings

Revenue was $126.1M, up 92.1% YoY and 9.4% QoQ, with a net new ARR of $61.3M. Q1 revenue guidance is $137M, suggesting 10.2% QoQ and 77.6% YoY growth. FY2024 revenue guidance is $640M, suggesting 54.6% YoY growth, with ARR guidance of 47% YoY growth. Sentinel One’s cloud security solution more than doubled QoQ and contributed about 15% of quarterly ACV. About 30% of revenue is from EMEA.

Sentinel One’s Go-To-Market strategy is noted as the reason for still being cash flow negative, but the Q1 operating margin guide and FY2024 gross margin and operating margin guide show positive trends.

Sentinel One added 750 customers , reaching a total of 10,000, and added 78 $100k+ customers. The dollar-based net retention rate was 130+%, and the gross retention rate improved. The company added a record number of Global 2000 enterprises, and ARR per customer continued to increase. MSSP partners performed well.

Sentinel One expects customers to remain cost-conscious, but has seen increased win rates and was recognized as a leader in endpoint protection platforms. They plan to focus on product innovation in endpoint and cloud security, and expanding platform capabilities. They have a strong Glassdoor rating and employee retention and expects dilution to slow in FY2024.

After delivering strong 92.1% year-over-year revenue growth, the initial market reaction to earnings was muted. I assume analysts’ fiscal year 2024 revenue estimate of $651.26 million versus the company’s lower-than-anticipated fiscal guidance of $640 million was the reason. The stock price increased about 7% during the confident and uplifting earnings call, which felt slightly oversold.

Compared to SentinelOne’s 9.4% sequential growth , CrowdStrike’s 9.7% sequential growth at 4 times the revenue seems strong. To maintain conviction in SentinelOne, I want to see an acceleration in sequential growth soon, as their smaller size is an advantage. That said, the market is big enough for many players, so I avoid reading much into comparisons.

Viewed in isolation, I liked the results. The valuation suffers from a lack of profitability. I remain concerned about negative profitability and excluding the revenue from the acquired company Attivo, Organic slowed to 9%, S&M expenses increased, and absolute cash flow is not improving, indicating Sentinel One must work hard for customers.

Despite that, the trend toward profitability from a margin perspective remains on track, which is mission-critical for them, though absolute negative cash flow metrics must improve soon. $1.2 billion in cash provides enough runway.

I didn’t change my allocation and don’t plan to. Lack of positive profitability mutes conviction, though the relatively small market cap below $5B indicating an easy double in share price intrigues me to buy more, which I resist.

Key metrics I’ll watch closely and want to see improve in particular: $100,000+ customers, dollar-based net revenue retention , and cash flow .

Crowdstrike

What they do: Leading cybersecurity firm with a "mission to protect customers from breaches”

Confidence tier: Contender

Type of revenue: Seat-based (Endpoints)

Cash: $2.71B

TTM revenue: $2,241.27M

Market cap: $30.5B

My Take on the Latest Earnings

I liked:

- The upbeat and confident tone of the call. Several analysts congratulated them on their strong performance.

- Revenue was $637.4M, up 47.9% year over year, and 9.7% quarter over quarter , which exceeded my expectation of $634.48M and accelerated sequentially, so I’m pleased with that.

- The remaining performance obligations were $3,368.49M, up 20.4% quarter over quarter . Wow!

- Strong profitability and cash flows, especially the 42.9% operating cash flow margin while still investing in future growth.

- Healthy customer adds and customer retention metrics: Added 1,873 subscription customers , reaching 23,019, up 41% YoY, and 8.9% from last quarter. The Dollar-based Net Retention Rate was 125.3%, and customers using 5+ modules was 62%. Though, I’ll keep a close eye on customer adds since Crowdstrike now focuses more on the lower end of the market, meaning more small and midsize businesses with lower average contract values.

- Instead of a 10% quarter-over-quarter decline in quarterly annualized recurring revenue growth , they delivered an 11.9% quarter-over-quarter increase !

The problem is the guidance again, driven by budget scrutiny and longer sales cycles.

Last quarter my $1 million question was: Competition or macro? I believe we got the answer.

The new big question: When will this end?

Here is my thesis: Crowdstrike has a seat-based subscription model. I interpret the stabilization of sequential metrics as a slowdown in layoffs, which is good for seat-based subscription model businesses like Crowdstrike, indicating the endpoint market is not saturated and the market has stabilized.

However, this does not mean we should expect further quarter-over-quarter acceleration, as businesses are not currently hiring more. So, I assume we’ll see minimal beats for another 1 to 2 quarters and possibly acceleration again in Q3.

I believe assuming Q1 revenue of $690M, 8.3% quarter over quarter growth with a 1.7% beat is realistic and “prudent.” I try to make conservative assumptions (and if these sound too conservative, it’s time to trim) - the last thing I want is a negative surprise every quarter.

I also assume Crowdstrike will achieve around 40% revenue year over year at the end of FY2024 (with some luck), more would be very optimistic.

I added after-earnings.

Zscaler

What they do: Cybersecurity firm that provides services secure user-to-app, app-to-app, and machine-to-machine communications over any network and any location

Confidence tier: Contender

Type of revenue: Subscription-based

Cash: $1.91B

TTM revenue: $1,348.1M

Market cap: $15.6B

My Take on the Latest Earnings

Zscaler’s earnings results puzzle but the negative market reaction after-hours does not surprise me.

The situation: Zscaler delivered a good quarter. Strong revenue growth, great cash flow and profitability. While revenue came in at $387.60M, 51.7% YoY, 9% QoQ, exceeded expectations, calculated billings growth slowed, leading management to guide for weaker revenue growth in the future. Full-year revenue guidance was raised slightly, but calculated billings guidance remained largely unchanged. Remaining performance obligations growth has also slowed since Q1, raising concerns. Zscaler mentioned they helped some customers increase subscription commitments “a couple of percentage points”. I assume ~3-4% .

The company had a gross margin exceeding 80%, an operating income of $48.8M, a net income of $57.6M, and earnings per share of $0.37. Operating cash flow was $89.48M, and R&D expenses rose to $56.19M. S&M expenses increased to $180.55M, while G&A expenses were in line with prior trends.

Customer growth was so-so: 30 new $1M customers , okay. 120 new $100k customers, their lowest in 2 years . Still, this is the case for every company too—that’s fine. The Dollar-based Net Retention Rate remained at 125%.

Zscaler is seeing its largest sales pipeline ever, but sales cycles are taking longer due to extra scrutiny and approvals required. The company is on track for $5B annual recurring revenue and 60% of revenue comes from upselling existing customers. They face more competition at the lower end of the market but perform well at the high end, where their value is well understood.

Will revenue growth stay above 30% in FY2024? Am I okay with lower future growth if I expect steady, reasonable growth for years?

Undoubtedly, Zscaler remains an excellent business. However, I have difficulty envisioning their revenue growing significantly above 30% a year from now.

That being said, my evaluation may be biased by their underperformance in billings growth, which could be having an undue influence on me. I have never really observed a pattern in revenue growth following the performance of calculated billings.

The following article on calculated billings is an interesting read and mentions, "In short, calculated billings can only be a good indicator of future performance if all other factors (i.e. pre-billed subscription duration, the weight of professional services in total revenue, the timing of renewals, etc.) remain constant, which is rarely the case in the technology industry. "

I am considering giving less weight to calculated billings and instead focusing on other metrics. However, the other metrics (customer growth, RPO ) were not as strong as I had hoped, which is why my position will remain the smallest one.

Bill

What they do: Simplifies, digitizes, and automates complex back-office financial operations

Confidence tier: Bench

Type of revenue: Transaction- and Subscription-based

Cash: $2.7B

TTM revenue: $857.03M

Market cap: $8.1B

Recap and Conviction

Bill reported on the revenue and guidance for Q2 2023. The company’s total revenue was $260M, which is a 66.2% YoY increase and a 13.1% QoQ increase . Float revenue was $28.9M, an increase of 2588% YoY and 92.7% QoQ. Core revenue was $231.1M, an increase of 48.6% YoY and 7.7% QoQ. Subscription revenues remained consistent with the past 3 quarters, while transaction revenue experienced a slowdown due to macroeconomic conditions . Divvy revenue was strong. The company provided weak guidance for Q3; however, it is expected to be conservative until the macroeconomic situation improves.

Bill experienced strong non-GAAP profitability due to opportunistic float revenue and operational excellence. This increased gross margin and significant growth in operating income, net income, operating cash flow, free cash flow, and EPS. The company also has $2.7B in cash on hand, and it is expected to have even stronger profitability in the next quarter.

Bill added 10,700 customers , although the actual QoQ customer growth rate was 2.8% without the Financial Institution segment. Revenue per transaction increased by 3.5%, and Divvy added 1,900 customers , bringing the total to 24,700 Divvy customers. Divvy customers deliver the highest revenue per transaction , and total transactions for Divvy increased by 77.4% YoY and 10.6% QoQ.

Bill announced several updates, including the acquisition of Finmark, a $300M buyback program, and the launch of an SMB-focused solution with the new bank partner BMO. Financial institutions currently contribute 4-5% of revenue, but the company expects this to increase in the long term. The company also has a 12-month payback period, which is positive for a SaaS business.

While standalone Bill is still growing, its organic revenue growth has slowed down . However, Divvy, one of Bill’s businesses, is experiencing strong growth in terms of both the number of transactions and revenue. Divvy has the highest revenue per transaction at $9.21.

Although FI customers are growing the fastest, they do not contribute significantly to the revenue. Therefore, I will continue to focus on developing Divvy metrics, which is my main reason for holding Bill . Bill’s low subscription-based revenue makes it more volatile in terms of revenue growth and less predictable.

On March 10th, Silicon Valley Bank collapsed , which scared investors [timeline]. Some believed that this would be the second banking crisis since the pattern repeated in 2007. However, events like that rarely repeat twice, and I don’t believe it will happen this time. Just two days later, the U.S. government announced that it would backstop all SVB deposits.

Bill reacted very fast and professionally to the incident by announcing what they are doing about it. In short, of the $2.6 billion corporate cash held at multiple financial institutions, only $300 million was held at SVB, which will be recovered. Additionally, of $3.3 billion cash held in trust on behalf of Bill’s customers (FBO Funds), $370 million was held at SVB, which Bill believes a significant portion will be recoverable.

Furthermore, Bill announced that it would expand its commitment to SMBs Impacted by SVB Events , allowing customers who are also SVB customers to maintain business continuity, including a 3-month free trial to try the BILL platform.

Management’s reaction and initiatives following the SVB event increased my confidence in management and made me think that it was skill rather than luck that they weren’t affected by the SVB collapse. Well done!

As noted by Bert Hochfeld, I maintain confidence in Bill’s projected >50% YoY revenue growth [source]. I added several times after the SVB incident when the price dropped below $70 since I believe Bill, with a forward-EV/s of just 7 and a smaller market cap of $8b, is vastly undervalued at that point and provides a decent risk/reward.

Other companies

Read my recent reviews on Cloudflare, DataDog, Monday and The Trade Desk in my previous summary, as I didn’t have meaningful updates this time.

Closing thoughts

What a turbulent March!

- Nearly all companies issued low full-year guidance.

- DataDog had an outage for one day.

- Sadly, SVB went bankrupt—the market feared the next banking crisis.

- Rising interest rates—the market worried even more.

- Investors losing faith in software-as-a-service companies.

Let’s take a step back and categorize everything into two groups.

The noise bucket:

- DataDog outage for one day —Even the most successful tech companies like Microsoft experience outages sometimes.

- SVB went bankrupt —We likely won’t see another global financial crisis like in 2007. Times change and the world today is different. The next crisis will likely play out differently, not the same as before. Tweeting stock charts from 2007 alongside today’s charts won’t make the same outcome more likely.

- Higher interest rates —The market always worries when rates increase, as they have for over 100 years. But as long as the overall economy keeps improving, stock prices will rise over the long run. For investors thinking longer-term, over 3 years, don’t worry about short-term rate hikes.

The “what you can control” bucket:

- Lower full-year guidance from all companies —Prolonged sales cycles and budget scrutinies are causing companies to guide more conservatively than ever.

- Investors losing faith in software-as-a-service (SaaS) businesses —Understandably, it’s challenging in this environment to determine which companies will succeed in the end.

And I’m wondering:

- Am I too stubborn to stick with my boring tech companies?

- When is it time to change direction significantly?

- Do I fail to adapt quickly enough?

Believe me, I don’t want to end up following just one path, one industry, or one business model, realizing too late I should have changed. I want to be a successful investor in 30 years—looking back at returns that outperformed my benchmarks! So, maybe it’s time to rethink what kind of investor I am.

What I’m Not:

- Only investing in tech, SaaS, software, or any single sector - though I focus on them since they often represent the best businesses

- Only considering a single metric like growth - that’s not sustainable

- Practicing GARP (Growth At A Reasonable Price) - I’d miss the best businesses

- A trader - I believe long-term investing in successful companies will outperform any trading

In short, I don’t invest in just one industry or metric. I seek the best businesses for the long run , not just reasonable growth at a low price or short-term trading.

What I believe in:

Investing in the best high-quality businesses. What makes a business high-quality?

To me, it means having:

- Strong fundamentals : high-profit margins and metrics like growth, profitability, cash flow, and increasing customers.

- A predictable growth model : recurring revenue, for example.

- Great leadership : A visionary founder-CEO invested in the company’s success and a strong executive team.

- A positive company culture : Employees approve of the CEO and enjoy their work.

- Sustainable competitive advantages : Characteristics that help a company maintain an edge over competitors.

- Durable growth : Likely resulting from the above attributes. A large market, the ability to continually release new products, and layered periods of rapid growth produce consistent growth.

High and durable growth, coupled with strong quantitative and qualitative attributes, is my ultimate definition of quality.

Because enduring, durable, sustainable, [insert synonoum] growth - not growth at all costs - signifies more than rising revenue. It shows:

- There is demand .

- Customers eagerly desire the company’s products.

- The company is doing something right.

Investing in durable and sustainable growth is a bet on humanity solving problems, progressing, evolving, and improving the world.

The top digital companies —those offering products and services related to data and software and driving digital transformation —are still excelling in all of the above areas.

It’s not a dying industry like oil, tobacco, or newspapers. Cloud and Software are insulated from trade wars and overseas manufacturing issues. It reduces costs for enterprises, which is ideal for economic uncertainty . And despite weaker fundamentals from macroeconomic effects, data and software will continue to improve our world.

These are the high-quality companies I want to invest in.

And that’s what I am: An investor in sustainable growth, investing in our future.

But what about new opportunities and why are the best new businesses so hard to find?

I understand: Valuations and market caps differ from a few years ago and The Law of large numbers continues increasing while growth rates decrease.

Yes, company valuations were lower before 2019. They increased once the market seemed to finally “get it.” Then it overreacted.

Now - in my opinion - it’s overreacting again but in the opposite direction. Higher interest rates, inflation, and wars in Europe don’t help. But eventually, those issues will resolve , and the best, sustainable companies will remain. My job is to identify and invest in them. I see this as an opportunity, even without new, immediate exciting opportunities arising.

However, why aren’t exciting new companies launching?

It can’t be because digital transformation, data, software, and buzzwords are dead, right?

The reason the best new companies are staying private is that hot startups and unicorns don’t want to go public in this environment.

Consider this: As a CEO, would you want a 5x valuation now or triple your valuation in 1-2 years?

Though the outlook seems bleak now, VC firms have ample cash on hand, ready to invest. Once economic conditions improve, countless opportunities will emerge.

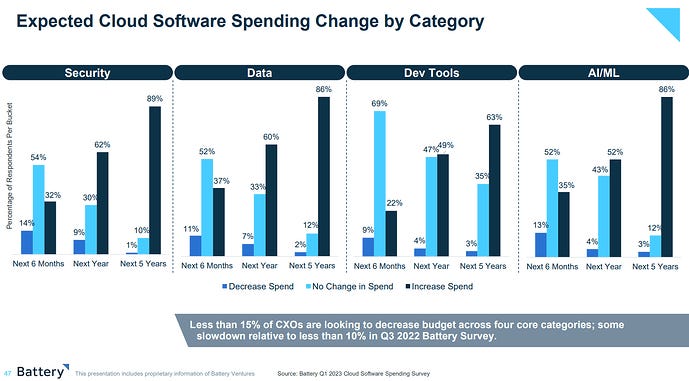

Remember: Cloud Software Spending is Not Immune, But It is Resilient:

46% of executives expect tech budgets to increase in 2023 , 60%+ next year, and 80%+ in 5 years , despite macro pressures (source).

I have to admit, this situation presents a genuine challenge.

On the one hand, I’m content waiting a few more quarters for improved performance while avoiding impatience and investing in high-quality, durable businesses with ample opportunities ahead.

On the other, I will continue evaluating my approach and try to remain flexible and open-minded to avoid getting stuck in the past.

I wish, I had that time-machine …

Appendix

My Watchlist

- MongoDB

- Duolingo

- Samsara

- Docebo

- Gitlab

- Okta

My Previous Portfolio Summaries

Thank you for reading.

Happy Investing, everyone!

PS - I am also publishing more thoughts on investing at my free blog https://www.happyinvesting.pro/