Oddity Tech, Ltd. ($ODD) came public on July 19, 2023 with a valuation of 2.7B. Unlike many IPOs they were already profitable.

Oddity Tech was co-founded in 2013 by brother-sister team Oran Holtzman and Shiran Holtzman Erel. Oran is the CEO and Shiran is the CPO. The company has operational headquarters in New York, R&D headquarters in Tel Aviv, and most recently acquired a proprietary lab in Boston.

While they produce beauty and wellness products, they consider themselves a tech company because of their tech-centric business model and R&D process. The headline on their IR page is “Transforming Beauty and Wellness Through Technology.”

BRANDS

Currently, their products include two brands with two more in the pipeline:

-

Il Makiage is a cosmetics brand that was a high-end, private company founded by a New York makeup artist in 1972. The brother and sister co-founders of Oddity bought it and re-launched it in 2018 with an eye to disrupting the beauty market with technology.

-

Spoiled Child was developed by Oddity and launched in February of 2022 to focus on skin care, hair care, and supplements.

-

Approaching launch in the next year is a third brand that will be more medically oriented, helping with acne, eczema, and perhaps other conditions. No name for it yet.

-

There’s a place-holder for a fourth brand, but no hints yet about that focus.

Launching all the time are additional products within each brand and the goal is that every brand reach at least $1B in revenue. The brands remain separate with their own leadership teams but share the technology stack, data, and vision of Oddity as the parent company.

Here’s a slide from their investor deck.

FINANCIALS

A couple of highlights from their March 5 earnings to interest the numbers people and then I’ll get into why they hooked me into a position, despite a couple of risk factors that usually make me more cautious.

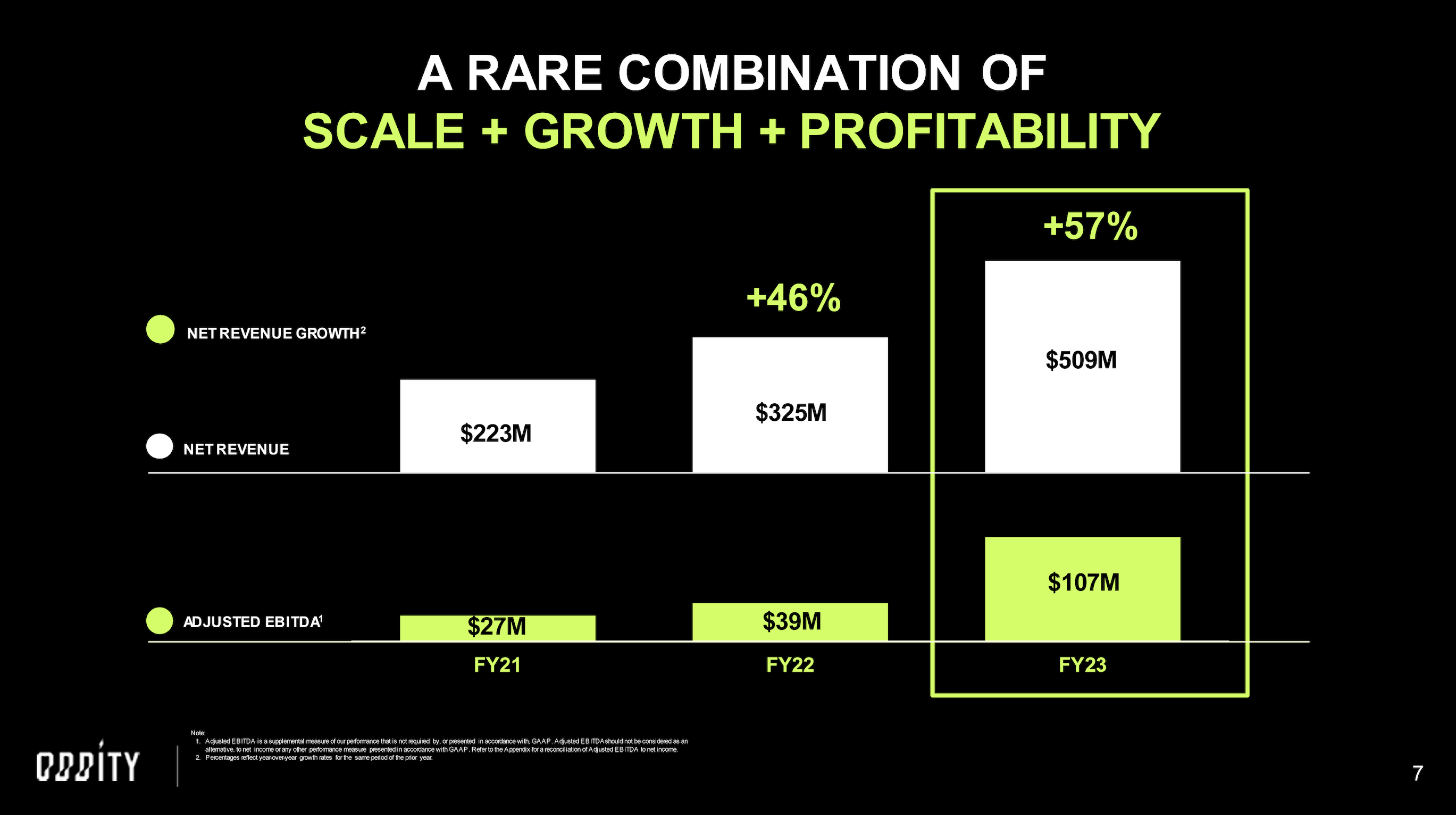

Highlights from their Q4 2023 earnings release:

- Record full year net revenue of $509 million, up 57% from a year ago

- Record net income of $59 million, up 169% from a year ago, and record adjusted net income of $77 million, up 181% from a year ago

- Record adjusted EBITDA of $107 million, up 172% from year ago

- Record $85 million of free cash flow generation

A couple of slides from their investor deck.

One of the things that makes the company an odd choice for me personally is that the C-Suite exec who tipped the scales for me is not the co-founder and CEO Oran Holtzman, but their CFO, Lindsay Drucker Mann, who they brought in from Goldman Sachs in 2021. While at Goldman, she was spearheading their research into consumer behavior among millennials.

Here she is at their IPO, explaining why she made the jump (about 8.5 minutes):

SPECIAL SAUCE

So what is all this tech they claim as their special sauce? This was a major hook for me.

They appear to have acquired their way into their various tech capabilities, so were they good acquisitions?

The first one was the e-commerce platform and Israeli start-up NeoWize. Oddity picked it up in 2019. It advertises itself as an AI company that personalizes e-commerce. A key part of Oddity’s strategy is to be a digital-first company that sells online, so it makes sense this was the first acquisition.

But is it a good company? Here’s what the Jerusalem Post had to say about NeoWize at the time of its acquisition by Oddity (actually acquired specifically for the Il Makiage brand at the time):

Founded by three veterans of elite IDF intelligence units, Ronen Ness, Omer Nevo and Yoav Cafri, NeoWize leverages data to make predictions on customer behavior even on the first visit, an approach which it claims can improve sales by 20-30 percent from the first day."

Current deep learning algorithms focus on making the most out of the data available. NeoWize utilizes active machine learning, neural networks and adaptive input to create more data and better data, thus increasing its predictive power even with limited available data," the company says.

That’s the smiling face of co-founder and CPO Shiran Holtzman Erel that you see with that article. Her LinkedIn profile says she has a degree in accounting and economics, but also that she served in the Israeli Air Force. My guess is that she was the one who found NeoWize, given its origins.

I think the same is likely true of their second acquisition, Voyage81, which Oddity (again through brand Il Makiage) picked up in August of 2021. That is the “computer vision” that the CFO keeps mentioning. It’s another Israeli start-up and Jewish Business News describes its capabilities this way:

Voyage81 is a deep-tech AI-based computational imaging startup and the only company in the world to develop patented software that brings hyperspectral imaging capabilities to smartphones via its physics-based algorithms.

Voyage81’s algorithms extract 31 channels of hyperspectral information from RGB images taken with existing smartphone cameras with 98% accuracy. Their tech can map and analyzes skin and hair features, detects facial blood flows, and create melanin and hemoglobin maps from a smartphone alone. So, this tech will obviously be of use to a make-up company like Il Makiage.

The CEO of Voyage81, Niv Price, is now the CTO of Oddity and, according to the above article, Price is the “former head of R&D at the IDF’s elite technological unit 81”

When you look at the capabilities of just that one acquisition and then start to think about how that level of imaging can give a uniquely personalized set of cosmetics, skin care, and medical grade recommendations, it’s jaw dropping. That is exactly the kind of tech that eliminates the need to visit a store for cosmetics. It doesn’t just make the experience easier, it makes it better in terms of product fit for each individual.

While not yet fully integrated into the selections of their brands, customers will be able to upload their face and get products that are exactly the right match for them. Hoping their cybersecurity is good!

The third acquisition, just made in June of 2023 brought in Revela Labs at Harvard. It’s a molecule discovery lab that is putting the science of bioengineering and AI techniques to work to find the best molecules for use in beauty and wellness.

Here’s about five minutes of Lindsay Drucker Mann talking about what the Revela acquisition last year brings to the company:

Revela’s CEO, Dr. Evan Zhao, was introduced on the earnings call as Oddity’s Chief Science Officer, but I don’t see him yet on Oddity’s website.

RISKS AND MOAT

Here’s the slide in their deck about their moat and TAM.

Of course there are the standard risks that they won’t be able to do what they say, that the tech is inferior to others, etc. In theory another company could do what they do, but, as the CFO noted in the first video I posted, these folks are driven. They will work themselves into the ground, which has so far produced lots of financial success very early–one of the reasons the CFO left Goldman to join them. It has also given them a strong first-mover advantage.

Co-founder and CPO Shiran Holtzman Erel seems to be the member of the family with the people skills. This is her description of what it took to get to their IPO. The mission she describes is to remake an industry, but I don’t yet know why this is the industry that inspires such dedication and therefore can’t gauge how easy it will be to convince others to give this much of themselves to it. Employee satisfaction and retention is, from what I see, a risk factor.

CEO Oran Holtzman appears to be an extreme introvert. I’ve found exactly one video of him and it’s in Hebrew. I was able to get the gist by taking the auto-generated Hebrew transcript and running it through Google translate, which is as garbled as you might imagine it would be. But he begins by explaining how he is giving this talk basically under duress because they had a successful IPO and he’s the CEO. He says he avoids such events at almost any price.

So the CEO won’t be the one out there stumping for the company. The CFO is an excellent spokesperson, but her regular job only gets bigger from here. Shiran’s LinkedIn post above sounds like she could potentially fill that role, but if she’s doing anything, I couldn’t find it. It’s a gap that needs filling.

The next section of Oran’s talk was his grief over the war, which is a reminder that the company has geopolitical risks. Those risks are mitigated somewhat by the Boston and New York locations, but they aren’t reduced to zero. They also sell physical products. While they aren’t in stores, they do have to ship around the world, and the war is disrupting Red Sea shipping. I haven’t figured out where their manufacturing is done, so if that part is outside Israel, that might be less of an issue.

I have only listened to the latest earnings call–from March 5. And the CEO there was a puzzle. He said things like this in his prepared remarks:

We basically grew way more than I wanted us to grow. In my view, there is no good reason to grow 50% at our scale, but due to both SpoiledChild’s ability to blitzscale and IL MAKIAGE’s stronger than expected repeat rate, we landed at a 57% growth rate in 2023 full year.

And about the Spoiled Child brand:

SpoiledChild scaled insanely fast in 2023. Since it was a one-year-old brand, I wanted to test the brand strength and its limits, and therefore, I allowed the hyper growth.

There were CFO comments and some questions about that, too, since the guidance was for a low to mid 20% growth rate each quarter after saying that they had enough visibility to know that they had already reached that for all of 2024.

So I’m confused there. I think what they’re saying is that their vision is so large that they want to reinvest everything above 20% back into the business to develop the new brands and drive into new verticals. Holtzman does strike me as a reclusive personality with enormous vision. But I need more clarity on that.

WHAT I DID

After watching them for a couple of weeks, I bought into a small position on March 12 at $45.07/share. About two hours later they announced a secondary offering (non-dilutive) that ended up pricing at $43.50. So I placed some limit orders and, like Holtzman, grew my position more than I had originally intended. It’s been above or below that since the offering closed on the 19th and I’m now sitting on just over an 8% position.

Ultimately I decided that it’s a huge industry, they have already proven themselves beyond what most companies have at this stage of their development. The potential in their acquisitions speak to a very broad vision that is just getting started. Their profitable and growing quickly. Their CFO gave me confidence, and each piece of tech seems primed to handle the scale of their vision.

At the very least, I think $ELF should be looking in the rearview mirror. I see an enormously competent C-Suite in their areas of expertise. My gut says that down the chain things could be harsh, morale low, and employee turnover high. What I would like to see are more senior hires that have strong skills in team building and demonstrated care for employees just to lay that concern to rest.

It’s an odd choice for me, but here I am.

JabbokRiver

8.13% $ODD