Oh what to do with PSTL and DEA.

Divi’s don’t meet my requirements. My only interest is Dollars and Cents.

Quill,

While you’re rejecting PSTL and DEA on the basis of your ‘Divvie Rules’, you should remind everyone just how silly and irrational those rules are.

Here’s what you require of a stock or ETF. If it pays a monthly div, then you require that it pays at least $0.11. If the div is quarterly, then you require a payment of at least $0.34. In sum, and as you say, you only care about dollars and cents, not dividend yield.

So, let’s run this thought experiment. Let’s say someone comes across a $15 stock that pays a monthly div of a dime, for a total of $1.20 per year. Simple, 4th grade arithmetic says that the dividend yield is a respectable 8%. However, you’d say that stock would be a bad choice, because it doesn’t meet your $0.11 cent rule, and you’d advise against buying it.

Here’s where things show just how silly you are. The CFO of the company knows you’re a savvy trader with a following of millions of subscribers. He wants his stock to be bought. But you’re panning it. So he convinces the board to do a reverse stock split of 4:1. Now the stock is priced at $60, and the board decides to raise the dividend to $0.12 per month. Now your rules say the stock could be bought for its dividend.

Quill, do the math. You wouldn’t buy the stock when it had an 8% div yld. But now that the div yld has dropped to a pitiful 2.4%, you find the stock attractive for the divvie portion of your portfolio? It that ain’t trading elephants for rabbits, I don’t know what is.

For sure, div yld can’t be spent at the grocery store or gas pump, only dollars and cents. But money put at risk in markets has to offer a decent return, and the only way to measure returns across instruments is ‘gains divided by cost’ (adjusted for ‘risk’).

PS I wouldn’t buy PSTL or DEA, either, because their fundamentals suck.

DEA earned paid about $ 0.09 cents per share per month on average for 4 months. PSTL about $0.06 per share per month for 4 months. They missed my one month.

The question was directed to the Grasshoppers as to what would they do assuming buying 1000 shares for each.

PSTL is a reality company owning building being rented to the US Postal Services. https://postalrealtytrust.com/

DEA not the drug company. https://easterlyreit.com/

They make boat load of money from the US Government Agencies Properties | Easterly Government Properties, Inc.

I am going to be Swing Trading these two companies for the next 10 years.

I like DEA and it is on my watchlist but I don’t think this is the time to buy into it right now. While it rents buildings to the government and I think they will be stable, that still won’t stop them from getting cheaper along with all the other office reits. Also look at this chart.

It looks like it is already to late. The RSI and the TSI along with the candles all confirm this should have been bought on 3/27. As far as PSTL goes I have no opinion.

Andy

2 Likes

“The question was directed to the Grasshoppers as to what would they do assuming buying 1000 shares for each.”

Quill,

I’m going to hold your feet to the fire over this one.

You use the term ‘grasshopper’ in a friendly, affectionate way to refer to ‘beginners’. But you really don’t understand the financial situation that characterizes them. DEA trades at $14; PSTK at $15. A 1,000 share position in either would be a $14,000 to $15,000 dollar bet. If the ‘grasshopper’ were following Wm O’Neil’s advice to divide cash into ten piles, --as he or she should be-- then they would need a (roughly) $15k grubstake, whereas the average American doesn’t even have $400 in savings with which to gamble in the equity markets. Opps. Just a slight mismatch between advice given and the means to act on it.

You can swing a big line and can make out-sized bets for two reasons. #1, Your assets under management (AUM) are in the millions. #2. You are very risk-tolerant. That isn’t the case with ‘grasshoppers’. They’ve got tiny money and tiny experience. Therefore, the max bet they should be making on DEA or PSTL --if at all-- would be a share or two or ten. And frankly, I think both of those stocks suck fundamentally, and I wouldn’t mess with them.

The second point I’m going to hold your feet to the fire over is your unwillingness to admit how bad and how unsound your divvie rules are. ‘Yield Percentage’ matters. But what matters even more is ‘yield percentage relative to risk’, which you totally ignore, as do most investors, because they lack a disciplined means to measure and to deal with it. (Which is a post for another time, but coming soon.)

Arindam

1 Like

Yields don’t pay the mortgage, put Food on the table, or Gas for the vehicles. It is the Dolla.

Your right, I don’t understand Yields and probably get confused at what Google is trying to say.

I went to " Chick-fill-A" today and said I want to pay in Yields, and they said sorry, NOT today, CASH or Credit CARD is acceptable.

Find me a stock that pays greater than $ 1.34 annually, I will buy it when the stock is heading north or at the Gate to replace any stock that is failing from any of my dividend paying portfolios.

194 Best Monthly Dividend Stocks for 2023 DNP has a yield of 7.24% yield and only pays $ 0.78 annually. OR about $ 0.07 per month.

I have two dividend accounts running

1 from M1 Finance via Ex Gen Dividend Investor all on autopilot with 25 stocks - How to Become a Millionaire / How to Become Rich - YouTube . What he bought, I bought.

The other from my Dividend block consisting of 12 portfolios (200 stock/etfs). In each portfolio is 15 monthly dividends paying monthly per my requirements. Currently I only own all of the first 3 and about 5 or 6 straggler stocks. O MAIN, GOOD and AGNC fills up my Gas tank every 4 weeks. Gas is $ 4.15 per gallon as of today. When I had my 2014 TESLA Model S 95, I would put the GAS money into buying more shares of stock on the first business day of each month for 4 years.

$0.11 monthly or greater.

$0.34 Quarterly or greater.

$1.34 Annually or greater.

I built the 12 monthly paying portfolios while in Sloan Kettering Cancer Center for having Colon Cancer back in 2013.

Have computer will travel, notebooks and 2 yellow legal pads. And access to the Fox Business channel.

While waiting around for the 4 drugs to take its time dripping inside the Power Port for 2 hours, I worked on the Dividend portfolio. The question was " How do I make money doing nothing".

Ding Ding - Let the money werk for you and not the inverse. This was going on for 3 months, every other week. I looked at the yields and annual payouts. Why was the lower yields paying a lot of money while the high yields were an embarrassment.

I have been Cancer free since 2013 and I see my nurse every year for an annual check up.

I taught and gave the portfolios to the 6 nurses and then taught them how use the Simon Sez III within Stockcharts. You take care of the Nurses and they take care of you.

4 Likes

Quill,

Kudos to you for surviving colon cancer. My Dad didn’t, and I miss him.

You don’t want to deal with calculating dividend yields, and you have my sympathy. The calcs quickly become tedious if the divs vary from payout period to payout period, as well as if multiple purchases of the instruments are made. But ‘yield’ provides a way to make rational, evidence-based choices and comparisons.

Again, let’s run a thought experiment. Three stocks are “at the gate”, and all are projected to offer exactly $1.34 in divs per year. One is trading at $5, the next at $50, and the third at $500. Which one should be bought? The obvious answer is NONE OF THEM. A 26.8% yield isn’t sustainable, and the stock is likely to go to zero. 2.68% isn’t worth fussing with, as isn’t a 0.268% yield. If the stock were priced in the $15 to $20 range, then it might be attractive for its 6.7% to 8.9% yield. But not at $25, and especially not at $30 or more, because they pay no more than what T-Bills are now offering, which is the other factor you ignore. “How much risk has to be accepted?”

Some background: Companies have two ways they can raise money. They can issue stock --aka, sell pieces of themselves-- or they can issue bonds --aka, borrow money. By and large, stocks aren’t assigned credit ratings, though they should be, nor even are all bonds. But between the credit rating of a bond and the coupon with which it comes to market, as well as any discount or prem that might be applied to the offer price, as well as how the bond trades in the secondary market once it has “seasoned” --from which can be derived a ‘market-implied’ rating–, it becomes possible for an investor to judge whether the gains that might be offered by the bond --from interest and possible cap gains-- are appropriate to the risks that have to be accepted.

Bond investors pay attention to ‘yield’, and to ‘risk-adjusted yield’ especially, because the bond game is primarily a yield game. Stock investors, by and large, focus on ‘cap gains’ and de-emphasize ‘yield’. But when yield becomes hard to find in debt instruments, such as when the Fed drops interest-rates to zero, then stock investors start trying to treat stocks as if they were bonds without understanding the game. That’s the point I’m making. You’ve got a divvie system that seems to work for you. But I can assure you that an audit of your transactions would show that you aren’t running it efficiently. For you, that doesn’t matter, because your assets under management are so outsized. But them with tiny money have to be efficient in their choices, or their account won’t grow as fast as they need it to.

Seriously, pull your records. On how many of your divvie holdings have you lost more in principal than you’ve gained in divs? Probably not many, right?, because you’re good about using Simon to jettison losers. But I’d bet that more than a few are scratches and that the money would be better off in T-Bills. And if I’m wrong about that, and if the cap gains are fat, then the div is irrelevant.

Arindam

1 Like

Now here’s an interesting dividend paying ETF:

2022 dividend total was 3.520838 and the last 12 month yield was 12.9% based on the price per Nasdaq right now…doc

1 Like

Arindam, this is very observant of you and so very true. When one is running six and 7 figure portfolios, 5 and ten thousand dollar losses are more tolerable than when one is running 1 thousand or 5 thousand portfolios…doc

Doc,

Quill is a person whom the Japanese would honor as a ‘National Treasure’ or whom his American counterparts would simply call “a helluva good trader”. Plus, he has an unbeatable work ethic and a constant drive to learn and explore.

But he’s been playing his Simon game --and others-- for so long that he’s lost touch with his roots and humble beginnings and them that have tiny money and tiny experience. Thus, whatever advice he offers has to be filtered by each person and their own means, needs, goals, interests, and opportunities. Also, he has some beliefs about what should and shouldn’t be done that just don’t hold up to close scrutiny. E.g., he hates mutual funds, avoids using options, etc. So, as always, borrow and be inspired by you can and just ignore the rest.

Arindam

1 Like

On the other hand, I want to take advantage of his knowledge (as well as yours ![]() ) and he has helped those two 9’th graders grow their small investments into nice ones for the future so there is hope for all. Success breeds success too…doc

) and he has helped those two 9’th graders grow their small investments into nice ones for the future so there is hope for all. Success breeds success too…doc

EWZ had a sell signal on 4/3/23

iShares MSCI Brazil ETF (EWZ) Dividend History | Seeking Alpha -

Ya missed, I don’t like to Short stocks. Nor I don’t like to be a Prop Trader.

https://tinyurl.com/3ept6372I Liar liar pants on fire. Most of these people have a luxury I don’t have during a 24 hour period and that is TIME.

These people are tighter than a crabs Alpha Seira Seira and that is water proof.

Yield Percentages ? Percentage of WHAT ! Everyone talks percentages of this and that and never Percentage of WHAT. !! I am confused. I keep asking OF WHAT ?

You guys can click on the chart once or twice for a larger view.

FXP is your better choice instead

of FXI. All of the International ETF’s are heading south for the last several days.

The International ETF’s are located on the Stockcharts right hand side at the 4th ICON going down.

CAT had a nice buy signal today. up $5.71 or 2.73 percent.

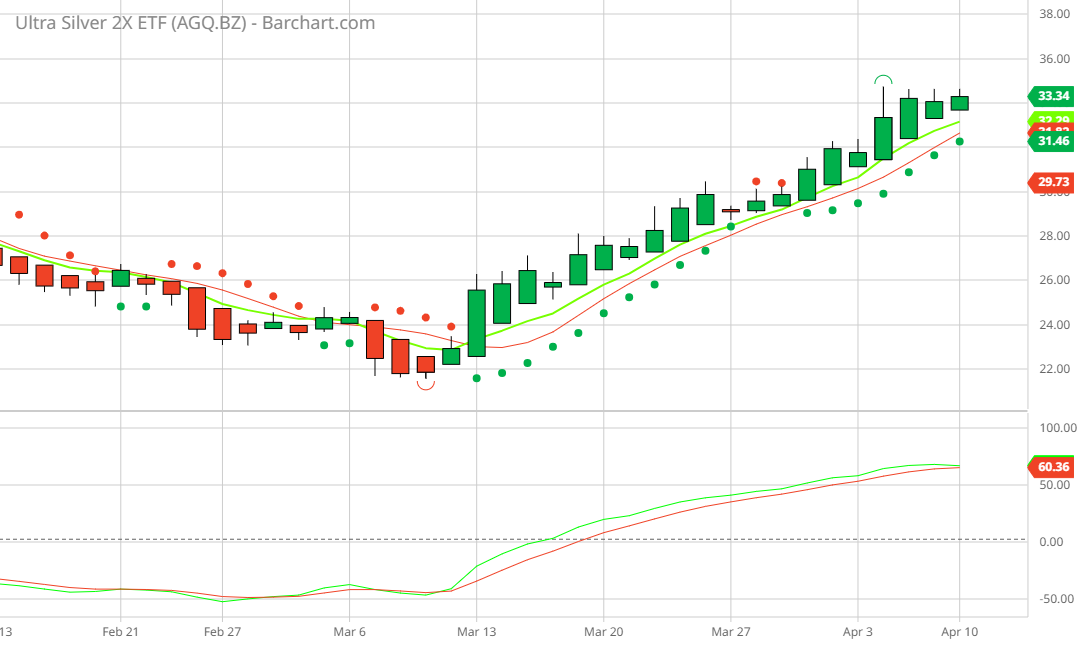

Okay, why was AGQ a nice head fake per the above chart, but lets look at the below if it works showing AGQ is heading south.

“Yield Percentages ? Percentage of WHAT ! Everyone talks percentages of this and that and never Percentage of WHAT. !! I am confused. I keep asking OF WHAT?”

Quill,

Stop pretending that you don’t understand the term ‘dividend yield’. You live in New York state, and you pay a sales tax that varies between 4% and 8% on many items you buy. Therefore, when you get up to the counter to pay, you don’t tell the clerk, “The price tag says $4.99, and that’s all I’m going to give you.” Instead, you round the price to $5, multiple it in your head by whatever the sales rate is in the city you live, and you hand over to the clerk --with a credit card or cash-- the upwardly adjusted price.

Same-same with divvie stocks. If the annual payout-rate is $1.34 and the stock price is $50 bucks, you know it has a lower yield than a stock with the same payout rate but a lower price.

You’re a superb trader, and you’re no dummie about basic, 4th grade math. Stop pretending otherwise.

Arindam

Quill

both of those charts you said were good are both way past the buy signal from back in March 13.

And all of a sudden you can’t figure out annual yield dividend!!! I see…doc

Ha! I learn something new every time I read this board, but this one takes the cake.

As far as grasshoppers go, we can just be new to technical trading methods, but not new to investing in general. We do all have to figure out what we can afford to lose on any given trade. I am starting out with small portions for now, but plan to increase as I gain confidence and solidify my method. It doesn’t bother me to see ‘1000 shares’ in an example. It’s all scalable. Hopefully, most people would see it that way.

1 Like

Doc,

What I said about beginners, their tiny accounts, their lack of investing knowledge and experience, and their intolerance of ‘risk’ wasn’t me being “observant”, just me remembering my roots and having empathy for today’s beginners.

‘Average net-worth per age’ is a topic that is frequently written about. The quoted numbers are nonsense, as it is easy to see from a thought experiment. If you and me are in a bar and we calculate the average net-worth of everyone present, the personal net-worth of anyone in the room isn’t likely to differ much from the calcuated average. But if Buffet, Soros, Musk, and Gates walk in, separately or together, and become a part of the game, then it quickly becomes obvious that none of the original group comes any where near to having a net-worth that is even close to the newly calculated average. Thus, the number that is meaningful is mean net-worth per age, and the numbers are frightfully tiny, (chart below) which why I all but go ballistic when someone blithely talks about putting on “1,000 share positions”.

But here comes the Catch-22. Unless a beginner takes on bigger risks than are statistically and probabilistically prudent AND is lucky enough to get away with it more than not, he/she isn’t going to grow their tiny, $14k account --assuming that their total net-worth is available for investing, which is never the case-- to $90k by the next decade of their life.

So here’s the next question. Given any market and account size, how much can be bet on each investment without risk of ruin? For sure, for them under 35 and their tiny investment account, it ain’t 1,000 shares of anything, not even penny stocks. There are huge debates in the gambling and trading literature about ‘optimal bet size’, which are well worth tracking down and studying. But we can cut to the chase and borrow from Wm O’Neil, who says, bet size should be no more than 10% of the account with an 8% stop loss.

That rule would exclude a beginner from buying even one whole share of a stock like TSLA. But fortunately, in these days of fractional share trading, there are workarounds that make the higher prices stocks available to small accounts. But the downside of fractional-share investing is that limit and stop orders can’t be used. So that 10% rule might need to be applied with some wiggle room. But it’s a good guideline.

Arindam

Dark Green is the ‘Mean’. Aqua is the ‘Average’. That chart predicts the US is facing massive old-age poverty, because they are reporting total net worth, not liquid net worth (aka, net-worth minus primary residence.)

Arindam,

I think I have been making the assumption that someone with a very small net worth would start out in mutual funds and advance to individual stocks later after having grown their account. But that’s probably a bad assumption. It’s nice that you consider all the possibilities.

You are right about the mean being much more telling than the average. Since the average does include all of the elite, it would be interesting to see this data from 3 years ago compared to today. Seems like the gap between the savings of a typical person and the savings of the elite got even bigger in the last 3 years. I’ve seen stats that individual credit card debt is at an all time high now too. Very concerning.

Just to clarify, in case, my comment about ‘taking the cake’ was in reference to Quill’s ‘waterproof’ comment above. Learn something new every day.

1 Like

Lisa,

The limiting factor to investing/trading success isn’t money, but knowledge, which includes ‘risk-management’, the chief part of which is proper ‘position-sizing’.

Van Tharp has participants play a trading simulation game. He pulls black or white marbles out of a bag 50 times. White is a winning trade; black, a losing one. Participants bet on whether he’s going to pull out a winner or a loser. Unbeknownst to them, 60% of the marbles are white. So if everyone simply bet the same amount on every trade, they’d be highly likely to come out a winner. But everyone doesn’t come out a winner, because they bet inconsistently.

Surprisingly, only a one-third of the people who play the game are winners. Of the two-thirds that lose money, half lose it all. This shows that the question, “How much capital do I risk on each trade?” is more important than the more fun questions, “What stock do I buy, and where do I enter?”

This is exactly the kind of market survival stuff that isn’t taught in stock investing classes.

Arindam

Arindam,

Yes, risk-management is important. The stop loss of 8% seems like a great rule of thumb. When I was previously all buy-n-hold, I didn’t use stop losses. With swing trading, it seems more necessary. I cannot find this comment now, but a while back I think it was you who mentioned to someone that if they put in some type of sell order at a lower price, someone else might purposely drive the price down to that level to pick up those shares. I do not remember the exact wording or situation, but it sounded like there is some nuance to stop losses that I am not familiar with. Does that sound familiar? I’m interested to understand the situation. If it doesn’t ring a bell, no worries.

Lisa,

What you’re referring to is called “running the stops”. Look it up, and make up your own mind whether it merits worry for a small, retail trader who’s often not trading round lots.

2 Likes