Link to full press release: https://investors.snowflake.com/news/news-details/2021/Snowf…

Snowflake Reports Financial Results for the Second Quarter of Fiscal 2022

08/25/2021

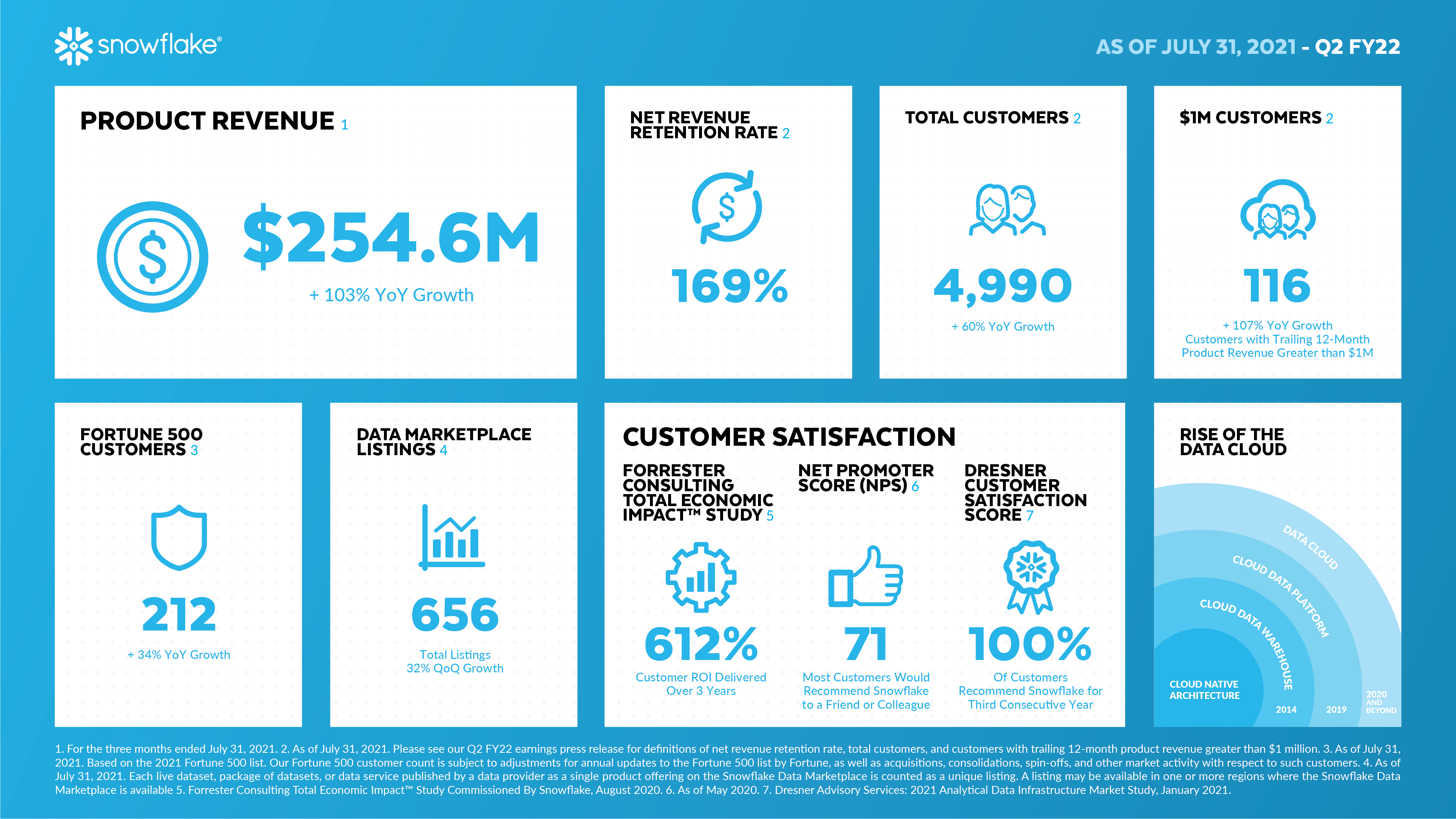

Product revenue of $254.6 million, representing 103% year-over-year growth

Remaining performance obligations of $1.5 billion, representing 122% year-over-year growth

4,990 total customers

Net revenue retention rate of 169%

116 customers with trailing 12-month product revenue greater than $1 million

No-Headquarters/BOZEMAN, Mont.–(BUSINESS WIRE)-- Snowflake (NYSE: SNOW), the Data Cloud company, today announced financial results for its second quarter of fiscal 2022, ended July 31, 2021.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20210825005718/en/

Snowflake FY22 Q2 Earnings Infographic (Graphic: Snowflake)

Snowflake FY22 Q2 Earnings Infographic (Graphic: Snowflake)

Revenue for the quarter was $272.2 million, representing 104% year-over-year growth. Product revenue for the quarter was $254.6 million, representing 103% year-over-year growth. Remaining performance obligations were $1.5 billion, representing 122% year-over-year growth. Net revenue retention rate was 169% as of July 31, 2021. The company now has 4,990 total customers and 116 customers with trailing 12-month product revenue greater than $1 million. See the section titled “Key Business Metrics” for definitions of product revenue, remaining performance obligations, net revenue retention rate, total customers, and customers with trailing 12-month product revenue greater than $1 million.

“Snowflake saw continued momentum in Q2 with triple-digit growth in product revenue, reflecting strength in customer consumption,” said Snowflake Chairman and CEO Frank Slootman. “While increasing net revenue retention rate to 169%, we also boosted gross margin and operating margin efficiency while our adjusted free cash flow was positive for the third quarter in a row.”

Lee

{kind=link}