| Year | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|

| Net Profit | 2,894 | 3,269 | 4,368 | 6,946 | 2,780 |

| Outstanding Shares | 518 | 504 | 501 | 471 | 460 |

Year end is Jan , i.e., 2019 is Jan-2019

I think bulk of merchandising issues (i.e., not having the products due to supply chain issues and consumer behavior changed due to COVID resulting in wrong inventory) are mostly behind. I am not saying consumer behavior is going to go back to pre-COVID level, but many retailers are slowly waking up to the change in behavior. The margin impact due to the above will also normalize.

Target has to find a solution for shop-lifting crime. This is a serious concern for shoppers to go into Target. At least for someone like me, I just avoid going to Target even though there are some items I would like to buy from there. This reduces traffic and money lost in theft (industry term shrink).

Of course the recession is perennially 6 months away, and that could hurt them in sales, margin, and store branded card losses. And could impact the earnings. How much, I don’t know. Currently, analysts’ Earning estimates for 2024, 2025 are $7.5, $9. The first 2 Qtr of 2024 are $2.06, $1.81, so the 2024 targets are more achievable. Now 2025 earnings assume margins get better. But conservatively we can assume $7 to $8 EPS. The dividend is $4.4 and yield is 3.97%

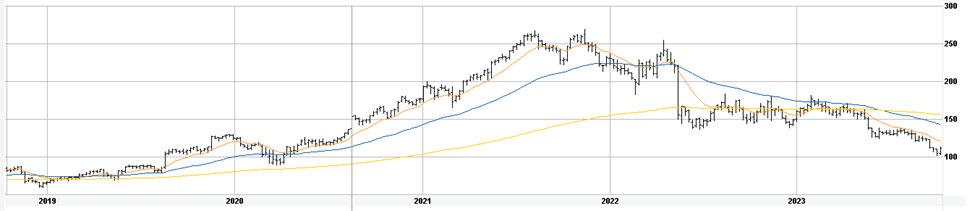

The stock is long way down from 2021 high of $260 to $111

For now, I am on the sidelines. I have sold Jan 2024 $110 put, Jan 2025 $100 put, $60 put. This lets me keep an eye on the stock, earn some premium, and if assigned will take the shares. OF course Jan $110 I will most likely roll it further out or further out and down or may even close if we get a strong year-end rally.

I have closed my Jan 2020 (pre-covid) position on May 2022, i.e., while I made over 40% gains, but completely missed taking profits at $260. There are many such stories… So the lesson is (right or wrong) take profits when your gut tells you.

In general, post year-end, after January, I want to go into Feb 2024 with only my long-term positions, deep in the money covered calls and deep in the money sold puts. Keeping significant dry powder.