Thanks to the great discussions in this board, I’m slowly dipping into buying growth stocks (currently own crwd and upst). I bought Upstart a few months back and added last week after earnings for a cost basis of $145.

There has been a lot of discussion on all the positives of Upstart, so I will focus on a couple of areas to watch for.

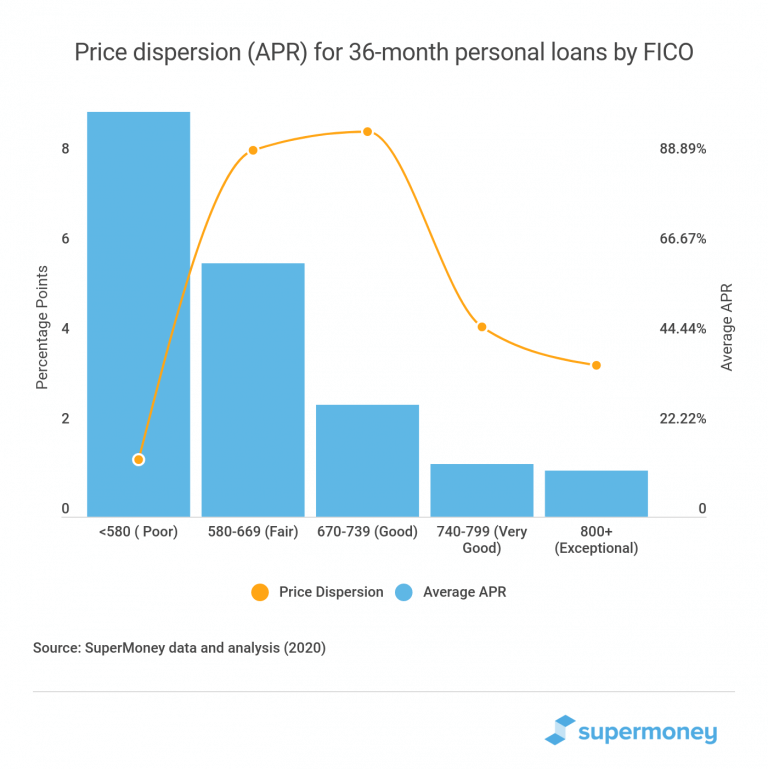

- Personal loan market share

As per an earlier post, the personal loan market is 84B per annum. Let’s say it’s $100B (there’ll be growth due to ease of lending from platforms like Upstart). In Q2, Upstart originated $2.8B, ~11% market share. It’s clearly very impressive and the main reason we’re all bullish.

With just a handful of bank and CU partners, I’m curious to understand how they were able to get such a big share. I would think there are 100s of lending entities, did Upstart manage to enroll a few big fish as early partners? Maybe someone with more knowledge of the industry could shed light into this.

Also, realistically they can only get to 20-30% of the personal loan market. Growing 20% sequentially will get them to this share in a year. For reference, they grew sequentially at 60% and 35% the last 2 quarters, so the market might consider even a 20% growth as a slowdown. Are these good assumptions or do I have some of my numbers wrong?

As I was researching this, another concern popped up. Apparently fintech’s account for 40% of the personal market and banks/CUs are ~50%. Fintechs likely won’t use Upstart and this makes getting 20-30% overall share even more challenging.

- Auto loan market opportunity

From CFO in the cc (answering the last question) - “But I think our expectation remains that the loans are clearly bigger and so there will be a higher dollar revenue per loan. And we’re expecting probably a similar dollar contribution profit per loan as we see in personal loans.”

We have been excited about the auto opportunity as the size is 5-6x personal loans. The above comment makes it clear Upstart’s fees would be lower. The CFO says they’re looking for same dollar revenue per loan which is concerning. If the average auto loan is 5-6x larger than personal loans, Upstart’s revenue from this market would be similar to personal loans.

The profile of the typical borrower is also very different. Personal loans are mainly for people with not so great credit, very high interest rates (20%!), rate spread between lenders is high and enables a platform like Upstart to bring efficiency, value and lower rates (win-win for everyone). Auto loans are dominated (in dollar terms) by people with better credit. Also, dealers have agreements with lenders for pre-approved rates - I have never needed to pay more than 2-3% so far. Upstart can still optimize rates for borrowers with bad credit and higher rates, but that market size is smaller.

Combining the above two makes me believe the overall auto opportunity (where they can actually win and their profit share of that business) would be smaller than personal loans.

Looking forward to thoughts from the experts who have looked at Upstart lot more closely.

-T2SP

{kind=link}

{kind=link}