Hey all, here are the details of my June 2025 portfolio review. I’ll put the allocations and researched companies in the text here, and link to the video at the end.

It was another strong month for results,

2024: +146%

2025: +35% YTD

Total cumulative return since January 2024, +232%

Allocations for this month look like,

Sezzle SEZL 17.6%

AppLovin APP 16.2%

Astera Labs ALAB 16.0%

Reddit RDDT 15.9%

Paymentus PAY 11.2%

Hims & Hers Health HIMS 11.1%

Cineverse CNVS 3.3%

Paysign PAYS 2.7%

Nova NVMI 2.4%

Dave DAVE 1.8%

Credo CRDO 0.9%

Champions Oncology CSBR 0.8%

Growth companies researched this month include,

TSS Inc TSSI - solutions for data centers

Leatt Corporation LEAT - makes protective gear for bikers

Innovative Solutions and Support ISSC - aviation, flight management solutions

Electrovaya ELVA - profitable lithium ion battery producer

Monolithic Power Systems MPWR - power management products

Climb Global Solutions CLMB - IT distributor connecting resellers

Kaspi KSPI - ecommerce platform in Kazakhstan

Pegasystems PEGA - AI decisioning and workflow platform

CyberArk CYBR - SaaS for identity management and security

NTG Clarity Networks NCI.TO - software for logistics

VitalHub VHI.TO - electronic health records with workforce automation

Kneat dot com KSI.TO - validation platform for life sciences

Zoomd Technologies ZOMD.V - performance marketing solutions

Hello Sir,

Like you, APP is one of my highest allocation positions given its demonstrated growth and traction /ROI with each new user base it has been incrementally adding to AXON..

My concern is that I’m hearing about how Gemini is leading to massive drops in click-thru-rates to content providers on Google. This is (at best) a tenuous connection to APP since AXON is more about in-app ads and CTV. However, I can’t shake the inevitable ad revenue collapse that will undoubtedly come from under-monetized SEO and content (one anecdote is business insider seeing 80% drop in search engine referrals.) seems like a potentially big weight on ad spend and thinking it could have knock-on effects.

Have you thought about this at all? APP is still a 10% position for me.

@EricPrzybylski My understanding of the AppLovin ad gaming product is that it wouldn’t interact with Google search results. Where companies like Google and Apple have some leverage over AppLovin is in the App or Play Stores. Since they create the rules for attribution and what is allowed, their policies changing can impact AppLovin. I’m not too concerned about this possibility though because back in 2022 Apple enacted new privacy changes which hurt mobile dev including companies like Meta. The whole industry took 6 months to adjust and it hurt Apple as well because they lost a lot of goodwill and revenue while mobile devs has to revamp their products.

I actually see AppLovin as the disrupter in this current situation. Meta Ads and Google AdSense/AdWords are about comparable on ROAS. However, AppLovin is claiming they have a significantly higher ROAS for their web pilot. This is why management keeps mentioning “performance” and how marketers will react when they see this higher ROAS which additionally gets incremental users that Meta and Google were unable to find.

With the way that AppLovin is cutting costs, they have a much more nimble organization than Google and Meta. I believe AppLovin has the capability to build an AdTech engine that is the size and scale that Google and Meta operate at. If they are able to do that and have sub 2,000 employees with nearly all the revenue going direct to EBITDA, there’s still tremendous upside to this company from my perspective.

I look at Applovin more on the same level as TTD. Here are some concerns that TTD had which everyone can google.

Google has impacted The Trade Desk (TTD) in several key ways, primarily through its dominant position in the digital advertising market and recent antitrust rulings and policy changes.

1. Antitrust Cases and Market Competition:

Google’s dominant position: The DOJ found that Google violated antitrust law by monopolizing open-web digital advertising markets, specifically through its control of publisher ad servers (DFP) and ad exchanges (AdX). This was achieved by tying DFP to AdX, effectively forcing publishers who wanted access to high-demand inventory to also use Google’s ad server, thereby limiting competition from other exchanges like TTD.

TTD’s struggle for fair competition: The Trade Desk CRO, Jed Dederick, testified in Google’s antitrust trial, outlining the difficulty TTD faced in competing in the display ad market due to Google’s control over SSP and ad server markets and its preferred ad network.

TTD’s opportunity in a fairer market: TTD’s CEO, Jeff Green, has expressed hope that Google’s behavior will change, leading to a fairer market where TTD can thrive. The antitrust ruling presents an opportunity to re-imagine programmatic advertising as a more open and transparent system, which could benefit TTD.

At present, I do not see much commonality between Applovin and The Trade Desk. TTD is primarily focused on CTV. At this time, APP does not play in this market, though clearly they purchased Wurl some time ago specifically to gain access to the wealth of data they can provide with respect to CTV.

As @wpr101 stated, APP’s appeal to advertisers is that they provide a higher ROAS than any other company is able to provide. In fact, if you go back to the 2Q24 CC transcript, Adam Foroughi said, “…our advertisers will spend much more today on our platform because we deliver profits to these advertisers. They’re arbitrage marketing on us, they are buying at a profit… let’s say that advertiser says, I’ll spend $1,000 today and I want to get it back in 30 days we get that within 1%, they get $990 - $1010.” That is not idle hype. It’s a guarantee. The only caveat is that they won’t accept an advertising spend that they can’t guarantee.

Will that same guarantee be provided going forward with web advertising and eventually CTV? I don’t know. Adam has spoken to that yet so far as I know.

In a nutshell, I don’t see Google or Meta or any other company posing a threat to Applovin. And, they are more shareholder friendly than any company I’ve ever held shares in. They buy their own stock aggressively. They strive at a minimum to purchase enough stock too fully offset a dilution that may result from SBC, but in fact they opportunistically buy more than that. And again, as @wpr101 mentioned, they are laser focused on cost control. They so not see the need to hire more and more folks. They do virtually no marketing, allowing the success of that AXON delivers to advertisers speak to the market. They are engaged in making their offering fully self serve so that they won’t need an army of engineers hand-holding customers.

People think that the only way to disrupt another company in through competition. But Google disrupted TTD not through competition but through their algorithms. Google also did this to Meta. Thinking they can’t do it to App is not the correct way to think about it.

Google has control over the Android ecosystem and the Google play store. They can set policy and rules on advertisement.

Google can set privacy regulations which can impact ads.

Googles admob platform sets policies for ads. If you get side ways to their policies they can shut a company down from placing ads on the android platform.

App relies on Apple and Google’s platforms, either one of them could put a bite in Apps business if they decide to modify or change their policies.

AppLovin is using about 20-30 standard techniques for attribution and tracking of users. There’s no way for Google or Apple to just shut them down out of nowhere without nuking their whole ecosystem. This is where the short reports are capitalizing on investor’s misunderstandings. They will say something like AppLovin is engaging in click hijacking the same way Cheetah Mobile was. However, if you look into the details of what a company like Cheetah Mobile had to get banned from Android, they were repeatedly and openly scamming on Android for years before any action was taken. Google warned Cheetah Mobile many times over a period of years before removing them.

Apple’s AppStore is much more restrictive than Google’s PlayStore. It’s why people call Apple’s ecosystem a “walled garden” whereas Android is sometimes described as the Wild West. Android needs to support a much wider array of devices and countries where Apple’s system is a lot more restrictive. Because of this Apple is the one most developers or companies are worried about. Again with Apple, they aren’t simply banning a company for violating rules. Their app submission to the App Store is rejected until they fix the issues. Apple isn’t deciding whether an app is ethical or they like the app, they are accepting or rejecting AppStore submissions based on compliance with their rules.

I am surprised that you would even argue this point because It is a given risk in everyone of their 10K’s. I am just highlighting the risk because of what happened to TTD and Meta.

**•changes to the policies or practices of companies or governmental agencies that determine access to third-party platforms, such as the Apple App Store and the Google Play Store, or to our Advertising solutions, Apps, website, or the internet generally;

•changes to the policies or practices of third-party platforms, such as the Apple App Store and the Google Play Store, including with respect to Apple’s Identifier for Advertisers (“IDFA”), which helps advertisers assess the effectiveness of their advertising efforts, and with respect to transparency regarding data processing;**

You can do a find on the document and search Google. It might be a good idea for everyone to search Google in this document and update your ideas of the risk. I am not saying App is a bad investment, I am just warning people to what they need to keep an eye out for.

The risks section of every 10K I’ve ever read, if taken to heart is sufficient to discourage anyone from ever investing in stock. This section is written by the legal department in order to insure that the company is shielded from litigation for every conceivable adversity that may conceivably impact the stock price, other than fraud or some other outright illegal activity.

I will admit that I am not familiar with exactly how Google damaged TTD and Meta. And even after having read your warning, I still don’t really understand exactly what Google did and how badly TTD and Meta were impacted.

There’s no investment that holds the potential for large returns that is also risk free. If you are very discouraged from investing in APP due to the risk posed by some action Google might take, I’d be curious to know what investment with similar potential that you think is a significantly safer bet.

You are going to have to take the information in the spirit it was given. Whether you want to accept it or not is totally up to you. While some risks in a 10K can be ignored there are others that have been proven to be very apt. Only someone who has been investing for a short time would think that there are investments without any risks. But only a fool would discount risks in their investments.

The language for risks in the 10-K forms is boilerplate for the risks section typically. Meta has similar language about the risks, and they actually call out that 2021/2022 time period where Apple negatively impacted everyone. Here’s from Meta’s latest 10-Q,

One more risk in Meta’s 10-Q,

Does it sound like a realistic scenario that Google would ever kick Facebook or Instagram off of Android?

This risk basically equates to Google decides to sabotage their entire mobile business.

Does it sound realistic that Google might do a major change to their search algorithm’s again? Everything doesn’t have to be an either or proposition. There are degrees of disruption. Like I said they did it and it changed the way TTD does their business. That is why TTD developed their Unified ID solution.

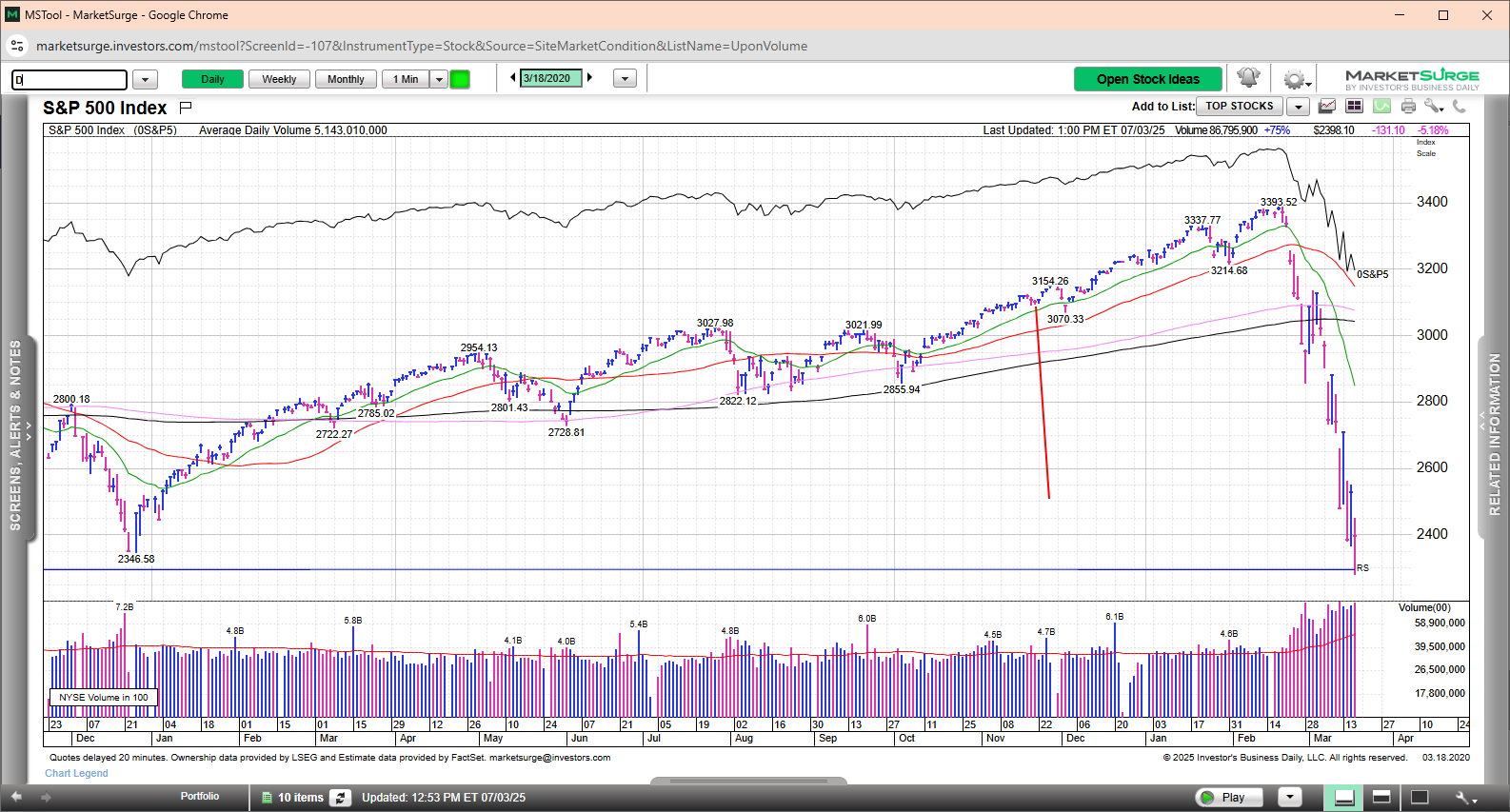

So where you see that red line is the date it came out. Meta just kept chugging along.

When Bert came out in 11/21/2019 it was a different story. But the drop didn’t happen until 2/19/2020. Remembering this drop it seemed to coincide with the drop of Bert but that doesn’t seem to be the case.

So it looks like I was conflating a drop in the overall market with the drop of Bert. Although, TTD, who I was following at the time, complained about it. It really didn’t seem to harm their business.

Here is TTD on 12/25/2020. Again the red line is 11/21/2019

I’m just getting up to speed with APP, so would like to hear from people more familiar with the business. But unless I missed it, I didn’t hear discussion of this particular risk even once in any of the analyst calls I listened to in the last year and a bit. So perhaps this isn’t as big an issue for them, given that they do in-app ads for mobile games mostly?

For me it sounds like they’ve conquered mobile gaming ads, which is a different market to non-gaming web/ctv advertising, and their next vector for growth will come from non-gaming ads. Perhaps Google/Apple are more relevant in this market? The success with that new growth vector is the thing to watch, right?

With that in mind, I have a question on KPIs: they mention MAP and ARPMAP as key metrics, and I can’t for the life of me calculate any revenue number that they report from that. So that is my first question: does anyone know what those metrics mean and to what revenue it ties back to and how? Those metrics have also flatlined for the last several quarters which makes me think that is a KPI only for the APP business:

MAP (m)

Q1

Q2

Q3

Q4

2023

1.7

1.8

1.8

2024

1.8

1.6

1.6

1.6

2025

1.5

ARPMAP ($)

Q1

Q2

Q3

Q4

2023

46

46

47

2024

48

52

52

52

2025

52

If yes, does that mean that those metrics are irrelevant going forward? And do we have anything except the P&L to gauge their success in the Ad business?

What I understood, reading it, MAP and ARPMAP are more useful for the management, not so for the shareholders and analysts. Maybe that’s why no one asks for those KPIs on the calls, as you pointed out.

While $APP provides such incredible growth, EBITDA and FCF margins, I assume MAP and ARPMAP will be ignored. In the future they could introduce new KPIs for the e-commerce, but we shall see.

Hi yes thanks that’s where I found the metrics (and in the prior quarterly releases).

To clarify, I have 2 points:

I pointed out that no-one seems to have discussed the potential risk of Google kicking them off Android in the ERs, which risk was extensively discussed upthread by @brittlerock , @wpr101 and @buynholdisdead. Hence that risk may be overblown. I was not referring to the KPIs.

About the KPI’s my point is that those metrics seem to relate to the App business, which has now been sold. If so, they are irrelevant going forward. Accordingly I was wondering if others see it similarly and whether there are other KPIs that someone has seen in their reporting or elsewhere which may be useful to track the ad business.

Probably the most useful metric to track in the ad business would be average ROAS (return on advertising spend), however, this is a metric that is unique to each business that places the advertising.

Foroughi (APP CEO) has alluded to it in the past, but it’s not a metric that they report, I’m not sure whether or not they would be able to as I don’t think they have a mechanism to gather the data in a direct manner. The best indirect way of determining it is in the revenue growth. If they are making their customers happy with their service, the customers will use more of the service and new businesses will come on board.

As for competition, IMO the business that is most similar would probably be META. Again, Foroughi has mentioned them in the past, but he does not see them as a direct competitor. His position is that no one will abandon META and divert their ad $ to APP. Rather, APP will function more as an add-on to META. Personally, I’m not sure I buy this. Businesses devote just so much budget to advertising. They will be prone to spend it wherever they find the best ROAS. If that is APP, most, if not all the budget will migrate to them.

@wsm007 The MAP (Monthly Active Payers) and ARPMAP (Average Revenue Per MAP) only applies to their legacy gaming business which they just sold in the quarter. This is why those metrics are flat as that part of the business was no longer growing, but these metrics will be irrelevant going forward.

AppLovin’s CEO has said that adj EBITDA per employee is the best metric to track the health of the business. The company has about 1500 employees right now, and I doubt there is any other tech company that has a metric this high for adj EBITDA/employee. Here’s what he said in Q4 2024,

I’d like to highlight our favorite metric going forward, adjusted EBITDA per employee. As we’re transitioning to a pure advertising platform, our focus will be on productivity, automation and building lean, high-impact teams. In Q4, we had approximately $3 million in run rate adjusted EBITDA per employee in our advertising business, and we expect that number to rise as we refine processes and scale our business. This metric underscores our commitment to operational excellence. Thank you for your continued support and partnership as we enter this next phase of growth. I’m more confident than ever that we’re building a platform with the potential to transform global marketing.

And then in Q1 2025, they said this about the metric,

Our run rate adjusted EBITDA per employee in our advertising business has risen to approximately $4 million annually, reflecting our commitment to operational excellence and robust economics.

Your analysis is correct that a lot of future growth will depend on the web expansion. I believe their top large competitors here are Google and Meta, and maybe to a lesser extent TikTok, Reddit, and LinkedIn among other social media or ad platforms. From what I’ve been able to gather management is saying they have the best Return on Ad Spend in the industry.

The timing of the launch of the web pilot going to general availability is still to be determined. They did say in Q1 that it may go live in Q2 but there has not been any press release regarding that. I’m willing to give them time to get the setup of this correct before launching. The gaming side of the business is still growing and able to carry strong results in the meantime.

I have reviewed many of your videos and they are very insightful, actually powerful.

My database includes quarterly metrics for the last four quarters, and I have not changed to Koyfin because they have indicated total revenue growth data for the last four quarters is not available from them. I note that you include quarterly data for the last 5 quarters in some of your videos. Do you have a source for this info or do you manually enter it using company data?