It is time to switch from SP500 to Berkshire. SPY, and QQQ have converged the mag 7 dominate the index weighting, if and when AI bubble bursts, both indexes will suffer. On the other hand, Berkshire with non-tech operating business, significant cash, will continue to muddle through, and on relative basis outperform the market.

At some opportune time, I will deploy my short SPY cash into Berky. There was an opportunity, and I missed it. Hopefully I get another opportunity.

I am not sure which period you were comparing. Currently Berkshire has very limited exposure to AI, outside of their Berkshire Hathaway Energy, which also has limited exposure to energy buildout for AI data centers, Berkshire reduced their Apple ownership also, thus, even their equity portfolio has limited exposure to tech/ AI.

Berkshire has big market cap, sufficiently liquid, and uncorrelated to tech/ai, I could think of. For someone like me, a relative outperformance on a downmarket is more important, because in a bull market I can outperform the market

IF only Berkshire pays dividend… who knows that could also be coming…

I have been thinking about it… here are some additional thoughts…

The Magnificent Seven stocks make up about 34–36% of the S&P 500 (SPY) and approximately 45–46% of the Nasdaq-100 (QQQ).

All Mag 7 companies have significant exposure to AI

If and when AI bubble pops, they all are going to suffer heavily, how heavy? Post COVID tech decline, stocks like $AMZN, $GOOGL declined 50%, and in the case of NVDA, I expect even more

Now, look at Berkshire a fortress balance sheet with $350 B+ cash and their insurance, operating companies have very little exposure AI

Berkshire cannot avoid the impacts of recession, but it will be very little

Shorting SPY and deploying that in Berkshire as a theory sounds good, there are practical challenges like margin impact, etc. But I have to come up with a better trade idea of how to implement this.

Already Berkshire is underperforming since WEB announced retirement. May be lot of WEB fans leaving the stock, but it is setting up the stock as a better hedge, if this trend continues…

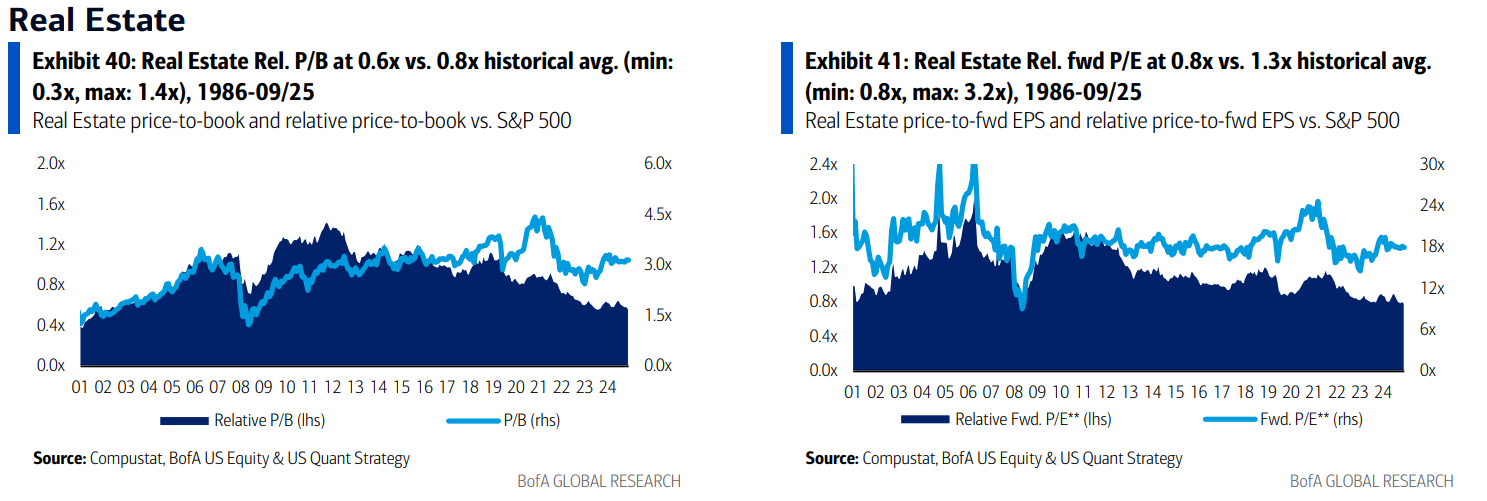

REIT’s may be another place to hide. The valuations are below historical levels, with lot of room to raise dividends, and in an rate cut environment, they may be relatively outperforming, heck they may even post some positive numbers…

Today, Berkshire received a rare sell rating from KWEB. While the analyst mentioned multiple reason, the primary reasons are:

Insurance weakness in P&C, Auto

With interest rates coming cash pile will earn less

The operating business, specifically railroads underperforming

Berkshire Hathaway stock is down nearly 1% Monday in the wake of receiving the equivalent of a sell recommendation from KBW analyst Meyer Shields, who cited several earnings headwinds for the conglomerate headed by Warren Buffett.

In a client note published early Monday, Shields cut his rating on Berkshire to Underperform from Market Perform and reduced his price target on the Berkshire stock continues to lag behind the overall market, continuing a trend since the Berkshire annual meeting in May when Buffett surprised shareholders by saying he would step down as CEO at year-end 2025 while remaining chairman.

I have flagged the insurance under performance in another post. While the reasons highlighted by the analyst are more or less aligned with my thought process, nevertheless I welcome this downgrade and any price decline. If berkshire could get to $400, I know I am greedy, that will basically setup the stock for next few years of outperformance. WIth or without Buffett, Insurance, railroad and most of the operating businesses will do okay. A significant price decline might provide an opportunity for Berkshire to do a significant buyback, of course, they may choose not to do anything.

I believe it was just the opposite. Geico margins are at 15% as opposed to the usual 5. No / or lower hurricanes hitting land means underwriting will also overperform, which usually leads to more competitive pricing the following year from others.

So it’s not that the insurance segments have underperformed, its that they are performing so well they have nowhere to go but down.

It is understood, the stock price doesn’t reflect the past but the future earnings… something generally Berkshire crowd with their rear-view mirror don’t get it

RICHMOND, Va., Oct. 29, 2025 /PRNewswire/ – Markel Group Inc. (NYSE:MKL) today reported its financial results for the third quarter of 2025. The Company also announced today it filed its Form 10-Q for the quarter ended September 30, 2025 with the Securities and Exchange Commission.

“I’m very pleased with our overall results and the progress we’ve made as a company this year,” said Tom Gayner, Chief Executive Officer. “Revenues and adjusted operating income of our businesses are both up for the year and for the quarter. We’re seeing improvement in our insurance combined ratio. And $2.1 billion in operating cash flow has helped fund continued steady share repurchases. In short, the strength of our diversified approach is on display, and we’re seeing tangible signs of improvement in areas we’ve been focused on.”

Summary of our third quarter results:

Operating revenues increased 7% for the quarter and 4% year to date.

Operating income, which is affected by market movements in our equity portfolio, decreased 26% for the quarter and 23% year to date.

Adjusted operating income, which excludes the impact of market movements in our equity portfolio, increased 24% for the quarter and 7% year to date.

For Markel Insurance, our cornerstone business:

Underwriting gross premium volume increased 11% for the quarter and 4% year to date.

Operating revenues increased 6% for the quarter and 3% year to date.

Adjusted operating income increased 55% for the quarter and 11% year to date due to increases in underwriting profitability and net investment income.

The combined ratio improved by more than four points in the quarter to 93%. For the year-to-date period, Markel Insurance’s combined ratio was consistent period-over-period at 95%.

Comprehensive income to shareholders was over $2 billion year to date.

Operating cash flows were $2.1 billion year to date.

Share repurchases were $344 million year to date, and we had 12.6 million shares outstanding at September 30, 2025.

First, I have decided to ignore your post. But thought I will share this.

Why I write? Because it helps me to think clearly, at times deeply, keep me sharp, and share my views. Merely pasting the press release shows a certain laziness, instead of saying here are the thinks that I think are important, the 3 thinks why you should consider… etc.

Of course it is your choice, just like I have a choice as a reader.