My musings last month turned prescient for my portfolio as the music did finally stop in October, with my first month in the red since March, albeit less than 1% down. My only stocks that performed well were in AI, and all other sectors were down, especially smaller caps. Almost all of this was macro related with the trade war. Since many of my companies don’t publish a ton of news in between earnings, my portfolio seems to be pretty susceptible to macro factors - interesting given the recent chatter about “hype stocks” on the board.

I don’t think we search out hype stocks, as much as we look for strong numbers with tailwinds that suggest the numbers will continue, which also tends to produce “hype”, which is ultimately very beneficial. I have a mix of companies that are in all stages of “hype” - pre, during, even post (but hopefully also pre). Many of the pre-hype companies can see big increases during earnings, but then not see much activity for another 3 months. I figured that’s something you have to accept if you want to get on anything early, especially small or micro caps, but it also seems to be industry dependent.

That being said, people have made a ton of money this year on companies whose hype is perhaps outperforming their results, in my humble opinion. No hate, there is something to it, but it seems that when the hype ends, they tend to fall hard fast, and it’s hard to predict when that will be. There are many on this board who are more knowledgeable than me that can identify when they hype will likely play out in results, but I tend to wait, which has repercussions.

For instance, with the battery stocks the board has been discussing, I don’t see numbers that justify selling any of my current positions until I see the next earnings reports. But I understand why the sector has a ton of attention. I will likely take a position in ELVA and/or EOSE soon during this earnings season, and I’m comfortable being late to the game.

I will likely do deeper company reviews in 2 weeks after earnings, but I’ll drop some thoughts below, especially since I added some new positions this month, and made some adds & trims.

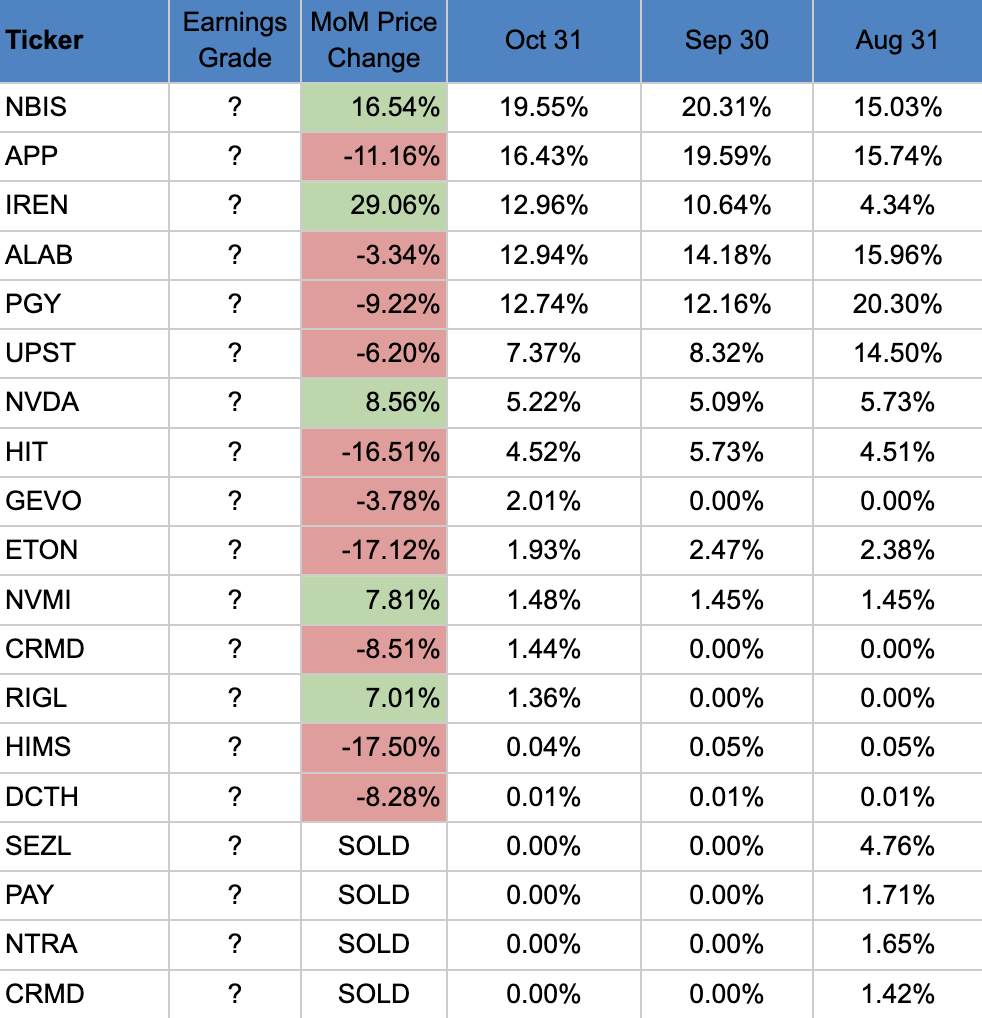

Here are my results to date and current portfolio:

JAN: -2.42%

FEB: -1.15%

MAR: -20.60%

APR: +7.91%

MAY: +24.92

JUN: +11.48%

JUL: +17.66%

AUG**:** +12.85%

SEP: +19.52%

OCT: -0.32%

YTD: +67.77%

NEW COMPANIES

I adjusted my screener to account more for profitability, which led to 2 new companies, GEVO and RIGL. And I got back into CRMD after reading @drew1618t‘s analysis. The funds came from trimming down NBIS after they once again hit over 20% of my portfolio during the month.

GEVO

It looks like @wpr101 had this on his watchlist, and I also stumbled upon it after messing with my screener. They are a sustainable energy company, and I’m still learning about it. But they make money by producing low-carbon fuels but also through selling carbon credits as they capture carbon from their North Dakota plant. They are coming out with new revenue streams relatively regularly, in fact one just dropped this morning. This new carbon credits contract is only $5M/year initially, but at such a small run rate, if they are able to consistently add these kinds of contracts, it will add up to massive growth. Since adding carbon abatement to their strategy in July 2025, they have signed two deals in September and November. So I’m watching this closely.

This has led their revenue to take off, moving from 5.7M → 29M → 43M. Current YoY Quarterly Revenue growth is over 700%. They also just had their first profitable quarter, with gross margin at 57% last quarter. It seems to be priced well below analyst price targets and is certainly under the radar for now. They report on Nov. 10th.

RIGL

Rigel Pharmaceuticals is another Biotech company which I really haven’t had a lot of luck in, but the numbers stood out so I took a starter position. They provide therapies that enhance the lives of patients with hematological disorders and cancers.

RIGL had a big one time revenue contribution from collaborative effort with Eli Lilly, which caused revenue to nearly double QoQ last quarter, but under the curtain, product sales also increased 76% YoY. They are GAAP profitable with gross margin around 80%.

They have 3 products, Tavalisse, Reslidhia and Gavreto. The latter two products have been introduced in the last couple of years, and all 3 products continue to grow. They are also expanding internationally, with the latest market being South Korea. They sounded very optimistic on their Q2 call, we shall see how it shakes out in Q3.

CRMD

I dropped them due to flat revenue QoQ which seemed like a flag for such a small company. But their preliminary release showed a huge increase in sales and @drew1618t’s analysis spelled out the market opportunity and momentum very well, so I got back in.

OTHER COMPANY-SPECIFIC THOUGHTS

PGY/UPST

The credit fears hit a high with the fallout from the First Brands and sub-prime lender Tricolor’s bankruptcies. I don’t necessarily see a connection to either Pagaya nor Upstart, but both have been sold off (especially Pagaya) continuously since mid-September when the credit concerns began. The actual financial results for both companies this year have painted a very different picture, so it will be interesting to see what happens if they beat and raise again. Upstart has been severely punished for again taking loans onto their books, but they have stated it’s temporary. We shall see what they say during their report tomorrow.

DCTH

They had a really disappointing preliminary report, missing earnings and lowering their guide. I am keeping them in the portfolio only to pay attention as I also had purchased some long calls in DCTH. They are still confident in their long-term growth trajectory, so I’m curious what they will say about this disappointing quarter.

WRAPPING UP

I’m excited for earnings and am going in very confident about my top 6-7 holdings. If all shakes out well, this should be my best year since 2020. Best luck to everyone, and more importantly, to our holdings!