Orange is my projection on Q4 sales and script numbers, otherwise actual trends.

2 Likes

So the past 4 Q’s, their drugs have sold approx $285m worldwide.

There are no sales yet for Japan (starts in 2025) and new markets like Canada/Israel just announced, and I am ignoring the currently immaterial Daiichi-partnered markets in South Asia and South America as they aren’t meaningful yet.

You would think this is a no-revenue start up or something the way it is trading.

I think a lot of the angst in stock price reflects poor decision-making by mgmt, and perhaps some bad luck, starting in 2020.

Summarizing here, and obviously I wasn’t in the stock at the time (first bought Dec 2023) but prev CEO and company got FDA approval for Nexletol/Nexlizet. This isn’t the same as the “broad label” they have today. Basically they were restricted to things like “if you have a patient that is either statin-intolerant or needs more help than a statin provides, then you can get Prior Auth from a cardiologist and have Bempedoic Acid added to the mix”. It was a restricted label in the “secondary” market.

Stock price was as high as $60-70 back then but also 1/10th or so the outstanding shares.

Esperion “launches” their product right into the face of a covid shutdown in 2020. They don’t do so hot. (shocker)

Meanwhile, they hire current CEO as the COO and commit to the Phase 3/CLEAR trial that would allow for a less-restrictive label. This takes years. CEO gets fired, COO takes over, dilutes the heck out of the company to stay afloat as their revenues were small at time.

They start partnering in Europe and elsewhere, getting milestone payments that helped the bottom-line year to year, while treading water in US sales.

Ironically I showed up about a month too late to catch the bottom in late 2023, but from a fundamentals standpoint, it was actually the time to start paying attention, because the CLEAR study was finally wrapping up, and it would lead to the FDA updates and expanded label in March 2024 that included Primary prevention and no requirement for Prior Auth.

At this point, the insurance machine moves a bit slowly, and we saw waves of payer improvements (covering at better prices, removing Prior Auth, etc) in June, then Sept, and final insurance updates should kick in on January 2025 (such as ExpressScripts, DoD contract, etc)

Also this year they got rid of horrible “RIPA” debt by temporarily handing off their DSE royalties in Europe until OMERS collects $500m (guesstimating some time in 2027/2028) at which point the royalties revert back to Esperion, likely worth 20-25% of what should already be a $1b+ runrate based on current trends. So that alone could be worth $200-250m/annually starting in 2028.

They had Notes coming due in Nov 2025 and they just refinanced that out to 2030 today.

They continue to actually make progress on new markets as they mentioned in ER’s this year as a goal, and the other (perhaps more exciting) goal is to announce new “indications” for Bempedoic Acid for help with Liver, Kidney, and perhaps Cancer in 1H-25. That “potential” should pop the stock plus add more patent life. In addition, their DSE partner is pursuing the triple-combo of BA+statin+ezetimibe which should also extend patent. Esperion isn’t pursuing triple-combo in US, presumably due to costs of study, and fact they probably either want to come to a partnership deal in US or in case of a buyout the new parent company would fund any needed studies.

Anyway - I still believe I showed up to ESPR at right time. If I was a good technical trader, I might have played all these moves from $2 to $3 more astutely, but at my age/experience, I am resigned to the fact that my forte isn’t trading, or macro timing (ha), but rather finding what I think is undervalued at X and selling it for Y. I don’t have a hard or fast rule for how long I will wait, but at some point opportunity cost kicks in via missed opptys in other stocks…so I kind of want 2025 to pay off or this thing may get relegated to the dustbin with other Dreamer unfulfilled greats like Elastic (ESTC).

I am hoping it is more of a TTD type result, of course. ![]()

Do your own DD, and good luck out there!

time to buy more xmas presents,

Dreamer

5 Likes

WOW this stock trades crazier than Upstart. After today Upstart became my largest holding. I did buy a little more ESPR on the dip. 4 of the 5 largest single trades on ESPR this month were in the last hour of trading today. 3 x 750K shares @ 2.13 & 2.15, 1 Dark pool transaction at the close 740K @ 2.25. Someone is buying the dip!

5 Likes

quick update.

Side note first: where the heck do people talk stocks online now? Stocktwits is akin to ragingbull from back in the day…mostly trash. SeekingAlpha has decent amount of articles but not really a separate mssg board (that I am aware of anyway). I did a google search for “top stock discussion websites and apps” or something like that, and TMF was literally the top response. Yet this place a ghost town.

Discord maybe? Some folks on Reddit? Twitter/X has some, but soooo many bot messages to filter thru, mostly saying “check me out on discord!”.

Anyway, what is new with Esperion?

They had a conf call at JPM health conf earlier this week.

Not a ton new, except a date given (April) for an Investor Day and the new indication/molecule or whatever they refer to it as will be targeting liver disease, with a supposed $2b market. Nice to see progress on the new pipeline front.

Here is my latest running list of “what has happened” in past 13-14 months or so.

They have an updated investor preso on the Events link of their IR dropdown.

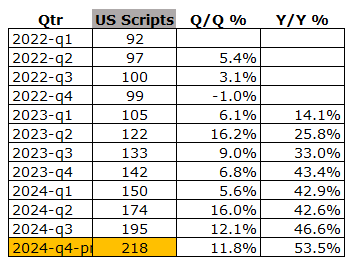

Notable was showing “12%” as the Q/Q growth in US Scripts for Q4. So I still have it listed as “proj” but here is latest Script trend then:

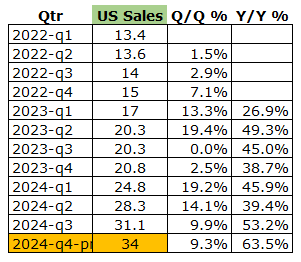

Sales is lumpier than Scripts, just generally follows it. The idea is that Sales is comprised of payments received from big 3 pharma wholesalers, and there may be some seasonality tied to medicare or when purchases are made, etc…

My best current guess is that US Sales will come in at either $33-34m.

Here is where it left off.

I had to make a point on stocktwits about the Q3-23 and Q4-23 SALES anomalies in the data. Was told elsewhere offhand that Esperion may have had higher rebates to the wholesalers during this period, which is why Sales were flat 3 straight Q’s yet Scripts is always steadily up every Q. So I did a quick exercise to show what Sales would look like if it had followed the SCRIPT Q/Q % growth for past couple years.

What does this tell me? It tells me at least that true sales/script growth is now just ticking above 50% y/y and that the past two Q’s, which were also the first two Q’s after the label expansion after completion of their years-long CLEAR study, has shown a slight inflection up.

I think there is a good chance this inflection continues in Q1, which seasonally appears to be a strong Q. I guess this might have something to do with updated insurance/payer UM criteria, which in turn impacts how much of a drug the wholesalers buy to start the year off. Anecdotally it appears payer coverage improved in a few waves; June, Sept, and now Jan.

We have Q4 ER coming up sometime in Feb, and usually a week prior we see the results from their European partner DSE, too. I don’t expect many/any surprises at that ER. But if they are off to a fast start in January, it would be good to hear that, and there was word of an expansion in the DoD contract that opened up another 8m potential lives to prescribe to. I would like to hear more about the indications, more about the DoD impact, any news/movement on partnering for the Canadian market, and perhaps Australia.

As always, the really big news, and end game, is either a massively important US partnership with a big pharma or a buyout. But if those don’t occur, then pretty much just killing time until May ER for Q1. Honestly, I have that mentally penciled in as very key. It will have been 1 year in April that the new label expansion occurred. Sales and Script growth should maintain or increase growth with that organic momentum and tailwinds of improved coverage. If not, then may be time to say thanks for all the fish. But to borrow a page from Saul, if growth keeps occurring, especially at 50% y/y levels…I think eventually the market buys in and the stock price takes off. That is the hope anyway.

Keep in mind, as always, I am just a guy on the internet. Do your own DD.

Enjoy the long holiday weekend all!

Dreamer

9 Likes

Some event on the 22nd, nice slide deck that I don’t really understand

https://www.esperion.com/static-files/5fcd31e6-b0bd-4729-941a-f5c7e93ca592

4 Likes

well…if you like low-priced moonshots, might be time to buy now.

By my count, there were (5) times that the price went from around $2 to around $3 since approx Dec 2023.

There are always concerns about dilution due to their past, but since Jan 2024, there has seemingly been only good news.

Hard to advocate for a stock performing so badly, but, ironically, that is also the best time to enter IF the fundamentals will eventually be reflected in the stock price once again.

They finished their important/expensive CLEAR studies which led to the label expansion in Spring 2024, which led to better insurance payer coverage, and scripts have been increasing every Qtr since, peaking now (based on their 12% Q4 script growth disclosure at JPM conf earlier this month) at over 50% y/y script growth.

We normally get excited on TMF about “50% growth” whether it is tech, SaaS, etc… Sales are similar, as you would expect, but some nuances as their sales are largely via big three wholesalers who in turn are purchasing based on script trends. So, for me, scripts = sales even if it is +/- a few percentage points in any given Qtr.

They entered 2024 with a lot of debt and addressed it all via monetizing their royalty stream of their EU partner DSE and then a recent refinance of their Nov 2025 Notes. That does appear to have led to potentially (a bit unclear) of 15% dilution.

At this point, they have a healthy amount of cash.

They have a proven product that sells over $100m/year, and which did approx $120m in 2024 in US sales alone.

They stated at JPM conf this month that they expect $130m in milestones from their Japanese partner Otsuka.

If they maintain a 50% growth rate in 2025, they would do approx $180m in US sales. Add in the $130m in milestones and that is a min of $310m they should bring in, against approx $240m in expenses for 2025 per same JPM conf.

So they are well under $1b mkt cap, they will be profitable in 2025, and they are currently growing over 50% y/y.

So, yeah…I don’t get the stock price troubles. I expect Q1 will be good, as it seems a bit seasonally strong in prev years. That ER would be May.

They also have their investor day for new liver indications (aka new potential future revenue stream) in April.

To sum up:

DSE reports late tonight, so should see how their European sales trends are holding up by tomorrow.

Esperion reports probably before Feb 15th.

Investor Day in April.

Q1 ER probably before May 15th.

Kind of feels like, if they don’t get a buyout by their Q1 ER, that you think there is a good chance for a 6th runup from $2 to $3.

But I am just a guy on the internet…so do your own DD.

Dreamer

4 Likes

I’ve been following along here and ST… the disconnect between fundamentals and stock price is curious. Usually, in software, hardware this provides a unique opportunity to get in cheap. Being this is a Pharma/biotech stock I just can’t help but think I am missing something. I have a 4% position at avg of $2.11… but I’m hesitant to go any deeper. good information on the company! thanks

2 Likes

Added 10% more today at 1.87 for first time since mid-December when I added at 1.92. Avg cost is 2.01. 1.93 avg cost if i factor in profits from trades (which I do).

I have a bigger limit order sitting at 1.54 because that old gap wants to close. It really wants to close.

2 Likes

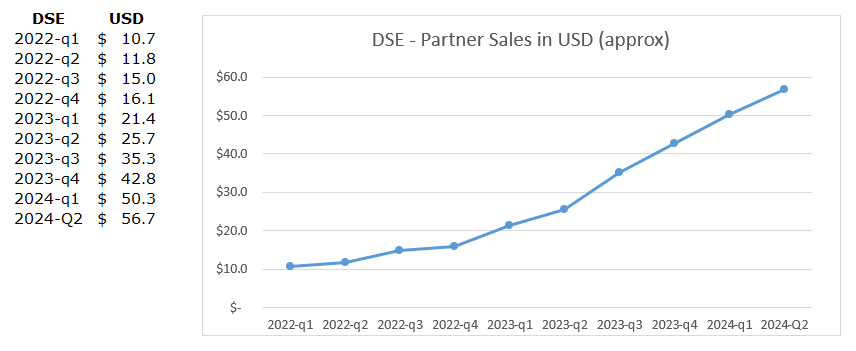

Here is the info I posted on X about the good Qtr DSE just had, and for the heck of it I wanted to model how long it might take for royalties to revert back to Esperion, and this napkin math says maybe mid-2028.

DSE is growing about 70% y/y. They just did about $63m USD in their most recent fiscal Qtr, which is Q3 2024 for them. So they are already a $250m/yr runrate business.

The drugs are legit. No idea if my projected math is legit, as I am just a guy on the internet.

2 Likes

I looked at the DSE results but hard to decipher. Are you looking at just the Nilemdo/Nustendi (BA) revenue for your calculations? Looks like it was up 119.4% YoY.

1 Like

DSE lists results in japanese currency and then also EUROs. A lot of the info is YTD vs just qtrly. There is one page that lists the qtrly breakdown. You will see $61 listed, which i translated to $63m in USD.

I keep converting to USD and over time that may lead to slight percentage differences due to changes in the conversion at that moment in time.

But you can see my numbers above.

Dreamer

2 Likes

Orange is based on DSE forecast.

Yellow is just me showing what future might look like. Green is showing potentially when the royalties could revert back to Esperion.

1 Like

Maybe the question should be whether anyone invests in individual stocks anymore . I am probably of a demographic not representative of stock pickers. But I currently have only one position that would be worthy of the effort needed to post about it. That is ESPR and I have nothing to add to what is already presented here. You are convincing enough that I have a 4.7% holding which is further supported by a couple of bullish analysts who serve up koolaide targets of 4x and 8x. I am underwater on that…

I do have nine other positions totaling 0.5% of my IRA port. These are the dregs of my stock picking portfolio. They have been held for less than a year, mostly 10 months. I hold them for self-mockery for being defensively positioned for macro reasons. When I looked last week, the nine positions had a median gain of 67% and an average gain of 73%. There may be an investing lesson in there somewhere. META is the only mag-7 in there and up only 41%.

So I spare the community from my investment commentary.

Enjoy the weekend,

KC

3 Likes

ESPR was 4.7%. Now down to 4.4% even though I bought a dip or two.

Bitcoin, JEPQ, and the short term treasury ETF’s and are almost 67%. Cash 28%. Ready for whatever, including general geopolitical chaos and DC theatrics.

KC

KC

3 Likes

Pricing action wouldn’t indicate it but buy out rumours still happening.

Or some crazy price targets

https://x.com/brinkswealth10/status/1889324665853923331?s=61

1 Like

ER is before open on tuesday

No rev surprise, for me, expected, as their investor preso update in Jan showed Q4 US scripts up 12% q/q.

Due to seasonal pricing rebate thingies, rev may be closer to 9-10%?

So something like $33-34m is my guess.

More important will be any news on:

- Buyout or US partnership (unlikely)

- Canada partnership update

- More on April investor day where they show off new Liver-focused molecule/product. Can they get repriced based on new TAM?

- Any color on current Q1 script or forcast.

Many online noted march 14th is annually when mgmt gets option and stock comp grants. Question is if stock starts to fly after that, leading into investor day.

Realistic competition is years away, but competitors in the pipe will continue to make noise.

Q1 ER likely back to earlier in calendar in May. If nothing has changed by June in atock price, we may simply have more of an ESTC on our hands than a TTD, and I will likely significantly cut down and move on.

Will broader market tank under Trump austerity/chaos? If so, like with ESTC last time around, I was able to bail and move into a beaten down future winner SPG.

My ideal scenario, of course, is ESPR gives me a winning exit i want, AND I emerge in time, with extra loot, to take advantage of any crash bargains.

But universe doesnt always play along w what we want.

On plus side, my son got accepted into college he wanted…i am a proud/relieved dad tonight.

Enjoy weekend all,

Dreamer

8 Likes

3 Likes

– FY24 Total Revenue Grew 186% Y/Y to $332.3 Million; FY24 U.S. Net Product Revenue Grew 48% Y/Y to $115.7 Million –

–Q4 Total Revenue Grew 114% Y/Y to $69.1 Million; Q4 U.S. Net Product Revenue Grew 52% Y/Y to $31.6 Million –

– Q4 Retail Prescription Equivalents Grew 45% Y/Y and 12% Q/Q –

1 Like

New investor preso

Will weigh in when i can after conf call

Busy work day

https://www.esperion.com/static-files/3bd22c66-d8a0-40f4-b342-3ab81908bf27

Net is scripts more important, for trends, than sales due to rebate lumpiness, making q/q sales flat yet scripts up 12% q/q.

You would think a q1 q/q bounceback in Sales if Scripts stay solid. Will see.

Announced triple combo which should extend patent life.

Investor day still April 24th.

Dreamer

4 Likes