Some highlights here:

https://x.com/LucidDreamer397/status/1896938868395659677

and my latest “what has happened?” list

Some highlights here:

https://x.com/LucidDreamer397/status/1896938868395659677

and my latest “what has happened?” list

I wish they would provide a top line outlook, instead just got the expense outlook:

“ 2025 Financial Outlook

The Company expects full year 2025 operating expenses to be in the range of $215 million to $235 million, including approximately $15 million in non-cash expenses related to stock compensation.”

Yeah. I think this mgmt understands the science and the game they are playing in terms of having a real/proven drug asset with growing sales, and doing partner/licensing deals and ultimately trying to (I assume) sell the US rights or the company altogether. I don’t think they are sales and marketing experts. I can give them a pass in 2024 with a newly expanded label and mixed insurance coverage and being unable to predict script (and therefore sales) growth. But it has been 3 Q’s now, most payers are onboard. They should at least throw out a low-bar number for the classic beat and raise method each Q throughout the year.

They could also argue they are more than just the US sales and that the timing of milestones based on regulatory approvals or sales by partners in other countries is a bit out of their control. But I think a forecast on US Sales isn’t too much to ask at this point. It is what it is, and my expectations are 50% growth for 2025 y/y. They should do better than that, but it gives me something to work with:

US Sales

2024 Rev = $115m approx

2025 proj Rev (my goal) = $172m for 50% y/y growth

Other expected revenue

*$130m in Otsuka milestones by/before Q425

*$40m in misc non-Europe royalties and “collaboration” rev which is mainly -pill/product reimbursement. Total guesstimate.

*Excludes royalties for DSE/Europe, as those rights were sold to OMERS for $300m+ and revert back to Esperion after OMERS makes 1.7x their investment, which is tentatively projected as 2028.

So my bingo card has something like $340m in total sales for 2025.

They owe $65m in notes due in Nov.

That leaves $275m.

Expenses at high-end proj to be $235m

So they should come away with $40m to add to their cash, barring some new developments. Believe cash was currently $144m.

So they will burn some cash Q1-Q2 and probably Q3, and once Otsuka milestones hit, their accounts will be flush again.

Qtrly revenues are harder to predict. I would have said Q1 trends indicate a likely pop due to the seasonal impacts of how Medicare works, which led to pop in Q124 and flattish Q424 despite script growth being steady and up to right along the way. CFO claiming new rules make that lumpiness smooth out. So unclear what the Q1 number should be. But a guess:

US Sales in 2025

Q1 $36m

Q2 $40m

Q3 $46m

Q4 $50m (typically weaker due to holidays?)

that comes out to $172m, so will go with that for now.

Dreamer

Then they could just give the US sales numbers and maybe sales by active partners exclude Milestone payments or regions awaiting regulatory approvals. Those should be predictable.

Otherwise, there isn’t anything not to really like other than the share price.

amazingly, mgmt really did do their annual stock comp package distribution today.

a lot of internet chatter felt the stock was staying pinned until these clowns got hooked up. Who knows. If people had that kind of power of any given stock price, they would be billionaires already, is my rebuttal.

But if it helps investors to feel mgmt is more aligned, then, yes, mgmt certainly has more incentive now for stock price to go up.

Conveniently, mgmt got shares and options, and the options were at $1.50, which is current price from Friday close and happened to be a 52 wk low.

#convenient

Onward and upwards now, hopefully.

https://www.esperion.com/investor-relations/financial-information

Dreamer

My favorite pastime these days is buying the ESPR dip, dip, dip. Does this qualify as a ‘dip’? Or a whitewater rapid. Anyway, dipped in at $1.485 and $1.495. Green, for the moment on those. 5% position, quite red.

Macro and Geo…, sigh

KC

Not sure the angle here.

PR today w more questions than answers.

Vague, inept, or sly? History idnt on mgmt side.

Dreamer

I think this company really sucks at promoting itself in the US.

Apparently the DSE partner for Europe has UK growing at 100% y/y.

So - again - the drug works. The drug sells. US mgmt just is not very good.

Doesn’t change the thesis that the company/IP has value in a buyout.

Just means they probably get less than they should for it. But that is like arguing over getting 2-3x your return from today’s prices or 4-5x. Both are still good.

Anyway, overall I am hearing that cost of a study may not be egregious. Not clear the patent extension covers all BA products in US or just for pediatrics, but the thought process being thrown around is that by end of 2030, the runrate in US should be closer to $1b/year.

So, in theory, the 6-month patent extension they received should help them bring in another $500m more in revenue than they otherwise would have. So there is some value there. And if a study is under $10m or so, as some claim, the ROI, while not massive or terribly useful in the short-term, is justifiable.

The other angle is that the study will also allow for data points tied to other indications related to their upcoming R&D day. So if there is a market for pediatric liver/kidney, perhaps the side data from this study helps support those claims. Will see.

It is just incredibly hard to understand how/why this mgmt can’t just include some more useful details in their PR, such as how much it will cost, how they will pay it…even just hinting by using terms like “not prohibitive” or “reasonable costs” or “non-dilutive” etc etc…

But, nope…gotta be vague.

This speaks to either:

Neither is a good answer.

Again though - just bc this mgmt are ineffective at supporting shareholders (one of the key roles of execs at publicly traded companies, btw) doesn’t mean that the company won’t get sold in spite of them.

Dreamer

Updated my sanity list of why this is a good investment, despite mgmt.

ACC and Investor Day fast approaching in late March and April. Good oppty to promote and drive awareness on Triple-Combo drug upside and the new Indications (Liver, etc).

Enjoy the weekend all,

Dreamer

IR reply on costs of the new Pediatrics P3 study. Good response, but mind-boggling that they couldn’t have worded this in their PR in the first place.

"Thank you for reaching out and for your question. The costs associated with this trial are relatively small, and all related expenses have already been factored into our 2025 expense guidance. The key opportunity here is that upon completion of the trial, we will be eligible for a 6 month patent extension, which would provide meaningful additional value to the program.

Thank you,

Esperion IR"

New April 7th Needham conference announced:

Dreamer

I officially give up on ESPR.

In the sense that I don’t want others to get sucked in, as this has obviously been a bad call.

I am holding on to a large chunk still, but not gonna advertise it.

Will add my 2 cents after the R&D day later this month.

But this feels like as bad a call as ESTC.

I do remember that ESTC, during the covid drop, was maddeningly painful and it all came back. But I just don’t know what this mgmt is or isn’t doing.

They replaced a board member today, which seemed to pop the premarket.

But I never imagined it would get this low again, after all the positive news the past year. Doesn’t make sense.

Another reason why you never base your investment advice on what some dude on the internet says. Good luck all.

Dreamer

Agree but what some dude says on the internet in this case was and is backed by evidence and sound reasoning. The stock movement is a real head scratcher.

Rule 1. Don’t lose your money.

Rule 2. Never (again) investing in biotech stocks

Market hates biotech stocks (check XBI), 99% stocks are down or years away from old highs.

You made me look up ILMN (Illumina) which is back at levels from 10+ years ago.

Biotech has always been a gamble (Celera, anyone?).

Difference here is I was just looking at actual sales…not hype of a startup or AI something something or drug wrapping up P3 studies before an approval.

$370m in global sales last year ($250m DSE in Europe, $120m in US).

Comes down to mgmt.

Always should lean towards solid mgmt.

Dreamer

It is much more competitive for ILMN now than 10 years ago… also, it’s a battle between driving the cost down faster than the market seems to grow. Getting much more commoditised now so not been a good hold. It has been a bit painful

ESPR is more mystifying.. seems a growing movement to replace the CEO and board.. hopefully will start to see some action.

ESPR has been an utter disaster of an investment.

Obviously hoping for a partnership/BO (buyout) to bail me out of this deep hole.

Generally I had been careful when buying and felt like a genius when I got mgmt’s option prices around $1.50 and now we are around $1. Crazy.

Theories floating around about warrants/convertibles/Wasatch unloading, but that isn’t my forte to understand hedge fund and institution games. I just try to analyze if a stock/company seems to have upside, and this surely does.

My assumption, outside of just possibly a criminal (or criminally inept) CEO in Sheldon Koenig, is that the CEO overplayed his hand and didn’t take some perceived lowball offers, whether for US partnership or outright BO.

For a company that has an R&D day in 2 weeks that should be heralding new product lines and future recurring revenue stream (assuming they find a partner, such as Otsuka for Bempedoic Acid + Otsuka’s existing kidney medication, which they already filed a patent for, and also this new Liver indication.

Studies show synergy with GLP-1 drugs. etc etc

Is CEO simply holding out for too much, and now with his stock at $1 vs $3.80 it is that much harder to justify the premium he probably wants to be bought at.

It is just all very disappointing, and also a reminder (for me) to only invest in companies with perceived strong/talented/motivated and ideally founder CEO’s. This guy clearly is not, and with his CMO gone last year and now his CCO, he doesn’t seem to inspire his c-suite to stick around and/or he made bad hires and they underperformed. Neither answer is good.

Live and learn.

Dreamer

$1 came and went, surprised in the drop.. now low .90’s. Will wait to earnings before deciding if it is worth holding, investing or selling.

For what its worth…

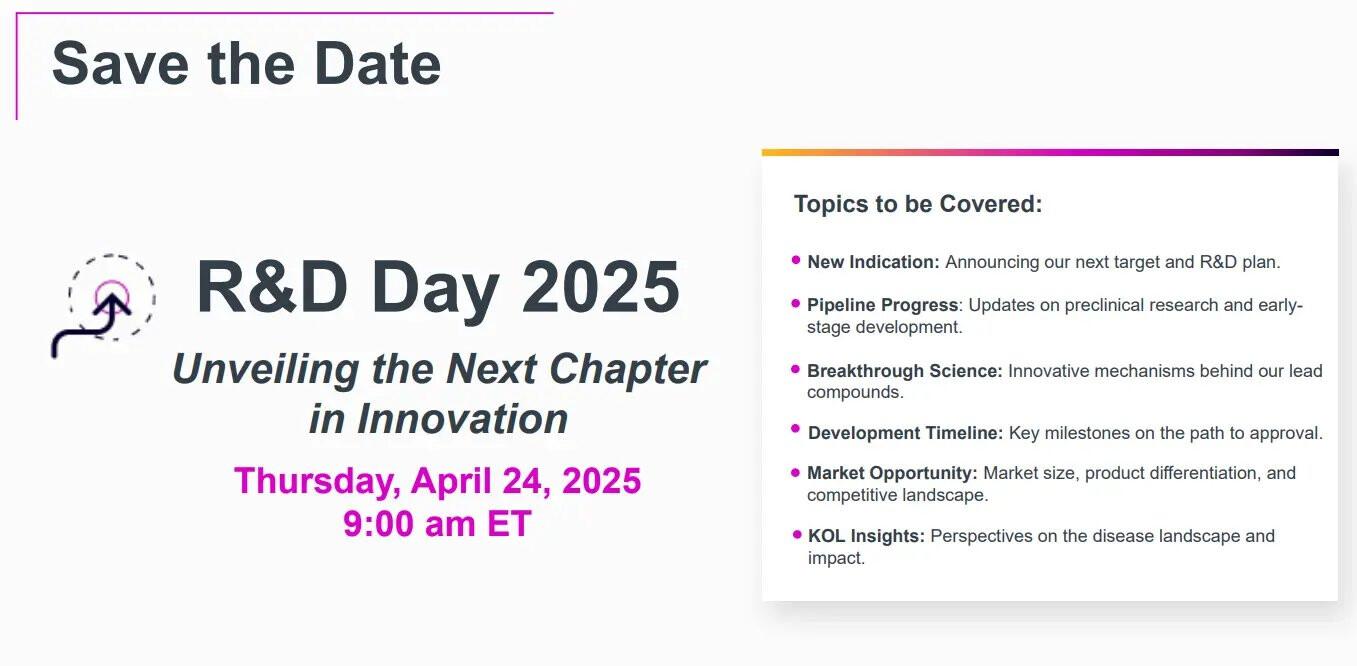

R&D day tomorrow - will be interesting.

I hope they speak to some/all:

advance Liver medication. 2025 article here: Bempedoic acid suppresses diet-induced hepatic steatosis independently of ATP-citrate lyase - ScienceDirect

discuss Kidney medication. Patent here in Dec 2022 tied to Otsuka's Tolvaptin drug: Unified Patents - Analytics Portal

Will any of the KOL's speak to the underlying ACLY "platform" or "mechanism" and the inherent potential across multiple diseases? https://www.esperion.com/science/pipeline

patents submitted for GLP-1 and BA…what about that angle, will it come up? Jan 2025 patent: WIPO - Search International and National Patent Collections

BA to use in AAA abdominal aortic aneurysm, from March 2025 article: Inhibition of ATP-citrate lyase by bempedoic acid protects against abdominal aortic aneurysm formation in mice - ScienceDirect

Been hesitant to speak on this stock since it has been such a dud. The science seems strong, the intl sales are strong, but US leadership is iffy.

I cant speak to stock manipulation, but the fundamentals dont seem to align w stock price.

ER May 6th in two weeks.

Between tomorrow and ER, I will either remain patient or cut some losses.

Dreamer